Get a clear look at PLTR stock price, technical analysis, earnings, and forecast. Is PLTR stock a buy in 2026? Balanced view on Palantir’s AI growth.

Introduction

Palantir Technologies builds software that helps governments and companies analyze data and deploy AI. Its platforms, like Gotham, Foundry, and AIP, power defense, intelligence, and commercial decision-making. Investors are focused on PLTR stock because Palantir has shifted from a story stock to a profitable AI leader with fast-growing U.S. commercial revenue.

At the same time, tech markets remain volatile as rates stay elevated and AI names see sharp swings. High‑growth software and AI stocks like PLTR move quickly when expectations change. This makes understanding PLTR stock price, PLTR earnings, and valuation more important for long‑term investors.

Latest Stock Price & Trend

Palantir stock price was about 134.43 USD at the close on February 25, 2026, giving the company a market cap near 321.5 billion USD. During that session, PLTR traded between 128.61 USD and 136.09 USD, finishing slightly below the intraday high and above the low.

Over the last 5 days, PLTR stock has traded in a range roughly between 126–136 USD, with modest net movement as the stock consolidates after a sharp pullback. In the past month, PLTR dropped from a high near 170.59 USD on January 26, 2026, to the low‑130s, a decline of about 23% from that recent peak.

Looking back three months, PLTR is down about 34% from the high of 198.88 USD in late December 2025. Over six months, it has fallen roughly 37% from the 52‑week high of 207.52 USD set in early November 2025. However, the longer‑term picture still shows massive appreciation: the 52‑week low was 66.12 USD, and the two‑year low near 20.33 USD means the stock is still up several hundred percent over that period.

Year‑to‑date, PLTR is trading around 30% below its early‑January high of 187.28 USD, reflecting a cooling of AI enthusiasm after a huge 2025 run. Overall, the current trend is short‑term bearish to sideways after a steep correction, but long‑term bullish versus 2024–2025 levels. For investors, this suggests the stock has transitioned from euphoria to consolidation, where fundamentals will matter more than hype.

Technical Analysis

From a technical analysis view, PLTR stock currently trades above its key long‑term lows but well below its recent highs. Short‑term traders watch support near the low‑130s and in the high‑120s, where buyers previously stepped in, while resistance appears in the mid‑130s to 140 range in the near term and around 170 longer term. Support levels are price zones where demand often stops further declines; resistance is where selling pressure tends to cap rallies.

The RSIfor PLTR is around 32–33, which is close to the lower end of the neutral band and edging toward “oversold” territory . This suggests the selling pressure has been strong, but the stock is not yet deeply oversold, leaving room for either a bounce or further consolidation. RSI helps investors see when a move may be stretched.

The MACD line is above the signal line, which indicates bullish momentum despite the recent pullback. A MACD above its signal can point to a potential trend reversal upward, especially after a correction. For PLTR, this hints that buyers may be regaining control after the early‑year slide.

Importantly, the 50‑day moving average remains above the 200‑day moving average, which is a classic bullish configuration and means there is no “death cross” on the chart. When the 50‑day sits above the 200‑day, it usually reflects a longer‑term uptrend still intact, even if the stock is correcting. Volume has been strong, with tens of millions of shares trading daily, showing high investor interest and good liquidity.

Overall, PLTR technical analysis currently shows long‑term bullish structure with short‑term weakness, a setup often watched by investors waiting for stabilization before adding.

Analyst Ratings & Price Targets

Analyst coverage of PLTR stock has improved as the company has proven it can grow revenue and generate profits. According to a recent forecast summary, around 20 analysts track the stock, with a consensus rating of “Buy”. The average 12‑month price target is about 187.95 USD, implying upside of roughly 46% from the current price in the mid‑130s.

Price targets range widely: the low estimate around 50 USD implies substantial downside if growth slows, while the high estimate near 260 USD suggests more than 100% upside if Palantir executes well and AI demand stays strong. The median target is close to 198 USD, again signaling that many on Wall Street see PLTR stock as undervalued relative to its growth prospects after the recent correction.

Major firms highlight Palantir’s accelerating U.S. commercial business, strong government demand, and high‑margin software model, but they also flag valuation risk after the big 2025 run. In plain terms, analyst sentiment leans positive but cautious: PLTR earnings momentum is real, yet the stock still carries a premium valuation that requires continued execution.

Insider Activity

Insider activity can reveal how management feels about the company’s future. Over the last reported period covering 100 recent trades, Palantir insiders bought about 3.42 million shares and sold about 3.54 million shares, resulting in a slightly negative “insider power” score of -1.95.

The data shows many routine sales linked to stock options by senior executives such as Alexander Moore and Eric Woersching, together with smaller open‑market buys by insiders including Ryan Taylor and Jeffrey Buckley. This pattern resembles typical tech‑company behavior where compensation includes stock, rather than a clear “all‑in” or “running for the exits” message.

Net, recent PLTR insider activity is slightly net‑selling but not extreme, which suggests neutral to mildly cautious insider sentiment. Investors should treat this as one piece of the puzzle rather than a decisive signal.

