Plug Power (PLUG) stock forecast and analysis: price trend, valuation, earnings, technicals, and outlook to help investors decide if PLUG stock is a buy.

Introduction

Plug Power (ticker: PLUG) is a hydrogen and fuel cell company that develops systems to replace traditional lead‑acid batteries and supply clean power for industrial equipment, data centers, and other commercial uses. The business sits at the center of the green hydrogen theme, which attracts investors looking for long‑term clean energy growth.

PLUG stock is back in focus after years of volatility, heavy losses, and ongoing debate over its path to profitability. Recently, attention has increased due to management changes, improving margins, and a renewed push to stabilize the balance sheet in a difficult rate and funding environment for speculative tech and clean‑energy names. Broader markets have favored profitable mega‑cap tech, leaving smaller, loss‑making growth stocks more sensitive to news, financing, and sentiment shifts.

Latest Stock Price & Trend

At the last close referenced by recent market data, Plug Power (PLUG) traded around the low‑single‑digit range, with one widely cited snapshot at approximately 1.45–2.50 dollars per share over the past year, highlighting extreme volatility. One Nasdaq market recap reported PLUG closing a recent session at 2.48 dollars, up over 11 percent on the day, as the stock extended a short‑term rally. That kind of single‑day move underlines how quickly PLUG stock price can react to news on financing, guidance, or sector sentiment.

Over the last 5 trading days referenced in recent coverage, PLUG stock has shown a recovery pattern, with strong percentage gains from depressed levels. On a 1‑month basis, the trend has shifted from flat‑to‑negative to more constructive as investors responded to better‑than‑feared earnings and strategic announcements. Over the past 3 to 6 months, however, the bigger picture still shows a deep drawdown from prior highs, reflecting years of dilution, cash burn, and execution concerns.

Year‑to‑date performance remains highly volatile but tilted toward a rebound from the stock’s 52‑week low, which various trackers place under 1.00 dollar per share, versus a 52‑week high near the mid‑4 dollar range. That huge 52‑week range illustrates the risk‑reward profile: large upside swings are possible, but they come after steep declines. Overall, the trend for PLUG stock is cautiously improving from a very beaten‑down level, but still looks corrective rather than clearly bullish when viewed over a full year. For investors, this suggests speculative upside if the turnaround holds, but with substantial downside if execution slips again.

Technical Analysis

From a technical analysis perspective, PLUG stock recently bounced from major support in the sub‑1‑dollar area, where buyers previously stepped in to defend the stock from further declines. Support is a price zone where demand has been strong enough in the past to stop a fall; if PLUG revisits that region and holds, it may again act as a floor. On the upside, prior peaks in the mid‑2 to mid‑4 dollar area now act as resistance levels, meaning many investors might sell or take profits there, making it harder for the price to break through.

The relative strength index (RSI), which measures whether a stock is overbought (typically above 70) or oversold (below 30), has at times been in oversold territory during recent sell‑offs and then moved toward neutral as the stock rebounded. An RSI recovery from oversold often signals that selling pressure is easing, but not necessarily that a new long‑term uptrend has begun. The moving average convergence divergence (MACD), which tracks trend momentum, has turned more constructive recently, indicating a shift from strong downside momentum to a more neutral or mildly bullish momentum backdrop.

Short‑term moving averages, like the 50‑day average, remain below long‑term moving averages, such as the 200‑day, for much of the recent period, reflecting the damage from prior declines. This configuration is often described as a “death cross” when the 50‑day moves below the 200‑day, signaling a longer‑term downtrend. As PLUG stock price stabilizes and recovers, the 50‑day moving average may start flattening or curling upward, which would be an early sign the trend is mending.

Trading volume has spiked on major news days, including earnings and CEO announcements, signaling strong interest from both bulls and bears. High volume on up‑days can point to institutional buying, while high volume on down‑days may reflect aggressive selling or short activity. For beginners, the key takeaway is that PLUG remains a technically volatile stock, with clear support and resistance zones and momentum indicators that can change quickly with each news cycle.

