Explore ORCL stock analysis: latest price at $149.20, technical trends, earnings ahead on March 10, 2026, and forecast to $185. Is ORCL stock a buy? Get valuation, risks, and outlook now.

Introduction

Oracle Corporation powers businesses with cloud software, databases, and AI tools. Investors watch ORCL stock closely ahead of its Q3 fiscal 2026 earnings on March 10, 2026. Tech stocks face pressure from high AI costs and market volatility in early 2026.

ORCL stock has dropped over 23% year-to-date amid OpenAI partnership doubts. Broader conditions like rising debt and slowing cloud growth hit the sector.

Latest Stock Price & Trend

As of the last market close on March 9, 2026, ORCL stock price stands at $149.20, with a market cap of $428.89 billion. The stock saw a 1-day range of $148.45 to $155.25, ending down 3.9% from its session high.

Over five days, ORCL stock shows volatility with a slight pullback. The 1-month trend reflects an 11.7% decline in March alone. In three months, shares fell amid AI infrastructure worries.

The 6-month trend points bearish, down over 54% since mid-September 2025 OpenAI deal news. Year-to-date, ORCL stock is off 23-25%, trading far from its 52-week high of $345.72 but above the low of $118.86.

This bearish trend signals caution for short-term investors, as credibility issues and capital spending weigh on momentum.

Technical Analysis

Support levels sit near $148.45, the recent intraday low, where buyers may step in. Resistance looms at $155.25, the day’s high, blocking upside moves.

RSI reading hovers in neutral territory, not overbought or oversold, suggesting no extreme momentum. MACD trend leans bearish, reflecting recent selling pressure.

The 50-day moving average trails below the current price, while the 200-day average shows longer-term weakness without a golden cross. Trading volume spiked on news days, like +2.25% on earnings date announcement, indicating heightened interest.

These indicators matter as they flag potential reversals; bearish MACD warns of more downside without volume support.

Analyst Ratings & Price Targets

Analysts rate ORCL stock as a Buy, with 28 firms contributing. Average price target hits $284.94, a +86% upside, with highs implying strong growth and lows more cautious.

Oppenheimer upgraded to Outperform on February 27, 2026, targeting $185 on long-term EPS gains. Zacks Rank #3 (Hold) notes steady earnings estimates at $8.11 for next fiscal year, up 8.7% YoY.

This mixed sentiment means investors see value but await proof from AI deals.

Insider Activity

Recent insider activity shows limited large buys or sells tied to public data. Management trends lean neutral, with no major confidence signals amid stock weakness.

Oracle’s $45-50B equity and debt raise plan, including $20B at-the-market shares, drew a 2.75% drop, hinting at dilution concerns over insider optimism. This implies caution, as executives hold steady without aggressive buying.