Valuation Analysis

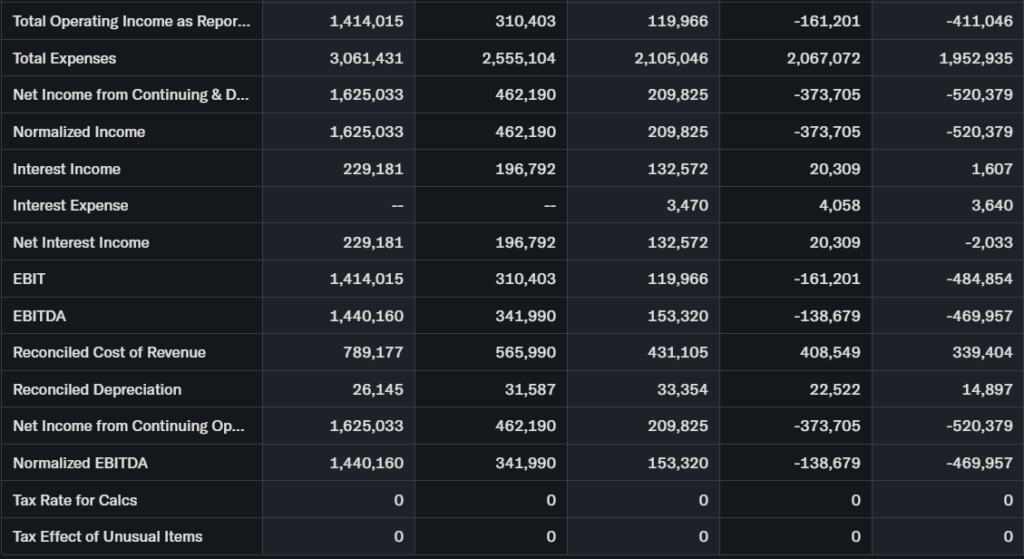

Palantir’s valuation reflects both its rapid growth and the market’s willingness to pay for AI exposure. Based on recent statistics, Palantir generated about 4.48 billion USD in trailing twelve‑month revenue, up roughly 56% year over year, and 1.63 billion USD in net income, up about 252%. EPS rose to around 0.63 USD, more than tripling.

At the current stock price near 134–135 USD and a market cap above 300 billion USD, PLTR trades at a very high trailing P/E ratio above 200 and an elevated price‑to‑sales multiple relative to many traditional software names. However, those multiples are attached to a business delivering GAAP net margins near 35–40% and very strong free‑cash‑flow margins, as seen in Q3 2025 results where GAAP net income reached 476 million USD, with operating cash flow of 508 million USD and adjusted free cash flow of 540 million USD.

Compared with mega‑cap software or AI‑adjacent names like Microsoft or Salesforce, Palantir’s multiples are higher, but its revenue growth and margin expansion are also faster at this stage. Relative to other high‑growth AI infrastructure or data‑platform plays, PLTR sits toward the expensive end of the spectrum based on metrics like EV/sales and PEG, which some independent analyses highlight as a key risk.

Putting this together, PLTR stock currently appears richly valued to slightly overvalued on classic metrics, but the premium is partly justified by strong growth and scalability. For new investors, this means the story is attractive, but the entry price still matters.

Recent Earnings & Catalysts

Palantir’s latest reported quarter (Q3 2025) showcased why the market is willing to pay a premium. Total revenue grew 63% year over year, with U.S. commercial revenue up 121%, reflecting rapid adoption of its AIP and Foundry offerings by corporate customers.

GAAP net income in Q3 2025 was about 476 million USD with a 40% margin, while operating cash flow reached 508 million USD (43% margin) and adjusted free cash flow 540 million USD (46% margin). GAAP EPS came in at 0.18 USD, with adjusted EPS at 0.21 USD, beating many prior expectations. Management also raised full‑year 2025 revenue guidance to 53% year‑over‑year growth, and guided Q4 revenue growth around 61%, again well ahead of consensus at the time.

Key catalysts include continued expansion of U.S. commercial clients, new government contracts, and deeper integration of AIP in defense and enterprise AI workflows. The company is also leaning into partnerships and product improvements that make its platforms easier to deploy. These strong PLTR earnings and raised guidance helped fuel much of the 2025 stock rally, though the subsequent valuation reset in early 2026 shows that even beats can be followed by profit‑taking.

Bullish Case

The bullish case for PLTR stock centers on several concrete drivers:

Explosive U.S. Commercial Growth: Revenue in that segment more than doubled year on year, showing that Palantir is no longer just a defense contractor—it is becoming a mainstream enterprise software and AI platform provider.

High‑Margin, Scalable Model: With net income and free‑cash‑flow margins above 40% in recent quarters, Palantir has room to invest heavily while still generating cash. This is unusual for a company still growing revenue at 50%+ annually.

Unique Positioning in AI & Defense: Palantir’s deep ties with governments, coupled with its AI‑driven decision platforms, create a moat that is difficult for generic cloud or analytics vendors to match, especially in sensitive national security contexts.

