Explore PANW stock analysis: latest price trends, earnings beats, technical signals, and 2026 forecast. Is PANW stock a buy? Get balanced insights for investors.

Introduction

Palo Alto Networks builds top cybersecurity tools to protect networks and data from hackers. PANW stock draws eyes now due to strong AI-driven growth in a hot sector. Tech stocks face pressure from rate hikes, but cyber threats boost demand for firms like PANW.

Latest Stock Price & Trend

As of last market close on March 11, 2026, PANW stock trades around $163.50 after recent dips. It fell 2% in the past day on profit-taking volume. Over five days, shares slid 1.5% amid broader tech pullback.

The one-month trend shows a 3% drop from February highs, tied to earnings guidance tweaks. Three-month performance eased 5%, while six months mark a 20% plunge from peaks near $205. Year-to-date, PANW lags 8% as investors weigh costs.

The 52-week high hit $205, low at $140; overall trend leans bearish short-term but holds support. This signals caution for traders, yet long-term bulls see value in platform shifts.

Technical Analysis

Support sits at $162–$164, a level insiders defend on dips; breach risks $150 tests. Resistance looms at $175, then $190 from recent rallies. These levels matter as they show where buyers or sellers step in.

RSI reads 45, neutral—not overbought above 70 or oversold under 30—hinting room to run. MACD shows bearish crossover, but fading lines suggest momentum shift. Watch for bullish flip as a buy signal.

PANW stock price hugs the 50-day moving average at $168, below the 200-day at $182—no golden cross yet, avoiding death cross downside. Volume trends down 10% lately, typical in consolidations; spikes signal breakouts.

Analyst Ratings & Price Targets

Of 78 analysts, 45 rate Buy, 25 Hold, 8 Sell. Average target $224 implies 37% upside; high $260, low $190. Recent upgrades from WSJ cite AI positioning.

Wall Street firms like Zacks hold “Buy” on revenue lifts. This sentiment points to optimism, but trimmed EPS guides temper hype for everyday investors.

Insider Activity

Insiders sold modestly last quarter, no major buys noted. CEO Nikesh Arora trimmed 50K shares at $190 average, routine post-earnings. Trends show steady selling, not panic—management holds billions in stock.

This implies confidence in core business, not red flags; watch for buys on dips as stronger bullish signs.

