Explore NVO stock analysis with latest price, technicals, earnings, valuation, and forecast. Is NVO stock a buy? Get balanced insights for investors as of March 2026.

Introduction

Novo Nordisk develops diabetes, obesity, and rare disease treatments like Ozempic and Wegovy. NVO stock draws attention due to GLP-1 drug demand amid obesity trends. Broader market pressures from rate hikes and competition hit healthcare stocks.

Latest Stock Price & Trend

NVO stock closed at $37.45 on February 26, down 0.45% that day. It dropped 2.80% over one day and 37.76% in the past four weeks. The one-month trend shows sharp decline, with 3-month and 6-month falls near 58% yearly.

Year-to-date, NVO lost over 50% from peaks, hitting a 52-week low of $37.31 versus high of $91.90. This bearish trend signals caution for investors, as selling pressure dominates amid valuation resets.

Technical Analysis

Support levels sit at $37.31, the recent low, while resistance is near $49.68 pivot. RSI at 19.58 indicates oversold conditions, suggesting potential rebound. MACD at -2.61 points to buy signals despite downtrend.

The 50-day moving average is $48.73, above price, and 200-day at $61.13 shows no golden cross—death cross occurred earlier. Trading volume hit 22 million shares, above average 19-30 million, showing high interest. These metrics warn of volatility but hint at bounce for beginners.

Analyst Ratings & Price Targets

Of 20 analysts, 1 sell, 10 hold, 7 buy, 2 strong buy yield moderate buy consensus. Average target $76.00 implies 43% upside from $53 recent levels, high $160, low $47. Recent downgrades from UBS, HSBC, Barclays shifted to hold.

Wall Street sees value post-drop but cites competition risks. This mixed sentiment urges investors to weigh growth versus hurdles.

Insider Activity

Recent insider trades show limited large buys or sells per SEC filings. Management activity trends neutral, with no major confidence signals. Routine transactions imply steady but cautious outlook from executives.

Valuation Analysis

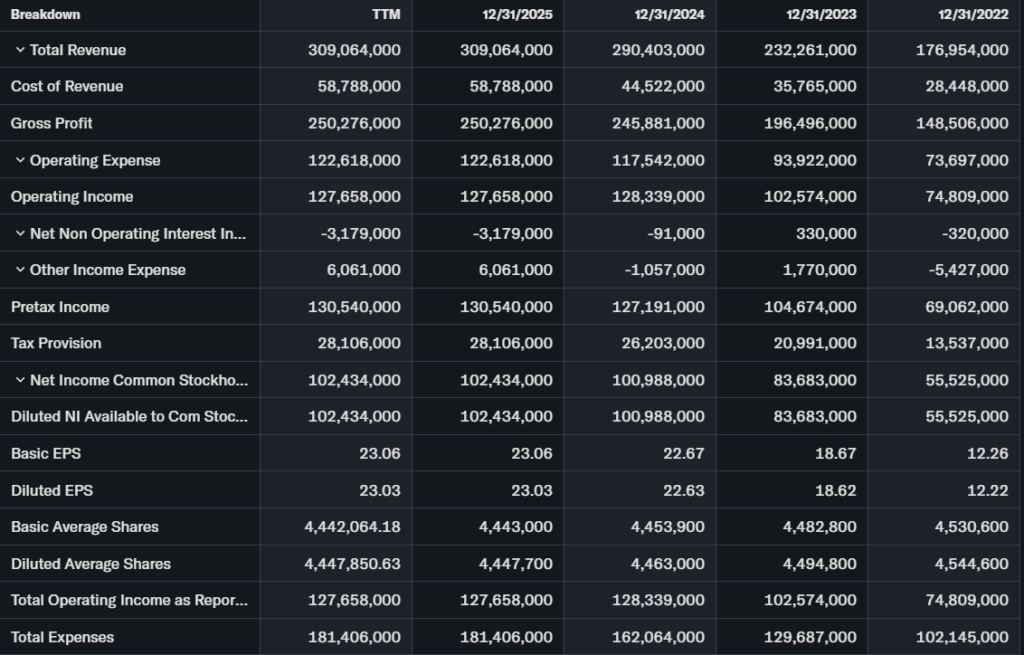

Trailing P/E is 10.74-10.83, forward lower at normalized 9.29. Price-to-sales at 3.57, with YoY revenue growth strong at 37% in obesity. EPS grew to $1 in Q4 2025, beat estimates by 12%.

Free cash flow supports dividends at 4.61% yield; debt manageable with solid cash. Versus peers like Eli Lilly, NVO appears undervalued post-correction.

Recent Earnings & Catalysts

Q4 2025 revenue beat via Wegovy sales up 41% CER to DKK 59.9B. EPS $1 topped $0.89 forecast; net profit DKK 75.5B up 4%. Guidance cuts 9,000 jobs for efficiency amid growth.

Catalysts include GLP-1 expansions, but stock fell on competition fears. Earnings drove initial pops then pullback.

Bullish Case

Wegovy demand fuels 37% obesity revenue growth. GLP-1 leadership and rare disease 13% rise aid expansion. Cost cuts boost margins long-term.

Bearish Case

Competition from Eli Lilly erodes share; 56% yearly drop reflects this. Pricing pressures, regulatory scrutiny on GLP-1s loom. Job cuts signal margin strains.

Market Sentiment

Short interest data limited, but high volume shows activity. Institutional ownership strong at 343M shares by Loomis, Citadel. Retail chased highs, now fearful post-drop.

Sentiment neutral to optimistic on value, momentum bearish.

Short-Term Outlook

Oversold RSI and volume spikes suggest rebound potential next weeks. Momentum may stabilize if support holds $37. Watch resistance at $50.

Medium to Long-Term Outlook

Strong business in growing obesity market, competitive moat via brands. Financial health solid with cash flow. Long-term investors should hold or accumulate on dips despite risks.

FAQ

Is NVO stock a buy right now? Moderate buy per analysts, undervalued at P/E 10 but volatile.

What is the price target for NVO stock? Average $76, up to $160.

What are major risks for NVO stock? Competition, regulation, slowing GLP-1 growth.

What is NVO earnings outlook? Next EPS $0.88 expected.

Suggestions

Compare with Opendoor stock analysis.

See our healthcare sector valuation breakdown.

Read Lilly obesity drug forecast.

Final Balanced Conclusion

Hold NVO stock. Valuation attractive post-drop, growth intact, but competition warrants caution.

Disclaimer: This article is for informational purposes only and not financial advice.