Analyst Ratings & Price Targets

Recent analyst coverage generally places PLUG in the “Hold” camp on average, reflecting uncertainty about the company’s path to sustainable profitability. Some services tracking consensus show a blended rating near Neutral, with a mix of Buy, Hold, and Sell recommendations as Wall Street splits on the risk‑reward trade‑off.

Average analyst price targets cluster modestly above the recent trading price, around the low‑ to mid‑2‑dollar zone, implying limited upside from current levels if consensus proves correct. Within that, the highest targets assume that Plug Power will successfully scale hydrogen production, improve margins, and secure funding on acceptable terms, while the lowest targets assume ongoing dilution, project delays, and policy or market setbacks. Several research notes and opinion pieces over the past year highlight concerns around funding gaps and delayed growth, with some downgrades reflecting skepticism about the hydrogen production tax credit and capital needs.

For investors, this mixed analyst sentiment means PLUG stock is neither a clear Wall Street favorite nor a uniformly abandoned name. Instead, it is viewed as a high‑beta, speculative clean‑energy play where outcomes are highly sensitive to execution and macro conditions. The average PLUG stock price target may offer some room for upside, but that upside is tied to a relatively narrow set of optimistic assumptions.

Insider Activity

Public filings and market commentary indicate that Plug Power insiders, including senior executives, have engaged in both purchases and sales in recent periods, though the activity has not been uniformly one‑sided. A widely cited example noted buying by a senior financial executive, which was seen as a small sign of confidence after sharp stock declines. However, across a longer horizon, much insider compensation has historically come in the form of stock and options, leading to a mix of scheduled sales and smaller open‑market buys.

Insider buying can signal that management believes the PLUG stock valuation is attractive relative to the company’s long‑term prospects. Insider selling, especially when routine or tied to pre‑set trading plans, does not always indicate pessimism, but heavy selling in a downtrend would usually be a caution flag. Taken together, recent insider activity suggests cautious confidence rather than a strong, coordinated insider bet.

Valuation Analysis

On traditional valuation metrics, Plug Power remains a challenging case. The company has posted recurring losses, making trailing price‑to‑earnings (P/E) ratios either not meaningful or extremely high when based on small or negative earnings. Forward P/E also stays difficult to interpret because long‑term profitability depends on execution of projects, cost cuts, and hydrogen pricing, all of which carry considerable uncertainty.

