Explore ONDS stock forecast with the latest price trends, earnings beats, and analyst targets. Is ONDS stock a buy amid 2026 growth outlook? Get technical analysis now.

Introduction

Ondas Holdings Inc. builds autonomous drone systems and robotics for defense and industry. ONDS stock draws eyes after a 22% monthly drop despite strong backlog growth. Broader market volatility in tech hits small caps hard as rates linger high.

Investors watch ONDS stock price for signs of recovery in unmanned systems demand. Recent M&A and cash raises fuel debate on near-term dips versus long-term gains.

Latest Stock Price & Trend

ONDS stock closed at $2.13 as of last market data on March 14, 2026. It fell 10.8% over the past downtrend from February 19.

The 1-day change shows minor pullback amid volume drops hinting at rebound potential. Five-day trend stays neutral with average turnover at 962 million shares. One-month slide hit 22% while the sector gained 8.7%.

Over three months, ONDS stock price eased from peaks after 2025 gains. Six-month view reflects expansion but recent pressure. Year-to-date, shares lag amid transition costs. The 52-week high sits near prior highs, low at lower supports. Overall trend leans bearish short-term but bullish on fundamentals.

This signals caution for traders yet opportunity for patient investors eyeing backlog surge.

Technical Analysis

Support levels rest near $2.02, a key floor if selling persists. Resistance looms at $2.63, where sellers may cap gains. These levels matter as they show where buyers or sellers step in to shift momentum.

RSI reading nears neutral, avoiding overbought or oversold extremes. ONDS RSI analysis points to consolidation after downtrend. MACD trend shows sell signals but fading volume suggests bullish reversal soon.

The 50-day moving average trails the 200-day, no golden cross yet—death cross avoided. Trading volume trends down recently, often preceding bounces. ONDS technical analysis favors neutral mid-term outlook for beginners.

Analyst Ratings & Price Targets

Ten analysts cover ONDS stock with mixed views. Eight provide estimates leaning toward hold amid growth bets. Average price target hits $2.13, high at $2.63, low $2.02.

No major upgrades lately, but sentiment ties to earnings on March 25. Wall Street sees revenue upside but flags expenses. ONDS price target reflects balanced outlook.

This means investors get cautious optimism—growth potential tempers transition risks.

Insider Activity

Recent insider activity stays quiet post-M&A deals. No large buys or sells flagged in latest SEC data. Management focuses on acquisitions like Roboteam and Rotron Aero.

Trends show confidence via $1 billion equity raise, boosting cash to $1.5 billion. ONDS insider activity implies long-term bets over short-term trades.

This suggests caution on optics but faith in strategy, watch for Form 4 updates.

Valuation Analysis

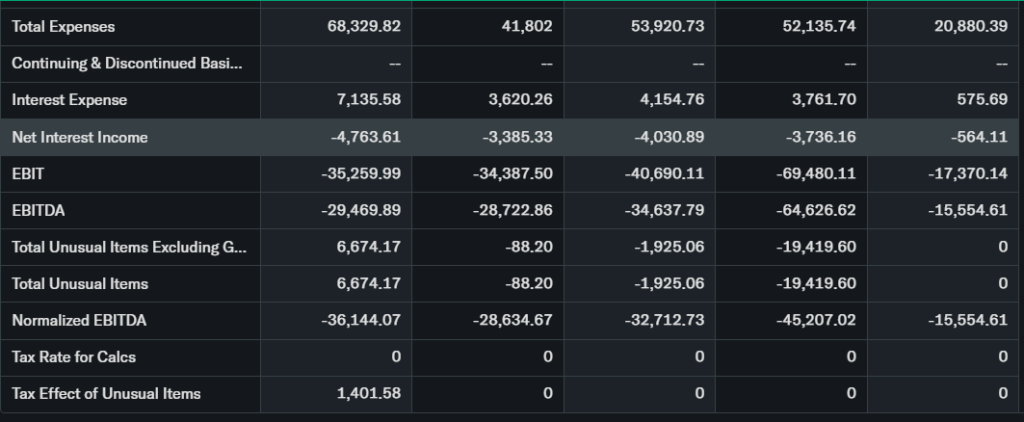

Trailing P/E stays negative on losses, forward P/E improves with guidance. Price-to-sales looks stretched versus peers like smaller drone firms. Revenue growth hit 51% in Q4 prelims over targets.

EPS growth accelerates on backlog up 180% to $65.3 million. Free cash flow pressures from expansion, but $1.5 billion cash offsets debt. ONDS valuation appears fairly valued against autonomy peers.

Compared to Zoom or larger tech, ONDS trades at growth premiums—neither cheap nor overdone.

Recent Earnings & Catalysts

Q4 2025 revenue hit $27-29 million, beating prior targets by 51%. Backlog soared to $65.3 million. Full results due March 25 with expected EPS loss of 4 cents on $27.86 million sales.

2026 guidance raised to $170-180 million, up 25%. Catalysts include World View $10 million investment for ISR tech and acquisitions. ONDS quarterly results drove initial pops, now digested in price.

Earnings beat yet stock dipped on spend visibility.

Bullish Case

Strong backlog and M&A pipeline with 20 targets fuel revenue growth. ONDS revenue growth catalysts shine in C-UAS and robotics demand. NDAA-compliant U.S. production aids defense wins.

Partnerships like Rift Dynamics expand platforms. Cash pile enables buys without dilution risks. Tech edges in multi-domain autonomy attract contracts.

Bearish Case

Heavy infrastructure and team costs pressure margins short-term. Competition from larger drone makers like bigger autonomy players looms. ONDS stock faces slowing growth if M&A integration lags.

Economic slowdowns hit capex budgets. Regulatory hurdles in defense add caution.

Market Sentiment & Investor Psychology

Short interest data limited, but options show put activity like Mar 2026 11-put up 34%. Calls lag, hinting bearish bets. Institutional ownership rises post-raise.

Retail chases momentum dips. Sentiment skews neutral—fear from monthly drop, optimism on guidance. ONDS forecast leans value over hype.

Short-Term Outlook

Technical signals mix with 1 buy, 3 sells—downtrend but volume drop signals rebound. Earnings on March 25 key. ONDS stock price may consolidate near $2.02 support next weeks.

Watch momentum for bounce without overcommitting.

Medium to Long-Term Outlook

Robust cash and pipeline strengthen business model in growing autonomy sector. Competitive edge in ground-air systems positions well. ONDS long term outlook favors accumulation for growth investors.

Financial health solid, risks in execution—hold or add on dips.

FAQ Section

Is ONDS stock a buy right now?

Neutral hold; wait for earnings clarity amid strong guidance.

What is the ONDS stock price target?

Average $2.13, up to $2.63 per analysts.

What are major risks for ONDS stock?

Margin squeezes, integration delays from M&A.

What drives ONDS earnings?

Backlog execution, defense contracts.

ONDS technical analysis summary?

Neutral, rebound potential near support.

Suggestion

Compare with Opendoor sector peers.

See our AI stock forecast analysis.

Read defense tech valuation trends.

Conclusion

Hold ONDS stock—backlog and cash support growth, but watch earnings and costs. Balanced view favors patience over chase.

Disclaimer: This article is for informational purposes only and not financial advice.