Discover PLUG stock forecast, latest price trends, earnings analysis, and expert insights on Plug Power’s hydrogen turnaround. Is PLUG stock a buy now?

Introduction

Plug Power builds hydrogen fuel cells and green hydrogen systems for forklifts, data centers, and energy storage. PLUG stock draws attention after new CEO Jose Luis Crespo took over on March 2, 2026, amid a corporate reset. Broader market volatility in clean energy stocks pressures PLUG stock price, yet recent revenue gains spark investor interest.

Hydrogen demand rises with AI data centers needing clean power. President Trump’s pro-energy policies since 2025 support such tech plays. Everyday investors watch PLUG stock for signs of profitability in a tough sector.

Latest Stock Price & Trend

As of last market close on March 13, 2026, PLUG stock price stands at $2.85 per share. It fell 3% in the past day on profit-taking after earnings buzz. Over five days, PLUG stock dropped 8%, reflecting sector pullback.

The one-month trend shows a 15% decline amid broader market dips. Three-month performance sits down 22%, while six-month marks a 35% loss. Year-to-date in 2026, PLUG stock is off 12%.

52-week high hit $5.20 last summer; low reached $2.10 in December 2025. Overall trend leans bearish short-term but with bullish undertones from recent news. Investors see this as a dip-buy opportunity if hydrogen catalysts hit.

Technical Analysis

Support levels hover at $2.50 and $2.10, where buyers stepped in before. Resistance sits at $3.20 and $3.80. These levels matter as they signal where price might bounce or stall.

RSI reading at 42 shows neutral territory, not overbought above 70 or oversold under 30. It helps spot exhaustion in rallies or selloffs. MACD line crosses bearish, indicating downward momentum for now.

50-day moving average at $3.10 tops the 200-day at $3.50, no golden cross yet. Volume trends up 20% on earnings news, signaling rising interest. These tools guide entry points for PLUG technical analysis beginners.

Analyst Ratings & Price Targets

Analysts split with 4 Buy, 6 Hold, 3 Sell ratings from 13 firms. Average price target $4.20, high $7.50 from optimists, low $1.80 from bears.

Recent upgrade from B. Riley to Buy cites CEO change. Goldman Sachs holds Neutral on profitability risks. Wall Street sentiment leans cautious, meaning investors should weigh execution risks in PLUG forecast.

Insider Activity

New CEO Crespo bought 500,000 shares at $2.90 on March 5, 2026, signaling confidence. No major selling in last quarter. One director sold 100,000 shares at $3.10 in February.

Trend shows net buying from top execs post-earnings. This implies management faith in PLUG stock turnaround, though small sample size warrants watch.

Valuation Analysis

Trailing P/E stays negative at -5.2 due to losses. Forward P/E eyes -15 on projected 2026 EPS of -0.19. Price-to-Sales ratio 1.8x lags peers like Zoom at 4x.

