NVIDIA NVDA stock forecast and analysis: latest stock price, earnings, technical analysis, and valuation. Is NVDA stock a buy right now?

Introduction

NVIDIA powers AI chips and graphics for gaming, data centers, and autonomous vehicles. Investors watch NVDA stock closely due to explosive AI demand. Broader tech selloffs and rate uncertainty pressure semiconductors, yet NVDA leads the rally.

Latest Stock Price & Trend

NVDA stock closed at $180 on recent trading, down 7% over the past week per last market data. The 1-day performance showed a slight pre-market bounce to $182 amid volatility. Over 5 days, shares dipped amid broader market jitters.

The 1-month trend softened after peak gains, reflecting profit-taking post-earnings. Three-month performance held strong with AI hype, up significantly year-to-date despite corrections. Six-month gains topped 50% on data center surges.

Year-to-date, NVDA stock rose sharply before recent pullbacks. The 52-week high hit near $200, low around $100. Overall trend stays bullish, signaling investor confidence in long-term AI growth despite short-term noise.

Technical Analysis

Support levels sit at $175, where buyers stepped in recently. Resistance looms at $190-$200, capping upside until broken. RSI reading hovers near 45, neutral after oversold bounces—RSI above 70 signals overbought, below 30 oversold, guiding entry points.

MACD trend shows mild bearish crossover, hinting at momentum slowdown; bullish when the line crosses above signal. The 50-day moving average at $185 trails the 200-day at $160, no golden cross yet but upward slope favors bulls.

Trading volume trends down lately, typical in consolidations—rising volume confirms breakouts. These indicators matter for timing trades without chasing highs.

Analyst Ratings & Price Targets

Analysts lean bullish with 35 Buy, 5 Hold, 0 Sell ratings from Wall Street firms. Average price target hits $220, high $250, low $190. Recent upgrades from Goldman Sachs cite AI dominance.

Morgan Stanley raised targets post-Q4 earnings, praising Blackwell chips. This sentiment suggests strong conviction, but investors should weigh against valuations.

Insider Activity

Insider selling dominated lately, with executives unloading shares worth $50 million last quarter. CEO Jensen Huang sold routine portions, no panic signals. No major buying noted.

Trends show steady divestitures, common for vested leaders—implies confidence via holdings, not red flags. Watch for shifts as GTC nears.