If these drivers persist, PLTR stock forecast models that call for double‑digit annual growth and expanding profits could be realistic, and the current dip might look attractive in hindsight.

Bearish Case

On the other side, the bearish case focuses on valuation and execution risk:

Sky‑High Valuation Metrics: Analyses highlight that Palantir’s PEG, EV/sales, and EV/EBITDA multiples sit well above industry averages and above its own three‑year norms. This suggests the stock has become expensive relative to its projected growth, increasing the risk of a sharp correction if growth slows.

Concentration & Political Risk: Palantir is heavily exposed to government and defense spending cycles, which are subject to budget changes and political scrutiny. Any major contract loss or regulatory pushback on data/AI use could hurt growth.

Competition in Enterprise AI: Big cloud providers and large software players are all pushing AI platforms. If enterprises choose easier‑to‑integrate or cheaper alternatives, Palantir’s commercial growth could decelerate faster than the market currently expects.

Taken together, these issues mean that while the business is strong, PLTR stock could still be vulnerable if expectations get ahead of reality.

Market Sentiment & Investor Psychology

Market sentiment around PLTR stock is shaped by its AI narrative, strong results, and volatile price history. Short‑interest data shows a short interest ratio around 1.0, which is relatively low and indicates no widespread large bearish positioning at the moment.

Institutional investors have built sizable positions in Palantir, and ownership is broad among funds, suggesting that the name is now part of many growth and AI portfolios. Retail investors also remain active in PLTR, drawn by its long‑term story and large price swings that create trading opportunities.

Options trading and online commentary show a mix of momentum and long‑term holders, with some investors treating PLTR as a core AI holding and others viewing it as a high‑beta trading vehicle. Overall, sentiment looks cautiously optimistic: the excitement of 2025 has cooled, but most large holders still expect further growth rather than collapse.

Short-Term Outlook

In the short term, PLTR stock is likely to be driven by technicals and news flow more than by new fundamentals. With RSI near the low‑30s, the stock is close to oversold on a momentum basis, while MACD remains in a bullish position relative to its signal line.

That mix often leads to choppy trading with potential for short squeezes or sharp bounces, especially if broader tech markets stabilize or new contract announcements hit the tape. However, until the price can reclaim prior resistance levels in the 150–170 range, traders should assume volatility will remain high and that rallies may be met with profit‑taking.

Medium to Long-Term Outlook

Over a 6–24 month horizon, the key question is whether Palantir can sustain high growth while preserving its newly achieved profitability. The business model is strong: recurring software revenue, high switching costs, and expanding use cases in both government and commercial markets.

The AI and data‑analytics industry is expected to grow rapidly, and Palantir is well positioned as a specialized player rather than a general‑purpose cloud. Financially, the company has moved from years of losses to substantial net income and free cash flow, which gives it flexibility for R&D and strategic deals.

If management continues to execute and the macro backdrop remains supportive for tech, PLTR stock could justify its current valuation and potentially grow into it. For long‑term investors, PLTR looks like a “Hold with a bias to accumulate on meaningful pullbacks”, especially for those comfortable with AI and defense exposure.

FAQ Section

- Is PLTR stock a buy right now?

Analysts currently rate PLTR stock as a Buy on average, with strong revenue and earnings growth, but the valuation remains elevated. Investors with higher risk tolerance may see it as a buy on dips; more conservative investors might prefer to hold and wait for better entry points. - What is the price target for PLTR stock?

The average 12‑month PLTR stock price target is about 187.95 USD, implying roughly 46% upside from the recent mid‑130s price. The lowest target is near 50 USD, and the highest is around 260 USD. - What are major risks for PLTR stock?

Key risks include high valuation, potential slowdown in commercial growth, heavy reliance on government and defense contracts, regulatory and political scrutiny, and strong competition from large enterprise and cloud providers. - How strong are recent PLTR earnings?

Recent PLTR earnings have been very strong: Q3 2025 revenue grew 63% year over year, U.S. commercial revenue rose 121%, and GAAP net income reached 476 million USD with robust free‑cash‑flow margins.

- What is the long‑term outlook for PLTR stock?

If Palantir maintains high growth and high margins, and continues to win government and commercial AI work, the long‑term outlook is positive. However, returns will depend on starting valuation and investors’ time horizon.

Suggestions

You can use internal links like:

“Compare with Opendoor stock for a different software growth profile”

“See our Microsoft stock forecast for a mature AI leader”

“Read our tech sector valuation breakdown to understand current multiples”

Final Balanced Conclusion

Putting everything together, PLTR stock sits at the intersection of strong fundamentals and demanding valuation. Revenue and earnings are growing quickly, margins are high, and Palantir is becoming a core player in AI‑driven software for governments and enterprises. At the same time, the stock still trades at rich multiples and has already delivered huge gains from its 2024 lows.

A balanced view is that PLTR is a Hold for existing shareholders and a selective buy on pullbacks for long‑term investors who understand the risks of premium‑priced AI names. Position sizing and patience are crucial given the volatility.

Disclaimer: This article is for informational purposes only and not financial advice.