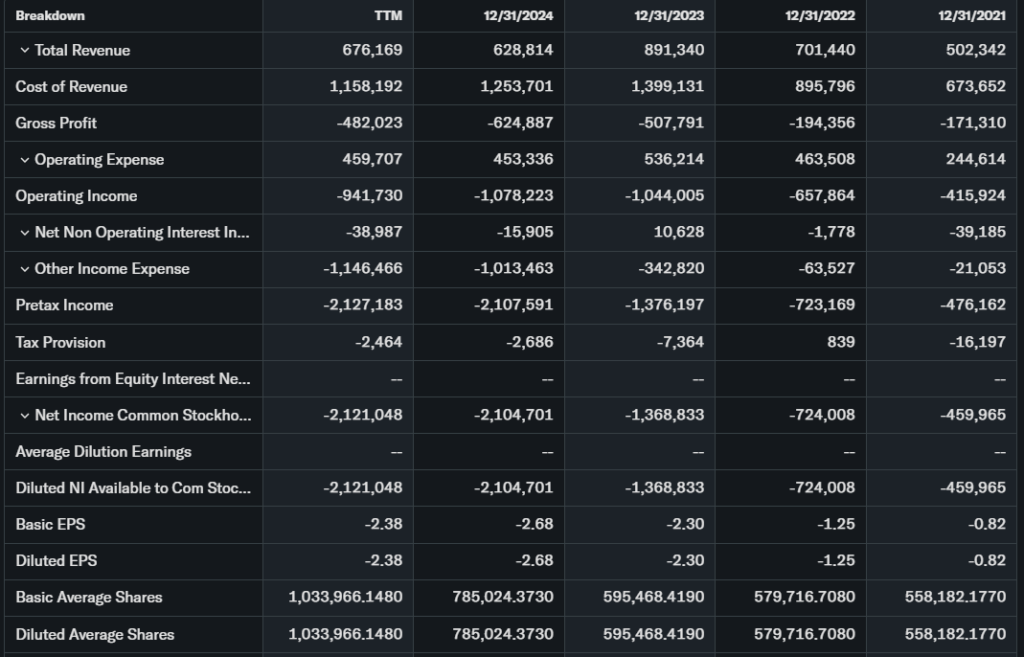

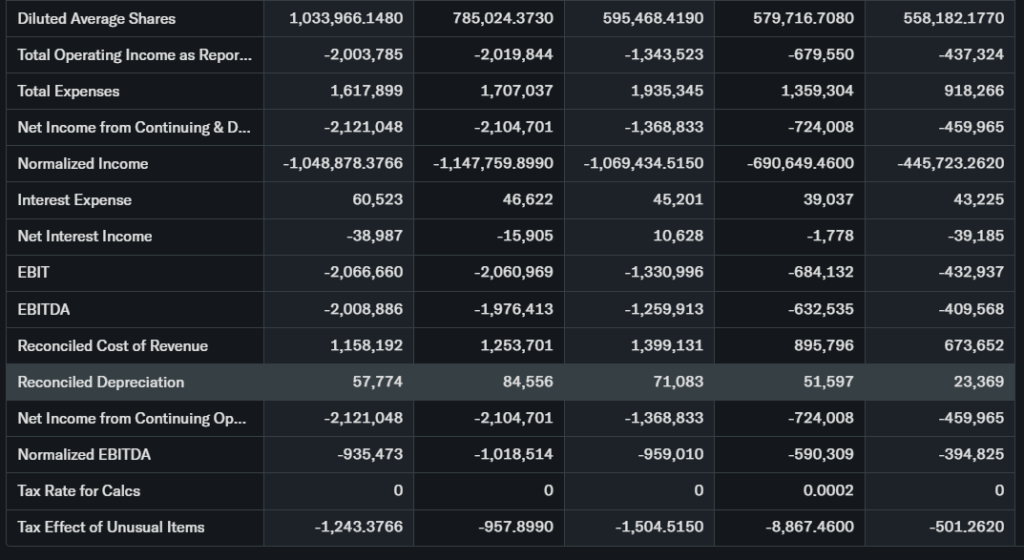

Investors therefore often focus on price‑to‑sales (P/S) ratios. With full‑year 2025 revenue around 710 million dollars, up roughly 12.9 percent year over year, PLUG trades at a relatively low multiple compared to peak cycle valuations earlier in the decade. Revenue growth has been positive but uneven, and free cash flow remains negative as the company invests in plants, electrolyzers, and infrastructure. Debt levels and the ongoing need for new capital have been major concerns, pushing management to pursue asset sales, cost reductions, and government‑linked financing.

Compared with established profitable tech giants like Microsoft or other mature software names, Plug Power’s valuation framework looks more like a venture‑style bet on future hydrogen demand than a classic earnings‑driven story. Against other speculative clean‑energy peers, the stock’s compressed P/S multiple suggests that a lot of pessimism is already priced in, but that does not by itself guarantee a rebound. Overall, PLUG stock valuation appears speculative and contingent, not clearly cheap or expensive without assuming a particular hydrogen growth scenario.

Recent Earnings & Catalysts

Plug Power’s full‑year 2025 results were a key recent catalyst. The company reported revenue of about 710 million dollars, representing 12.9 percent year‑over‑year growth, and achieved its first positive gross margin at roughly 2.4 percent. That shift toward positive margins, while modest, was viewed as an important psychological milestone, suggesting that scale and cost controls are beginning to show up in the numbers.