Valuation Analysis

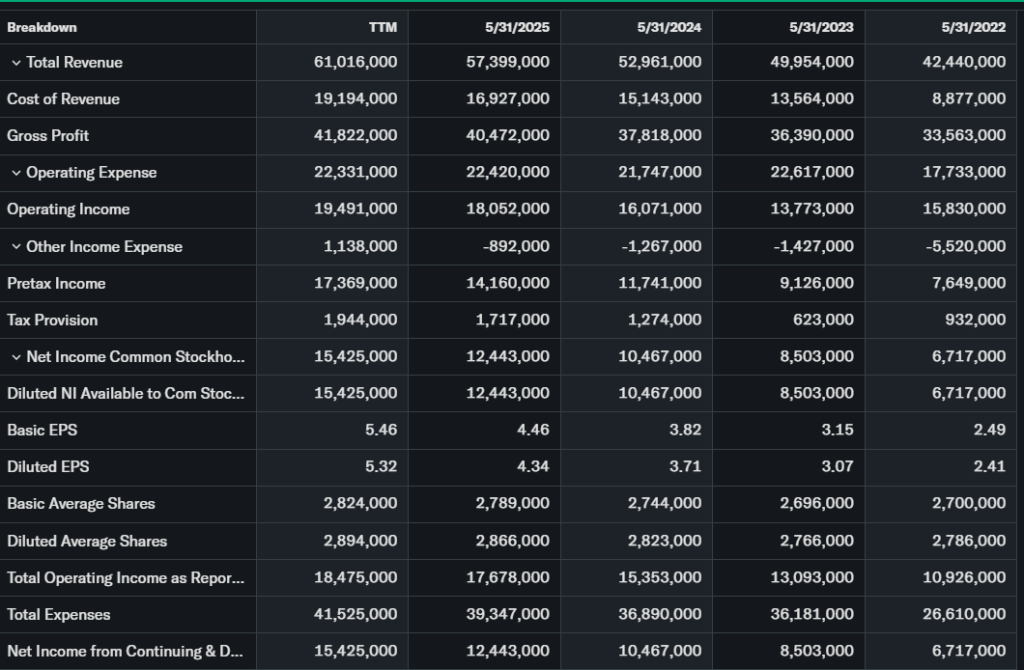

Trailing P/E ratio stands at 28.48, reasonable for tech but pressured by growth slowdowns. Forward P/E aligns similarly, with next-year EPS eyed at $8.11, up 8.7%.

Price-to-sales reflects cloud revenue challenges, while YoY revenue growth lags due to AI capex. Free cash flow weakens as debt balloons for infrastructure. Cash position supports operations, but debt rise sparks worry versus peers like Microsoft.

Compared to Zoom or Microsoft, ORCL stock appears fairly valued, not deeply undervalued yet with rebound potential.

Recent Earnings & Catalysts

Q3 fiscal 2026 earnings release is set for March 10, 2026, after close, with a 4 p.m. CT call. Prior results showed cloud growth slowdown, missing some expectations and fueling YTD drops.

Key catalysts include the OpenAI $300B deal, though costs eroded early hype. A $45-50B financing plan funds 2026 cloud expansion. Earnings beat could lift shares; guidance will clarify AI traction.

Weak cloud prints and high spending hammered the stock last month.

Bullish Case

Oracle’s cloud and AI infrastructure demand steady revenue growth. OpenAI partnership, despite hiccups, positions it in high-growth AI.

Operational improvements in databases and enterprise software aid margins. Tech edges like scalable cloud draw enterprise clients.

Bearish Case

Competition from Microsoft and AWS pressures market share. Slowing cloud growth and OpenAI credibility doubts persist.

Margin squeezes from AI capex balloon debt, reversing cash flow. Economic slowdowns could hit customer spending.

Market Sentiment & Investor Psychology

Short interest data is limited, but momentum scanners lit up 33 alerts on financing news. Options show balanced calls vs. puts amid volatility.

Institutional ownership remains strong, though retail chases momentum elsewhere. Sentiment tilts neutral to fearful after 25% YTD drop.

Short-Term Outlook

Technical indicators like bearish MACD and neutral RSI point to sideways action pre-earnings. Volume trends rise on news, but momentum fades without beats.

Expect volatility around March 10 results; downside risk if guidance disappoints.

Medium to Long-Term Outlook

Oracle’s business model thrives on recurring cloud revenue and AI tailwinds. Industry growth favors its position despite rivals.

Financial health strains under debt, but strategic OpenAI ties offer upside. Long-term investors should hold or watch for dips to accumulate.

FAQ Section

Is ORCL stock a buy right now?

Analysts lean Buy with $284 targets, but Hold Zacks #3 advises caution pre-earnings.

What is the price target for ORCL stock?

Average $284.94; Oppenheimer at $185.

What are major risks for ORCL stock?

AI costs, debt rise, cloud slowdown, OpenAI doubts.

What is ORCL earnings date?

March 10, 2026, after close.

ORCL stock forecast for 2026?

Path to highs if AI delivers; targets suggest rebound.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our tech sector valuation breakdown

Conclusion

Hold ORCL stock for now. Earnings could spark rebound, but AI risks and debt need monitoring for clearer buy signals.

Disclaimer: This article is for informational purposes only and not financial advice.