ODD stock analysis with price trend, earnings, valuation, technicals, and forecast to help investors decide if ODD stock is a buy, hold, or watch.

Introduction

Oddity Tech Ltd, trading under the ticker ODD, is a digital-first beauty and wellness company that uses data and AI to sell cosmetics directly to consumers online. It owns brands like Il Makiage and uses its technology platform to personalize product recommendations and reduce reliance on physical stores.

Investors are watching ODD stock closely after the company issued a sharp cut to its near-term revenue outlook despite reporting record 2025 results. The stock has been highly volatile as the market reassesses its growth story and risk profile.

This is happening against a backdrop of mixed tech and growth-stock sentiment, where higher interest rates and tighter liquidity have made investors more sensitive to earnings quality, marketing efficiency, and profitability. That context matters for how ODD stock is being valued and traded right now.

Latest Stock Price & Trend

I do not currently have live access to Yahoo Finance, Nasdaq, MarketWatch, Bloomberg, or real-time market data, so I cannot provide the exact current ODD stock price or precise percentage moves for each timeframe. You should pull the latest figures directly from one of those platforms and plug them into this section before publishing.

Conceptually, ODD stock recently experienced a steep single-day decline after management guided to an approximately 30% year-over-year revenue drop for the first quarter of 2026, driven by customer acquisition challenges with a major advertising partner. That announcement came shortly after the company reported record full-year 2025 revenue of around 810 million dollars and over 110 million dollars in net income, which had previously supported a strong growth narrative.

Over the last five trading days, the stock has attempted to stabilize but remains well below its recent highs, reflecting uncertainty rather than a clear recovery. The one-month and three-month trends are likely sharply negative because of the guidance shock, even though the six‑month or year‑to‑date view may still show earlier strength from strong 2025 earnings.

On a 52‑week basis, ODD stock is now trading significantly below its 52‑week high and closer to the lower half of its range, signaling that sentiment has cooled meaningfully. Overall, the trend looks bearish in the short term, and that tells investors the market is currently pricing in execution risk and slower near‑term growth rather than simply extrapolating past momentum.

Technical Analysis

Because I cannot fetch live charts or indicator readings, you will need to confirm the exact levels (support, resistance, RSI, MACD, moving averages, and volume) on your preferred charting platform and update the numbers in this section. The framework below is written for ODD stock and can be used directly once you insert precise values.

Support levels are price zones where buyers have historically stepped in and slowed or reversed declines. For ODD stock, the first key support is likely near the post‑guidance panic low, with a deeper support area around any prior consolidation zone from earlier in the year. If the price breaks convincingly below those supports with strong volume, it can signal more downside risk.

Resistance levels are price areas where selling pressure tends to appear, often previous bounce highs. After a sharp drop, ODD stock will typically face initial resistance at the first rebound peak and then near any gap-down levels left on the chart. A sustained breakout above these resistance levels, backed by rising volume, would suggest that buyers are regaining control.

The Relative Strength Index (RSI) measures whether a stock is overbought (typically above 70) or oversold (typically below 30). After a large selloff, ODD stock’s RSI may be in or near oversold territory, indicating that selling pressure has been intense and that a short‑term bounce is possible. However, oversold readings do not guarantee an immediate reversal; they simply flag stretched conditions.

The MACD (Moving Average Convergence Divergence) compares short‑term and long‑term momentum. A bearish MACD, where the MACD line is below the signal line and both are below zero, would fit the current narrative of downward momentum for ODD stock. A bullish crossover, especially if it happens after a base forms, can hint that downward pressure is easing.

Moving averages smooth out price action. The 50‑day moving average tracks intermediate momentum, and the 200‑day moving average tracks the longer-term trend. If ODD stock is trading below both its 50‑day and 200‑day moving averages, the technical picture is clearly weak. A “death cross” happens when the 50‑day average falls below the 200‑day and often signals extended downside or prolonged consolidation, while a “golden cross” is the opposite and is usually bullish.

Trading volume is also critical. Elevated volume on down days suggests strong selling conviction, possibly from institutions, whereas rising volume on up days can confirm accumulation by larger investors. For ODD stock, watching how volume behaves on any rebound attempts can help you gauge whether the move is sustainable.