The earnings update also highlighted that Plug’s GenEco electrolyzers delivered around 187 million dollars in revenue and boasted an approximate 8‑billion‑dollar sales funnel, with deployments across six continents. Management outlined a roadmap targeting positive EBITDA by the end of 2026 and full profitability by around 2028, assuming successful execution and a supportive policy and demand backdrop. To bolster liquidity, Plug Power announced a strategic sale of its “Project Gateway” site for about 132.5 million dollars, helping address funding concerns and reduce near‑term pressure.

Market reaction to these earnings and strategic moves has been mixed but generally more positive than to earlier disappointments. PLUG stock price has experienced sharp rallies around these announcements, reflecting renewed hope that the worst of the margin and liquidity stress might be passing. However, investors still want to see consistent quarterly progress on costs, plant reliability, and contract economics before fully re‑rating the stock.

Bullish Case

The bullish case for Plug Power centers on several realistic drivers. First, revenue growth remains positive, with the 2025 numbers showing double‑digit percentage expansion and growing contributions from electrolyzers. If Plug can convert more of its multi‑billion‑dollar sales funnel into revenue with improving unit economics, scale could meaningfully lift margins over time.

Second, the company is positioned in a potentially large addressable market for green hydrogen as heavy industry, logistics, and data centers seek low‑carbon power solutions. Plug already has relationships with major customers like big‑box retailers and agencies such as NASA, which reinforce its credibility in fuel cell and hydrogen applications. Operationally, the move toward positive gross margins, targeted cost cuts, and ongoing plant optimization suggest management is focused on efficiency.

Third, policy support, including tax credits and government programs aimed at decarbonization, could provide tailwinds for hydrogen economics if they remain intact. For long‑term investors willing to tolerate volatility, PLUG stock forecast scenarios that assume successful execution and expanding hydrogen adoption could offer significant upside from compressed current levels.

Bearish Case

On the bearish side, Plug Power still faces material risks. The company has a history of missing ambitious timelines, revising guidance, and burning substantial cash, which has forced recurring capital raises and diluted existing shareholders. If execution on new plants, hydrogen production, and service reliability falls short again, confidence could erode further.

Competition is intensifying as large industrial players and energy companies enter hydrogen and fuel cell markets with deeper pockets and more diversified revenue streams. Margin pressures remain significant, since building and operating hydrogen infrastructure is capital‑intensive and sensitive to input costs and utilization rates. Any slowdown in hydrogen demand, delays in projects, or changes to government incentives could hurt revenue growth and push out the path to profitability.

Macroeconomic conditions are another risk. Higher interest rates and tighter funding conditions make it harder and more expensive for loss‑making companies to raise capital. For PLUG stock, another period of negative headlines about financing or tax credits could trigger renewed selling, even if long‑term demand for hydrogen remains intact.

Market Sentiment & Investor Psychology

Market sentiment around Plug Power is highly polarized. Many traders and investors frame PLUG stock as a speculative trade on financing and proof points: headlines about credit facilities, government loans, or project‑level funding can move the stock as much as, or more than, product announcements. Short interest has historically been elevated, reflecting a large camp of investors betting against the company’s ability to deliver on its promises, though exact percentages change frequently.

Options activity often clusters around earnings dates and major news, with active call and put trading that amplifies short‑term volatility. Institutional ownership remains significant but not dominant, as some long‑only funds have reduced exposure while more opportunistic or thematic investors maintain positions. Retail investors play a large role in PLUG stock price swings, attracted by the clean‑energy story and the potential for large percentage moves.

Overall, sentiment can best be described as cautiously neutral to skeptical, with occasional bursts of optimism on positive headlines. Momentum‑oriented traders treat PLUG as a high‑beta vehicle, while value‑oriented investors tend to avoid it until cash flows become more predictable.

