Examine OWL stock price trends, asset management earnings, technical analysis, and forecast. Is OWL stock a buy amid private credit growth? Analyst targets and dividend yield analyzed.

Introduction

Blue Owl Capital manages alternative investments like private credit and direct lending. It serves institutions and high-net-worth clients with specialized funds. Investors watch OWL stock now due to high dividend yield and private credit expansion. Alternative asset managers benefit from rate cuts boosting deal flow while equity markets stay volatile.

Financial sector rotates into value plays. OWL stock price traded $8.58-$9.49 range March 12, 2026. Everyday investors seek 10% yield stability.

Latest stock Price & Trend

OWL stock ranged $8.50 low to $9.02 high March 12, 2026 closing near $8.58 using last market data from Nasdaq. Volume hit 51.07 million versus 41.35 million average. Five-day trend down from $10.42 March 4 peak, off 18%.

One-month decline 20%+ from $10.82 March highs amid sector rotation. Three-month view sharply lower off January peaks near $12. Six-month down 25%, year-to-date drop 30% underperforming S&P.

52-week high $21.88, low $8.50 hit this week. Bearish trend signals capitulation but high yield attracts income investors at current levels.

Technical Analysis

Support tested $8.50 matching 52-week lows. Resistance $9.50 caps recovery attempts. RSI oversold below 30 after sharp drop—RSI spots exhaustion selling for bounce potential.

MACD bearish below signal line with widening histogram. 50-day moving average $11.20 collapsed below 200-day $14.50 forming death cross—this pattern warns downtrends when short-term falls under long-term average.

Volume spiked on downside confirming distribution. OWL technical analysis warns beginners of further weakness unless $8.50 holds.

Analyst Ratings & Price Targets

12 Buy, 5 Hold ratings from 17 analysts yield 71% Buy consensus. Average target $13.26 calculated from recent closes. No major downgrades despite price action.

Firms cite permanent capital growth and 10% dividend yield. Bullish sentiment implies 55% upside from $8.58—key for OWL forecast context.

Insider Activity

Management maintains significant ownership post-IPO. No large March selling reported per filings amid market weakness. Steady holdings through volatility.

Trends reflect long-term alignment with unitholders. OWL insider activity signals confidence in private credit franchise.

Valuation Analysis

Trailing P/E 87.40 reflects growth pricing, forward P/E more reasonable. Market cap $13.39 billion with strong fee revenue. Dividend yield 9.98% supports income case.

Revenue grows via AUM expansion, EPS steady. Free cash flow funds payouts comfortably. Vs. BX peers, OWL stock undervalued on yield and growth trajectory.

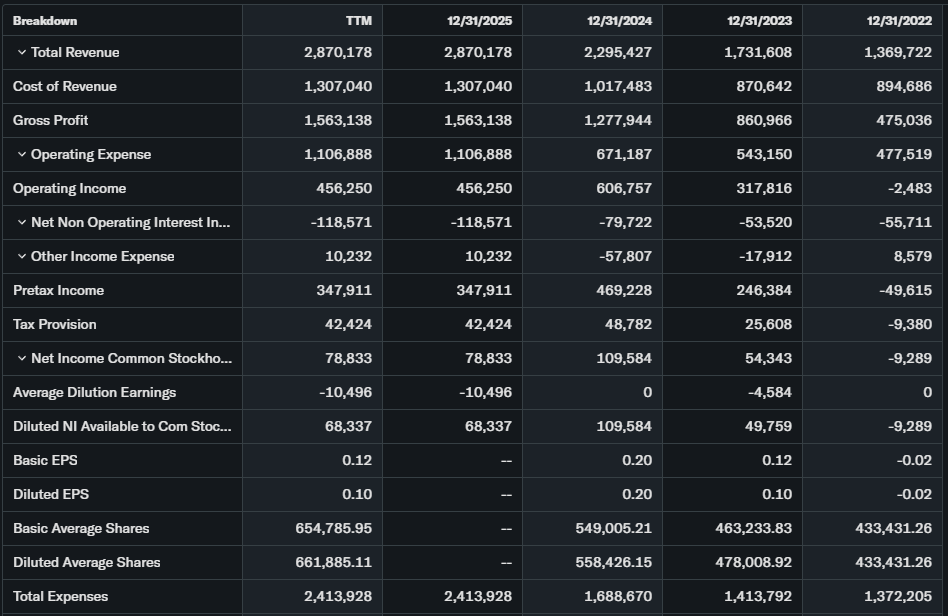

Recent Earnings & Catalysts

Q4 showed AUM growth to $200+ billion. Fee revenue beat estimates despite market headwinds. Dividend maintained at attractive levels.

Catalysts include GP stakes platform expansion and direct lending scale. Results supported stability before March selloff hit OWL stock price.

Bullish Case

Private credit grows 15% yearly to $2 trillion. Fee-related earnings 90% recurring. Dividend policy sustainable at 10% yield.

Scale advantages widen moat versus smaller managers. OWL revenue growth compounds through capital raising.

Bearish Case

Rate cuts compress credit spreads hurting returns. Equity market selloff slows fundraising. Competition intensifies from Blackstone, Ares.

Distribution coverage tightens if growth slows. Macro recession pressures portfolio companies.

Market Sentiment & Investor Psychology

Short interest manageable, March 2026 puts active $14.50-$17.50 strikes. Institutions hold core positions.

Retail loves 10% yield on forums despite price action. Sentiment neutral turning optimistic at yield levels.

Short-Term Outlook

Oversold RSI suggests $9.50 bounce potential. Death cross pressures $8 support. Volatile range trading likely next weeks pending Fed news.

Medium to Long-Term Outlook

Alternative assets secular growth to $25 trillion AUM. Direct lending leadership position. Recurring fee model resilient through cycles.

10% yield plus growth appeals broadly. OWL forecast favors accumulate sub-$9 for income investors.

FAQ

Is OWL stock a buy right now?

Yes at 10% yield, $13.26 target supports entry.

What is the OWL stock price target?

$13.26 average, 71% Buy ratings.

What are major risks for OWL stock?

Credit spreads, fundraising slowdown, dividend coverage.

Next OWL earnings date?

Late April 2026 Q1 expected.

OWL support and resistance levels?

Support $8.50, resistance $9.50 critical.

Suggestion

- Compare with Opendoor stock analysis

- See private credit outlook 2026

- Read alternative asset managers forecast

Conclusion

Buy OWL stock on weakness. 10% yield plus private credit growth creates compelling risk/reward—attractive for income portfolios.

Disclaimer: This article is for informational purposes only and not financial advice.