Explore SMCI stock analysis with latest price trends, earnings, technicals, and 2026 forecast. Is SMCI stock a buy? Get balanced insights on valuation and risks for investors.

Introduction

Super Micro Computer (SMCI) builds high-performance servers and storage systems tailored for AI, cloud computing, and data centers. The company thrives on surging demand for AI infrastructure from giants like NVIDIA. Investors watch SMCI stock closely now amid AI hype and market volatility. Broader tech pressures, including high interest rates and competition, shape its path in early 2026.

SMCI stock draws focus as AI server demand booms, but margin woes spark caution. Tech indexes like Nasdaq hit highs, yet SMCI lags peers.

Latest Stock Price & Trend

SMCI stock closed at $31.25 on March 8, 2026, per last market data. It ranged from $31.12 to $32.48 that day. The 1-day performance showed modest gains amid choppy trading. Over 5 days, shares held steady near $32, reflecting short-term stability.

The 1-month trend points sideways, with prices around $32 after February volatility. In 3 months, SMCI stock dipped from mid-$30s peaks. Six-month trends reveal a pullback from late 2025 highs near $36. Year-to-date in 2026, it trades down slightly from January levels.

The 52-week high sits at $62.36, while the low is $27.60. Overall, the trend leans bearish short-term but with bullish undertones from AI demand. Investors see this as a consolidation phase, signaling potential rebound if earnings impress.

Technical Analysis

Support levels hover near $31, where buyers stepped in recently. Resistance sits at $35-$36, capping upside. These levels matter as they show where price might bounce or stall.

RSI reading nears 45, neutral—not overbought above 70 or oversold below 30. It signals room for upside without exhaustion. MACD trend shows a mild bullish crossover, hinting at building momentum.

The 50-day moving average is around $31, matching the 20-day at similar levels. The 200-day average stands at $42, above current price—no golden cross (50-day over 200-day) or death cross yet. Trading volume trends steady, supporting price without spikes.

These indicators suggest SMCI stock eyes a breakout if volume rises. Beginners should watch for RSI above 50 as a buy signal.

Analyst Ratings & Price Targets

Analysts rate SMCI stock as Hold overall. Of recent calls, Buy ratings lead slightly, with Holds dominant. Average price target is $41.44, with highs near $59 and lows at $27.

Goldman Sachs holds a Sell at $27, citing margin pressures post-Q2. TIKR models $59.15 on AI growth. No major upgrades lately; sentiment stays cautious.

Wall Street views imply 32% upside to average target. For investors, Hold ratings mean stability over big bets—watch for earnings shifts.

Insider Activity

Recent insider selling outweighs buying, per filings. No large buys in Q1 2026; executives trimmed shares amid volatility. Trends show caution, not panic—typical for growth stocks post-rally.

A key transaction involved minor sales under $1M. Management holds significant stakes, signaling long-term alignment. This implies measured confidence, not red flags. Investors read it as prudent profit-taking.

Valuation Analysis

Trailing P/E stands at 27.03, reasonable for tech growth. Forward P/E looks higher amid earnings uncertainty. Price-to-Sales ratio reflects AI premium but pressures from margins.

