SMCI stock analysis: Latest price at $31.37, Hold rating, $39-46 forecast amid AI growth risks. Explore SMCI stock price trends, earnings, technical analysis, and buy/hold outlook for 2026 investors.

Introduction

Super Micro Computer designs and builds high-performance servers for AI data centers and cloud computing.

SMCI stock draws attention now due to strong AI server demand despite recent price drops.

Broader tech market volatility hits SMCI stock as investors weigh growth against margin pressures.

Latest Stock Price & Trend

As of last market close on March 16, 2026, SMCI stock price stands at $31.37 after trading between $31.26 and $32.07.

The stock saw a slight dip of about 0.4% in the 1-day performance with volume at 6 million shares.

Over 5 days and 1 month, SMCI stock price shows sideways movement near $31, down from recent highs.

In 3 months, it fell 15% amid broader tech selloffs; 6 months show a 20% decline from AI hype peaks.

Year-to-date in 2026, SMCI stock dropped 27.6%, with 52-week range from $27.60 low to $62.36 high.

This bearish trend signals caution for investors, as slowing momentum tests AI-driven gains.

Technical Analysis

Support levels sit near $30 and $27.60, where buyers may step in to halt further drops.

Resistance looms at $35 and $40, key hurdles for any rebound in SMCI technical analysis.

RSI reading hovers around 40, neutral but leaning oversold, suggesting potential bounce if buying picks up.

MACD shows bearish crossover, indicating downward pressure on SMCI stock price.

The 50-day moving average at $31.42 nears the current price, while 200-day at $41.54 confirms longer-term downtrend.

No golden cross in sight; instead, a death cross earlier points to weakness.

Volume trends stay moderate at 6 million shares daily, lacking conviction for big moves.

Analyst Ratings & Price Targets

Thirteen analysts rate SMCI stock as Hold, with 4 Buys, 7 Holds, and 2 Sells.

Average price target hits $42.38, ranging from $39.53 low to $46.19 high.

Recent notes highlight Q3 2026 guidance beats but note margin risks; no major upgrades lately.

Wall Street firms like those tracked by MarketBeat see balanced SMCI forecast, mixing AI optimism with profitability worries.

This Hold sentiment tells investors to watch execution before chasing gains.

Insider Activity

Recent insider selling outweighs buying, with executives trimming shares amid stock declines.

No large buys reported in Q1 2026; sales align with profit-taking after 2025 peaks.

Management trends show net selling, signaling caution despite AI demand.

This pattern implies tempered confidence, urging investors to probe deeper into SMCI insider activity.

Valuation Analysis

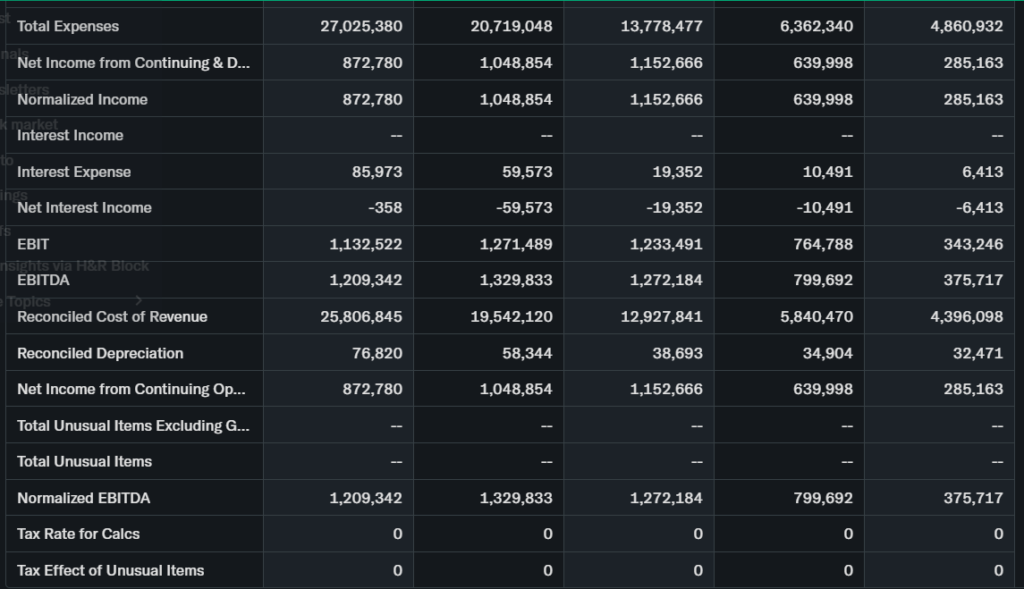

Trailing P/E ratio stands at 23.74, forward P/E around 20 based on growth outlook.

Price-to-sales ratio reflects $28.06 billion trailing revenue against $19.08 billion market cap.

Revenue grew massively YoY, but latest quarter dipped 15.5% to $5.02 billion versus $6.48 billion expected.

EPS hit $1.37 trailing; FY2026 guidance eyes $40 billion sales.

Free cash flow supports operations with current ratio 5.39 and debt-to-equity 0.72; cash buffers risks.

Compared to peers like Dell or HPE, SMCI valuation looks fairly valued, not overvalued despite AI premium.

Recent Earnings & Catalysts

Q2 FY2026 revenue reached $12.7 billion, beating views with EPS at $0.69.

Q3 guidance raised to $12.3 billion revenue and $0.60 EPS, topping $10.2 billion/$0.51 consensus.

But Q4 showed $5.02 billion revenue miss and margin drop to 6.4%.

Forward FY2026 sales target at least $40 billion on AI servers; catalysts include liquid-cooled systems demand.

Earnings beats drove initial rallies, but misses sparked SMCI stock pullbacks.

Bullish Case

AI server demand fuels revenue growth, with $40 billion FY2026 target.

Tech advantages in customizable, efficient systems win data center deals.

Operational scaling and partnerships boost SMCI revenue growth outlook.

Bearish Case

Competition from Dell and HPE squeezes margins, down 310 basis points lately.

Slowing customer spend risks $2.3 billion Q4 revenue drop.

Economic slowdowns and supply chain issues add pressure.

Market Sentiment & Investor Psychology

Short interest remains elevated, reflecting bearish bets.

Options show more puts than calls, signaling caution.

Institutional ownership holds steady, but retail chases momentum less.

Overall sentiment stays neutral, blending AI optimism with valuation fears.

Short-Term Outlook

Technical indicators point to sideways action near support.

Volume lacks surge, so expect consolidation in coming weeks.

Watch RSI for oversold bounce amid tech recovery.

Medium to Long-Term Outlook

Strong AI tailwinds support business model in growing data center space.

Financial health with low debt aids staying power.

Competitive edge in servers favors accumulation for patient investors.

FAQ Section

Is SMCI stock a buy right now?

Hold for now; AI growth tempts but margins worry analysts.

What is the SMCI stock price target?

Average $42.38, with $39-46 range for 2026.

What are major risks for SMCI stock?

Margin compression, revenue misses, and competition top concerns.

What is SMCI earnings outlook?

Q3 guides $12.3B revenue, FY2026 at $40B minimum.

SMCI technical analysis summary?

Bearish MACD, neutral RSI; support at $30.

Suggestion

Compare with Opendoor stock analysis.

See Nvidia stock forecast.

Read AI server sector valuation trends.

Conclusion

Hold SMCI stock for now.

AI demand offers upside, but earnings misses and valuations warrant caution.

Long-term watchers may accumulate on dips.

Disclaimer: This article is for informational purposes only and not financial advice.