Valuation Analysis

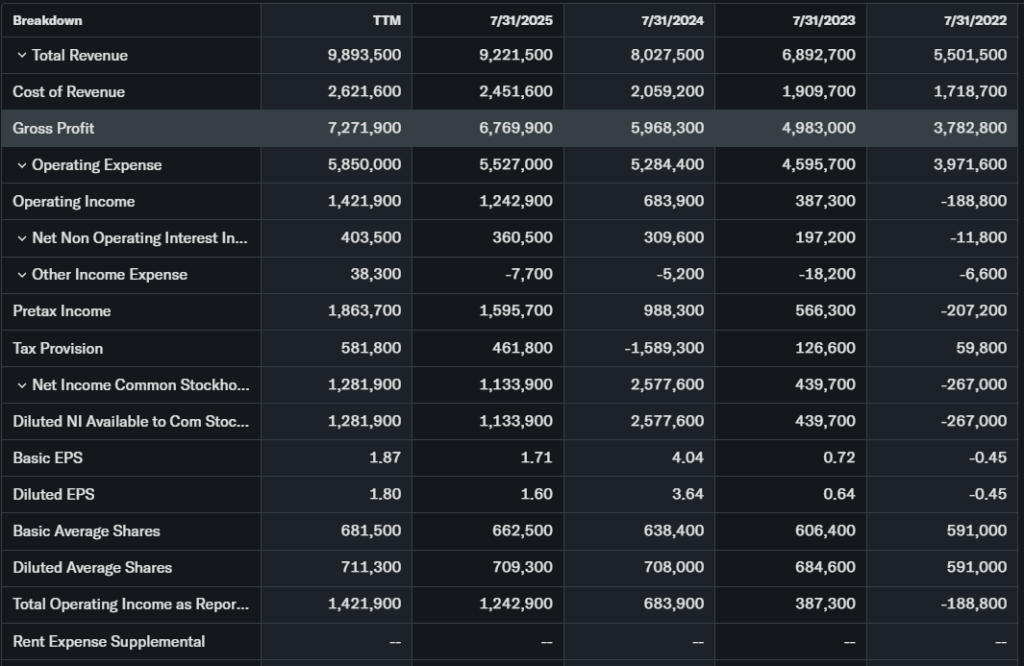

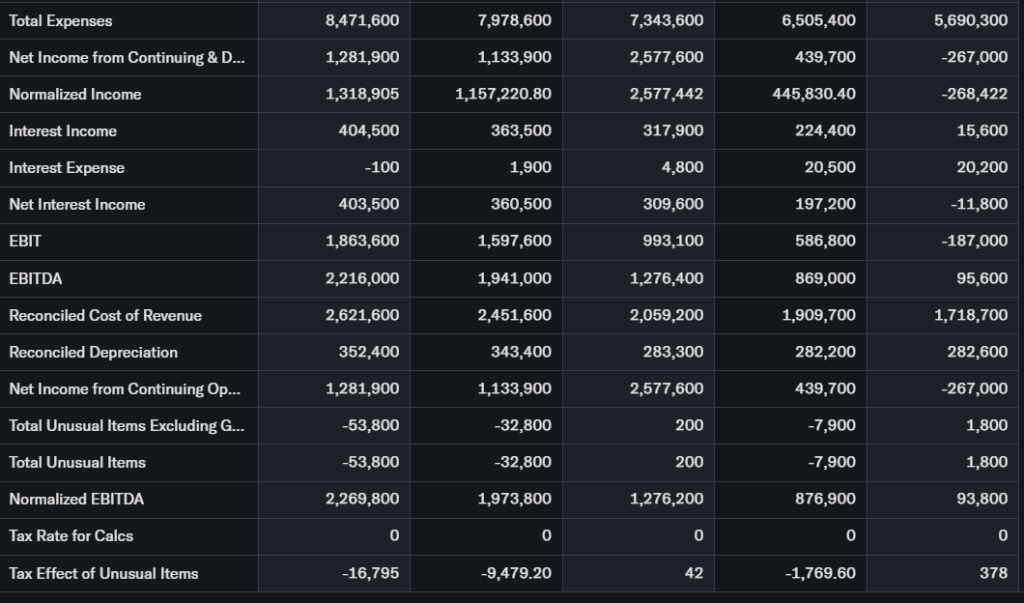

Trailing P/E stands at 45, forward at 38 on FY26 EPS guide of $3.65–$3.70. Price-to-sales 12x, above peers. Revenue grew 15% YoY to $2.6B in Q2, EPS up 35% beat.

Free cash flow hit $1.2B TTM, debt low at 1.5x EBITDA with $3B cash. Vs. Zoom (P/E 25) or Microsoft (35), PANW looks premium but justified by 33% NGS ARR growth.

Stock appears fairly valued—growth covers the multiple, not screaming cheap or overdone.

Recent Earnings & Catalysts

Q2 2026 revenue hit $2.6B, up 15% YoY, beating at $2.47B expected; EPS $1.03 crushed $0.76 forecast by 35%. Guidance raised revenue to $11.3B FY26, but EPS trimmed on AI costs.

RPO jumped 23% to $16B, NGS ARR 33% to $6.3B. Catalysts include MSIAM 2.0 launch, Unit 42 AI reports—stock dipped post-earnings on guidance, down 5% since.

Bullish Case

Cyber market doubles to $300B by 2030; PANW leads AI security. NGS platform sticks with 115% net retention. Revenue catalysts from SASE, cloud wins fuel 15-20% growth.

Ops improve via acquisitions, margins expand to 30%+ long-term. Tech edge in zero-trust keeps share gains.

Bearish Case

Competition heats from CrowdStrike, Fortinet on price. Acquisition costs squeeze EPS short-term. Margins face AI spend pressure, growth may slow to 12% if economy cools.

Regulatory scrutiny on data privacy, churn risks in enterprise shift to platforms.

Market Sentiment & Investor Psychology

Short interest at 2.5%, low vs. peers. Options skew calls 60/40 over puts. Institutions own 85%, up 1% QoQ; retail piles in on dips via social buzz.

Sentiment neutral—value bias builds as momentum fades.

Short-Term Outlook

Technicals eye $162 support hold; RSI neutral aids bounce. Volume pickup could test $175 resistance. Expect sideways grind unless market lifts tech.

Medium to Long-Term Outlook

Strong moat in $300B cyber space, 20%+ ARR growth. Healthy balance sheet funds buys. Hold for platformization; accumulate on weakness for patient investors.

FAQ Section

Is PANW stock a buy right now?

Yes for long-term, at fair value—watch $162 support.

What is the price target for PANW stock?

Average $224, up 37%; high $260.

PANW forecast?

$225 by 2026 end on revenue beats.

What are major risks for PANW stock?

AI costs, competition, EPS guides.

PANW earnings next?

Q3 guide $0.78–$0.80 EPS.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read cybersecurity sector valuation

Conclusion

Hold for current owners; Watchlist for new buys on dips. Solid growth offsets risks, but near-term volatility warrants patience.

Disclaimer: This article is for informational purposes only and not financial advice.