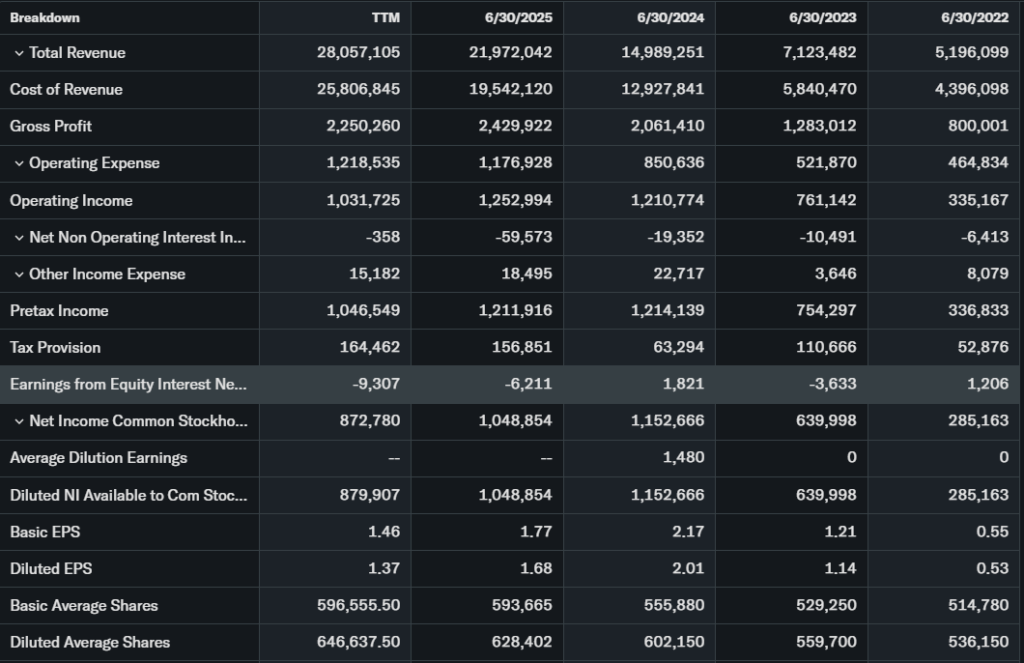

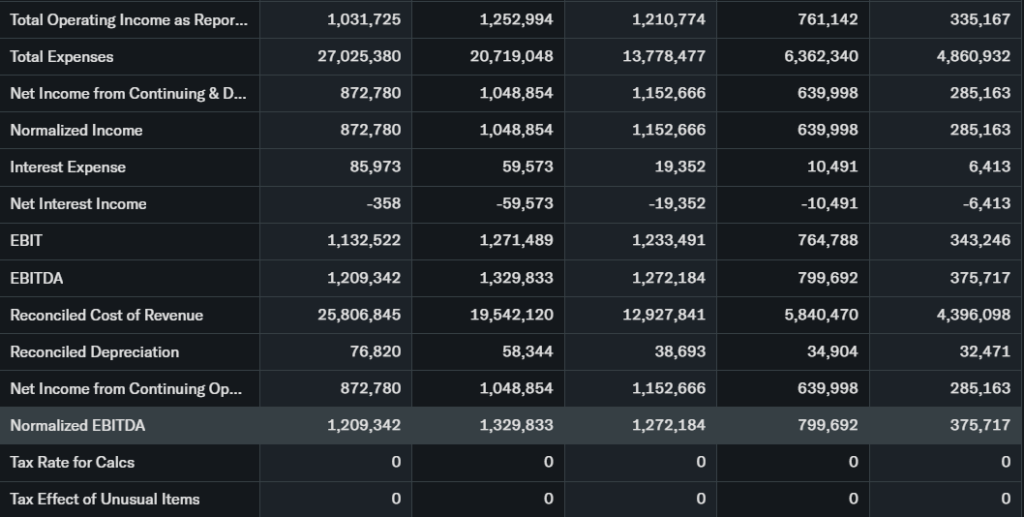

Revenue grew 123% YoY to $12.7B in Q2 FY2026. EPS expanded but faces scrutiny. Free cash flow improved; debt remains low with strong cash from operations.

Compared to peers like Dell or HPE, SMCI trades at a discount on sales but higher on growth expectations. Overall, SMCI stock appears fairly valued—neither cheap nor stretched.

Recent Earnings & Catalysts

Q2 FY2026 revenue hit $12.7B, beating estimates with 123% YoY growth. EPS topped forecasts slightly, driven by AI servers. Guidance reinstated $40B FY2026 revenue.

Gross margins fell to 6.4%, down from Q1 due to supply costs. Stock rose 14% post-earnings on demand strength. Catalysts include NVIDIA partnerships and edge AI launches.

Earnings boosted confidence short-term, but margins weigh on sentiment. Investor events in March 2026 loom large.

Bullish Case

AI server demand fuels revenue catalysts, with $40B FY2026 guidance intact. Market expansion in data centers favors SMCI’s speed-to-market edge.

Tech advantages like liquid-cooled systems cut energy costs. Operational scaling via new factories supports growth without dilution. Steady institutional buying adds tailwinds.

Bearish Case

Competition from Dell, HPE intensifies in AI servers. Margin compression persists at 6.4%, risking profitability.

Customer concentration in few big tech clients raises churn risk. Regulatory scrutiny on governance lingers from 2025. Economic slowdowns could delay capex.

Market Sentiment & Investor Psychology

Short interest hovers moderate at levels signaling caution. Options show balanced calls vs. puts, no extreme bets. Institutional ownership trends up slightly, at key levels.

Retail behavior leans momentum-driven, chasing AI dips. Sentiment mixes neutral to optimistic—fearful on margins, bullish on AI. Value bias grows as P/E dips.

Short-Term Outlook

Technicals point to support at $31 holding firm. Momentum builds if volume spikes above averages. Market breadth in tech supports upside tests at $35.

Expect sideways grind ahead of March events. No major downside unless broader selloff hits.

Medium to Long-Term Outlook

SMCI’s business model shines in AI tailwinds, with strong financials and low debt. Industry growth to $100B+ favors leaders. Competitive moat via customization aids position.

Risks like margins need fixes. Long-term investors should hold core positions; accumulate on dips below $30. Watch execution.

FAQ Section

Is SMCI stock a buy right now?

Hold for most; buy dips if AI demand holds. Analysts lean Hold at $41 target.

What is the price target for SMCI stock?

Average $41.44, high $59, low $27. Upside potential exists.

What are major risks for SMCI stock?

Margins, competition, customer focus. Governance echoes remain.

SMCI earnings outlook?

Q3 due soon; $40B FY guide intact despite pressures.

SMCI long term outlook?

Positive on AI growth; hold for 24 months if margins improve.

Suggestions

- Compare with Opendoor stock analysis

- See our NVIDIA stock forecast

- Read our AI server sector valuation

Conclusion

Hold SMCI stock for now. AI drivers offer upside, but margins and competition demand proof. Technicals stabilize; watch Q3 earnings for buy signals. Long-term potential rewards patience over chasing.

Disclaimer: This article is for informational purposes only and not financial advice.