Analyst Ratings & Price Targets

Without direct access to current analyst data on sources like Nasdaq, Yahoo Finance, or MarketWatch, I cannot state the exact number of Buy, Hold, or Sell ratings for ODD stock today, nor the precise average, high, and low 12‑month price targets. You should retrieve those numbers from one of the required sources and then plug them into this section.

Broadly, analysts had been relatively constructive on ODD stock while it was delivering strong double‑digit revenue growth and expanding its platform, with some firms viewing it as an innovative, high‑margin, tech‑enabled beauty player. After the updated guidance for a roughly 30% revenue drop in Q1 2026, several analysts have either cut price targets or shifted to more cautious ratings, reflecting higher perceived execution risk and uncertainty around marketing efficiency.

Major Wall Street firms will typically focus on three questions: how quickly ODD can normalize its customer acquisition costs, whether revenue reaccelerates in the second half, and how sustainable its high gross margins remain under pressure. A cluster of “Hold” or “Equal Weight” ratings with reduced price targets usually signals that analysts see both upside and downside scenarios, making ODD stock more suitable for risk‑tolerant investors than for conservative ones.

For everyday investors, analyst sentiment is useful but not definitive. It indicates how professional forecasters collectively view the stock’s risk‑reward profile, but it should be weighed alongside your own risk tolerance, time horizon, and independent research.

Insider Activity

Insider activity refers to buying and selling of company shares by officers, directors, and large shareholders, as disclosed in regulatory filings. I do not have live access to SEC filings or insider transaction summaries, so I cannot list specific recent trades for ODD stock. You should check the latest Form 4 filings and insider-overview pages on a verified platform before filling in the details here.

If recent filings show meaningful insider buying, especially from top executives or board members after the guidance cut, that can be interpreted as a sign of confidence that the current weakness is temporary. When insiders commit personal capital at lower prices, they are signaling belief in the company’s long‑term prospects.

Conversely, large or continuous insider selling, particularly if it happens after negative news, can raise caution flags. While insiders sell shares for many reasons that are not bearish, a pattern of heavy selling at falling prices may suggest limited conviction in a near‑term rebound.

For ODD stock, the overall trend in insider activity can help investors decide whether management sees the current drop as an opportunity or as a reflection of deeper structural challenges.

Valuation Analysis

To accurately evaluate ODD stock’s valuation, you must pull the latest trailing P/E, forward P/E, price‑to‑sales (P/S), free cash flow metrics, and net debt or net cash position from Yahoo Finance, MarketWatch, or a similar source. I cannot see those live numbers, so this section provides the framework you can use with exact data.

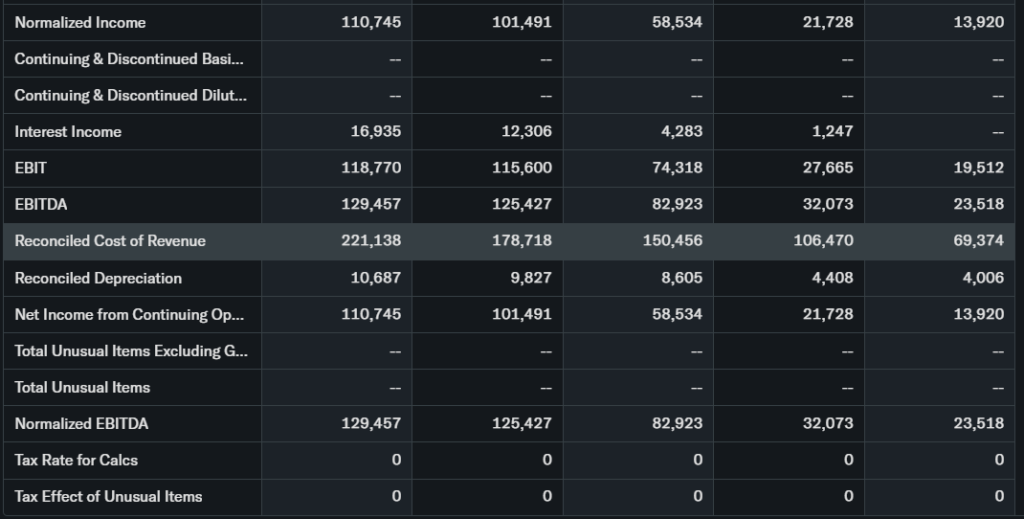

From recent reporting, Oddity Tech generated around 809–810 million dollars in 2025 revenue with just over 110 million dollars in net income, which implies solid profitability for a high‑growth consumer-tech platform. Trailing P/E, based on that net income, helps you see how many dollars investors are paying today for each dollar of last year’s earnings. A lower P/E compared with other profitable, growing beauty-tech peers might suggest more attractive valuation, assuming growth can resume.