Valuation Analysis

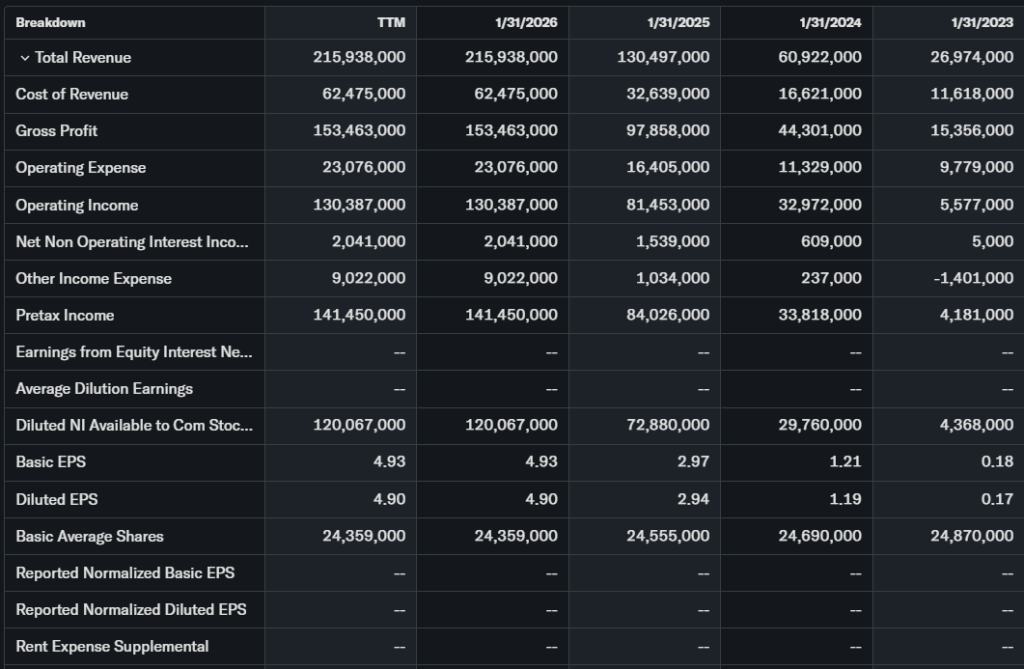

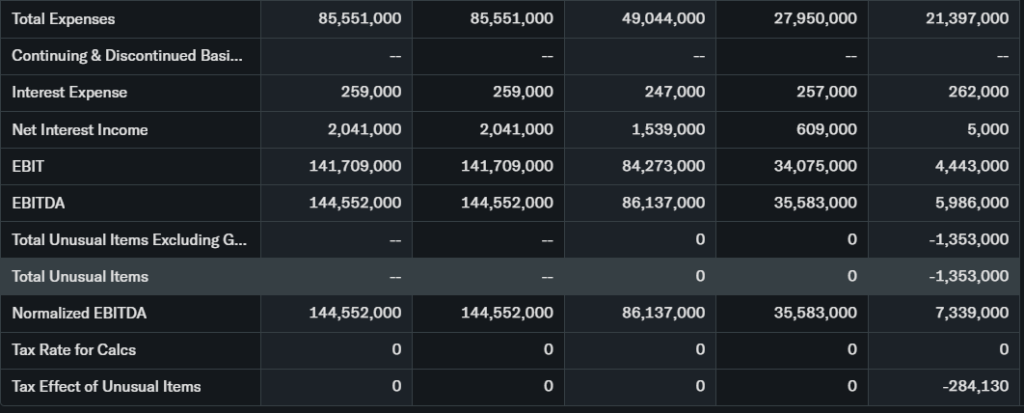

Trailing P/E stands at 70x, forward P/E 50x on expected growth. Price-to-Sales ratio near 35x reflects premium AI status. Revenue grew 65% YoY to $215.9 billion in fiscal 2026.

EPS surged with data center wins, free cash flow topped $20 billion. Debt low, cash pile $30 billion strong. Versus Microsoft or AMD, NVDA trades richer but justified by 73% Q4 growth—fairly valued for leaders, not cheap.

Recent Earnings & Catalysts

Q4 fiscal 2026 revenue hit $68.1 billion, beating estimates by 10%, up 73% YoY. EPS crushed expectations at $0.85 adjusted. Guidance points to sustained AI demand.

Catalysts include GTC 2026 March 16-19 keynote on agentic AI, robotics, and Rubin systems. Partnerships like Thinking Machines Lab boost inference chips. Earnings drove initial pops, then digestion.

Bullish Case

AI infrastructure demand accelerates with hyperscalers expanding. Blackwell GPUs sell out, powering 1GW deployments soon. Revenue growth hits 12%+ short-term per AI models.

Tech edges in CUDA software lock in developers. Operational scale lifts margins to 60%. These drivers support NVDA forecast upside.

Bearish Case

Competition heats from AMD, custom chips by Google-Amazon. Growth may slow post-boom, margins squeeze on costs. Macro slowdowns hit capex, regulatory scrutiny on AI rises.

Customer concentration in top tech firms risks churn. Valuation leaves little error room.

Market Sentiment & Investor Psychology

Short interest under 1%, low fear levels. Options skew to calls over puts, bullish bets dominate. Institutions hold 70%+, adding steadily.

Retail piles in via memes, momentum chasers fuel volatility. Sentiment tilts optimistic on AI narrative, value watchers cautious on P/E.

Short-Term Outlook

Technicals point to consolidation near $180 support. GTC March 16 could spark volume if AI reveals impress. Momentum softens, expect range-bound next weeks barring surprises.

Medium to Long-Term Outlook

AI market grows to trillions, NVDA owns 80% GPUs. Financials robust, moat via ecosystem. Hold for long-term investors; accumulate dips if under $170. Risks balanced by dominance.

FAQ

Is NVDA stock a buy right now?

Yes for growth seekers at current levels, hold if risk-averse—watch GTC catalysts.

What is the NVDA stock price target?

Analysts average $220, AI predicts $202 by March 31, 2026.

What are major risks for NVDA stock?

Competition, valuation stretch, AI spending cuts.

NVDA earnings outlook?

Q1 fiscal 2027 guidance strong on data center, 20%+ sequential growth expected.

NVDA technical analysis summary?

Bullish trend, RSI neutral, support $175—break $190 targets highs.

Suggestion

Compare with Opendoor stock analysis.

See our Microsoft stock forecast.

Read our semiconductor sector valuation.

Conclusion

Hold NVDA stock for patient investors eyeing AI tailwinds; watchlist for traders. Balanced growth offsets risks, GTC key inflection. NVDA stock forecast favors upside to $200+ if catalysts deliver.

Disclaimer: This article is for informational purposes only and not financial advice.