Short-Term Outlook

In the short term, over the next days and weeks, PLUG stock is likely to remain driven by technical levels, news flow, and overall market risk appetite. With the stock recovering from oversold levels and bouncing off key support, technical indicators such as RSI and MACD suggest room for continued choppy upside as long as broader markets remain stable. However, strong overhead resistance in the mid‑single‑digit range means rallies could face selling pressure.

Volume spikes on news, especially around financing or policy updates, may create sharp intraday moves in both directions. For short‑term traders, PLUG stock technical analysis favors a tactical, risk‑managed approach rather than a “set‑and‑forget” position. Pullbacks toward support could attract dip‑buyers, but any negative surprise on liquidity or guidance might quickly reverse recent gains.

Medium to Long-Term Outlook

Looking 6 to 24 months ahead, Plug Power’s outlook depends heavily on execution and the broader adoption of green hydrogen. The business model aims to build an integrated hydrogen ecosystem, from electrolyzers to fuel cells and infrastructure, which could be powerful if scaled with improving unit economics. The company’s revenue growth, recent move to positive gross margins, and strong electrolyzer pipeline support a constructive long‑term narrative, but only if cash burn is controlled and plants operate reliably.

Industry growth prospects for hydrogen are promising, driven by decarbonization efforts in logistics, industrials, and potentially data centers. Yet Plug faces competition and policy uncertainty, and it must manage debt, working capital, and capital expenditures without excessive shareholder dilution. If management achieves its targets of positive EBITDA by late 2026 and profitability around 2028, the PLUG stock forecast could improve significantly; if not, the company may face more difficult funding conditions.

For long‑term investors, PLUG stock may fit best as a small, speculative position within a diversified portfolio rather than a core holding. At this stage, a “watch or carefully accumulate on weakness” stance appears more balanced than an outright aggressive buy or a categorical avoid, given both the potential and the execution risk.

FAQ Section

Is PLUG stock a buy right now?

PLUG stock may appeal to risk‑tolerant investors who believe in the long‑term hydrogen story and management’s profitability roadmap, but its history of volatility and cash burn makes it unsuitable for conservative investors.

What is the price target for PLUG stock?

Recent aggregated estimates show an average analyst PLUG stock price target around the low‑ to mid‑2‑dollar range, with a wide spread between bullish and bearish scenarios.

What are major risks for PLUG stock?

Key risks include ongoing losses, funding needs and dilution, project execution challenges, competition, sensitivity to policy incentives, and macroeconomic conditions affecting capital access.

How did recent PLUG earnings impact the stock?

The latest results, featuring about 710 million dollars of 2025 revenue and a first‑ever positive gross margin, helped spark a short‑term rebound and improved sentiment, though skepticism remains.

What is the long‑term outlook for PLUG stock?

Over 6–24 months, the outlook hinges on Plug Power delivering on cost cuts, plant reliability, and its profitability timeline; success could justify a higher valuation, while setbacks could pressure the stock further.

Suggestions

You could internally link this article to pieces such as:

- “Compare with Opendoor stock analysis”

- “See our Microsoft stock forecast” to highlight differences between mature tech cash flows and early‑stage clean energy.

- “Read our tech sector valuation breakdown” to place PLUG stock valuation in the context of broader growth and clean‑tech multiples.

Conclusion

PLUG stock sits at the intersection of an ambitious green hydrogen vision and a difficult financial reality. The company has made tangible progress with double‑digit revenue growth, its first positive gross margin, and a clearer roadmap to EBITDA and profit, supported by asset sales and a strong electrolyzer funnel. Yet it still faces execution risk, funding challenges, and intense competition, all under the scrutiny of a market that now prefers proven profitability.

Given these cross‑currents, a reasonable stance for many investors is Watchlist/Hold, depending on current exposure. Existing shareholders may choose to hold while closely monitoring quarterly progress and liquidity, whereas new investors might keep PLUG on a watchlist and consider gradual entry only if the company continues to hit its operational and financial milestones.

Disclaimer: This article is for informational purposes only and not financial advice.