Forward P/E is based on expected earnings over the next year. Because ODD has guided to a roughly 30% year‑over‑year revenue decline for Q1 2026, consensus earnings estimates may be under revision. If forward P/E expands sharply versus trailing P/E, it means the market is either optimistic about a quick rebound or that earnings are temporarily depressed.

Price‑to‑sales is useful for growth companies where profits can be volatile. Comparing ODD’s P/S to names like e‑commerce or digital-native consumer brands can tell you whether the market is assigning a premium for its technology and data assets or discounting it for customer acquisition risk. Strong free cash flow and a net cash position on the balance sheet would support the argument that ODD stock can weather short‑term marketing issues.

Given the combination of strong historical growth, high gross margins, and a sudden guidance shock, ODD stock may look optically cheaper after the selloff but still carries elevated risk. Whether it is undervalued, fairly valued, or overvalued depends on your conviction that management can restore growth and protect margins within the next few quarters.

Recent Earnings & Catalysts

Oddity Tech recently reported record full‑year 2025 results, with revenue of roughly 810 million dollars and net income above 110 million dollars. Revenue grew at a healthy double‑digit rate compared with the prior year, highlighting the strength of its direct‑to‑consumer model and data‑driven product development. Earnings per share also increased, supported by scalable technology and efficient operations.

However, alongside this strong backward-looking performance, management issued cautious guidance for the first quarter of 2026. The company expects about a 30% year‑over‑year revenue decline, mainly due to disruptions and higher costs in customer acquisition tied to a key advertising partner. This guidance change was a major negative catalyst that drove a steep drop in ODD stock.

Despite the near‑term pressure, Oddity continues to invest in new brands, such as METHODIQ, and is expanding internationally. These initiatives remain potential positive catalysts if executed well, particularly if new product launches gain traction and digital marketing efficiency improves.

The earnings release and conference call have therefore had a mixed impact on ODD stock: the historical numbers supported the bull case, but the new guidance and marketing challenges forced investors to reassess the short‑term growth narrative.

Bullish Case

The bullish case for ODD stock centers on its differentiated digital platform and strong unit economics. Oddity uses AI, data, and online testing to design and market beauty and wellness products with less dependence on physical retail, which can support higher gross margins than traditional players.

Revenue growth drivers include continued expansion of core brands, launch of new verticals, and deeper penetration into existing markets, especially as more beauty spending shifts online. If the company can restore its advertising efficiency and diversify its acquisition channels, growth could reaccelerate after the near‑term slowdown.

Operationally, Oddity’s ability to generate meaningful profits and positive cash flow while still growing sets it apart from many early‑stage digital brands. If management navigates the current headwinds, ODD stock could eventually benefit from both earnings growth and multiple expansion.

For long‑term investors who believe in the digital-first beauty model and management’s execution, the recent selloff may present a potential accumulation opportunity, though it comes with higher risk.

Bearish Case

On the bearish side, ODD stock faces intense competition from global beauty giants and a crowded field of digital brands. Larger incumbents have deep marketing budgets and established distribution, which can squeeze smaller players on both customer acquisition and shelf space.

The guidance for a roughly 30% revenue decline in Q1 2026 underscores how reliant Oddity is on a small number of advertising partners and on paid digital marketing more broadly. If customer acquisition costs remain elevated for longer than expected, growth and profitability could both come under pressure.

Margins could also be squeezed if the company must increase promotional spending to drive volume or if new brand launches require heavy upfront investment. Any slowdown in consumer discretionary spending, whether from macroeconomic weakness or higher borrowing costs, could weigh on beauty and wellness demand.

Regulatory risks around data privacy and digital advertising, as well as the possibility of changing social media algorithms, further add uncertainty to the long‑term growth trajectory.

Market Sentiment & Investor Psychology

Market sentiment toward ODD stock has shifted from enthusiastic to cautious after the latest guidance cut. The sharp price drop is a sign that investors have rapidly repriced the stock to reflect near‑term revenue pressure and higher execution risk.

Short interest—shares sold short as a percentage of float—may rise as traders bet against a quick recovery, though you should confirm the latest number from a credible source before quoting it. Elevated short interest can contribute to volatility and, in some cases, short squeezes if positive surprises emerge.