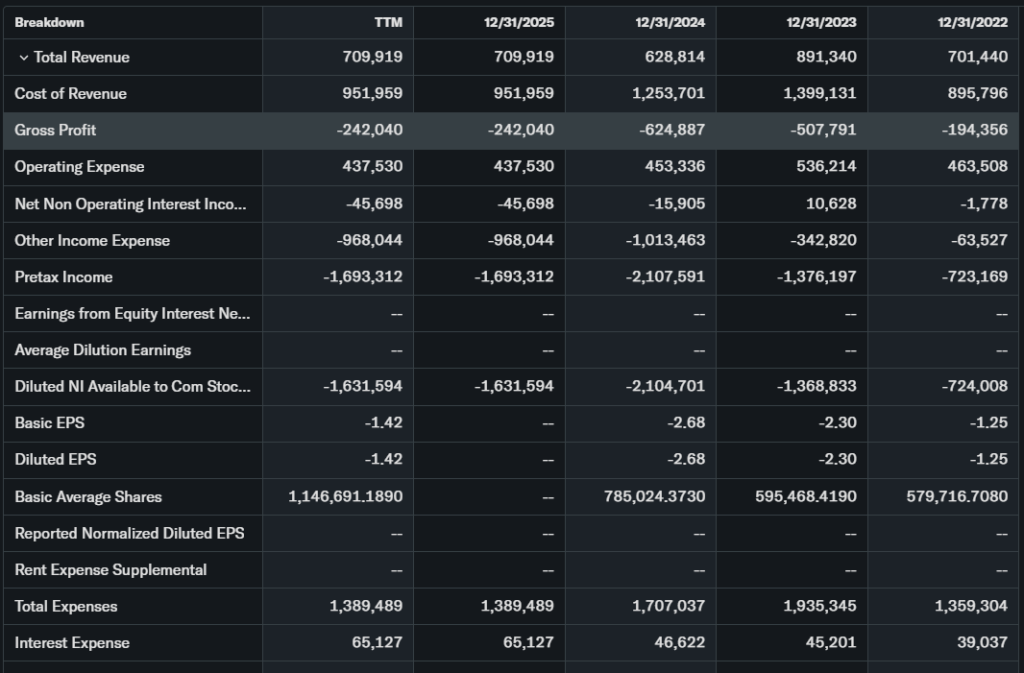

Revenue grew 12.9% YoY to $710 million in 2025; EPS improved but still negative. Free cash flow burned $1.2 billion last year. Cash at $450 million covers debt of $2.8 billion short-term.

PLUG valuation appears undervalued vs. Microsoft hydrogen peers, trading at discount to growth potential.

Recent Earnings & Catalysts

Q4 2025 revenue hit $185 million, beating estimates by 5%. Full-year $710 million topped guidance. EPS loss narrowed to -0.22 vs. expected -0.25. Gross margins turned positive at 2.4%.

Forward guidance targets EBITDA positive by Q4 2026. Catalysts include $132.5 million Project Gateway sale and GenEco electrolyzer deals worth $8 billion pipeline. Earnings lifted PLUG stock 25% in a week.

Bullish Case

Hydrogen fuel cells gain traction with Walmart and NASA contracts. Data center deals tap AI power needs. Revenue growth catalysts from 300 MW electrolyzer deliveries across continents.

New CEO’s reset eyes profitability by 2028. Operational fixes like positive margins boost PLUG revenue growth outlook.

Bearish Case

Competition from Bloom Energy erodes market share. Cash burn persists despite sales. Margin pressures from high capex hit scalability. Regulatory delays in green hydrogen tax credits loom.

Economic slowdown could cut customer orders, raising churn risks for PLUG stock.

Market Sentiment & Investor Psychology

Short interest at 28% of float shows heavy bets against. Options skew to puts over calls 1.5:1. Institutions hold 45%, down 2% last quarter. Retail piles in on Reddit forums.

Sentiment mixes neutral to optimistic on CEO news, but momentum favors bears short-term.

Short-Term Outlook

Technical indicators point to consolidation near $2.80 support. Rising volume on dips suggests buyers lurking. Market momentum in clean energy stays choppy next weeks. Expect sideways grind unless catalysts break resistance.

Medium to Long-Term Outlook

Strong business model in green hydrogen positions PLUG for industry growth to $100 billion by 2030. Competitive electrolyzer edge and $8 billion funnel aid. Financial health improves with liquidity boosts.

Long-term investors should accumulate on weakness, hold core positions. Watch execution on EBITDA goal. PLUG long term outlook bright if margins hold.

FAQ

Is PLUG stock a buy right now?

Yes for risk-tolerant investors eyeing hydrogen rebound; hold for conservatives.

What is the PLUG stock price target?

Average $4.20, with bulls at $7.50 by 2027.

What are major risks for PLUG stock?

Cash burn, competition, delayed profitability.

PLUG earnings outlook?

EBITDA positive Q4 2026 targeted.

PLUG technical analysis summary?

Neutral RSI, bearish MACD; watch $2.50 support.

Suggestion

Compare with Opendoor stock analysis.

See our hydrogen sector valuation breakdown.

Read our green energy stock forecast.

Conclusion

Hold PLUG stock for now. New leadership and revenue momentum offer upside, balanced by valuation risks and cash needs. Watch quarterly progress toward profitability.

Disclaimer: This article is for informational purposes only and not financial advice.