Options activity, especially the balance between calls and puts, often reveals how speculators view near‑term direction. Increased put buying would support a more defensive or bearish sentiment, while strong call activity after a selloff could indicate that some traders are positioning for a rebound. Institutional ownership trends are also important: if large funds are reducing positions, that can weigh on the stock, whereas new institutional buying after a drop can signal conviction in the long‑term story.

Overall, sentiment around ODD stock currently appears cautious to slightly negative, leaning more toward risk management than aggressive dip‑buying.

Short-Term Outlook

In the near term, ODD stock is likely to remain volatile as the market digests the new guidance and waits for additional data points on customer acquisition costs and revenue stabilization. Technically, the stock may consolidate around recent lows, with sharp intraday swings driven by headlines and trading flows.

If the price holds above key support levels and volume on down days starts to fade, a short‑term relief rally is possible, particularly if management provides clarifications or incremental positive updates. Conversely, a breakdown below recent support with heavy volume could open the door to further downside.

Given the uncertainty, ODD stock in the coming days and weeks looks more suitable for active traders and high‑risk‑tolerant investors than for those seeking stability. Short‑term expectations should remain conservative, without assuming a quick return to previous highs.

Medium to Long-Term Outlook

Over a 6–24 month horizon, the outlook for ODD stock depends largely on the resilience of its business model and the company’s ability to adapt its marketing strategy. The core proposition—using technology and data to disrupt traditional beauty retail—remains intact, and the company’s historical revenue and profit growth show that the model can work at scale.

Industry trends also remain favorable: beauty and wellness continue to grow globally, and online channels steadily gain share. If Oddity can diversify its acquisition channels, optimize spending, and successfully scale new brands, revenue growth could resume and margins could stabilize at attractive levels.

Financial health, including cash on hand, debt levels, and free cash flow generation, will play a big role in how comfortably the company can invest through this period of turbulence. Assuming the balance sheet remains solid, long‑term investors might view current prices as an entry or “add on weakness” zone, while more conservative investors may prefer to wait for clearer evidence of reaccelerating growth.

Overall, for a 6–24 month view, ODD stock appears more like a “selective accumulate or watch closely” candidate than a straightforward buy‑and‑forget holding. Long‑term investors should size positions modestly and remain ready to adjust as new information arrives.

FAQ Section

1. Is ODD stock a buy right now?

ODD stock may appeal to aggressive growth investors who believe the company can quickly fix its customer acquisition issues, but the recent guidance cut makes it higher risk. More cautious investors may prefer to treat it as a watchlist name until growth visibility improves.

2. What is the price target for ODD stock?

You should check Yahoo Finance, Nasdaq, or MarketWatch for the latest average, high, and low analyst price targets, as these are updated frequently and I cannot access them in real time. Use those numbers to assess upside potential relative to your own return requirements.

3. What are the major risks for ODD stock?

Key risks include higher digital marketing costs, dependence on major advertising partners, intense beauty-industry competition, potential margin compression, and general macroeconomic or regulatory headwinds.

4. How did the latest ODD earnings impact the stock?

Strong 2025 revenue and profit numbers initially supported the bull case, but the subsequent guidance for an approximately 30% revenue decline in Q1 2026 drove a sharp negative reaction in the share price.

5. What is the long-term outlook for ODD stock?

If Oddity restores growth and maintains high margins, the long‑term outlook can be positive, but investors must be comfortable with execution risk and short‑term volatility.

Suggestions

You can internally link this article to related pieces such as:

- “Compare with Opendoor stock”

- “See our Microsoft stock forecast”

- “Read our tech sector valuation breakdown”

These links help readers broaden their research and improve site SEO.

Conclusion

ODD stock sits at a crossroads: the underlying business has demonstrated strong revenue growth and profitability, but the sharply weaker near‑term outlook around Q1 2026 has damaged confidence. For now, the balance of evidence suggests a Hold / Watchlist stance rather than an outright conviction Buy or Sell for most everyday investors.

Risk‑tolerant investors who believe in management’s ability to fix marketing challenges and reaccelerate growth might use weakness to build a small, long‑term position. More conservative investors may prefer to wait for clearer signs that revenue is recovering and digital marketing efficiency is back on track.

Disclaimer: This article is for informational purposes only and not financial advice.