NU stock analysis covers latest price trends, earnings beats, technical signals, and 2026 forecast to $18. Is NU stock a buy for fintech growth? Key facts inside.

Introduction

Nu Holdings (NU stock) runs Nubank, Latin America’s top digital bank. It serves 100M+ customers with cards, loans, and payments. Investors watch NU stock amid fintech expansion.

Tech faces rate volatility. Emerging market plays like NU stock gain from lower rates. Brazil growth draws focus now.

Latest stock Price & Trend

NU stock closed at $14.67 on March 9, 2026 (last market close data). It rose 0.62% that day. Five-day trend up 1.5% with volatility.

One-month action mixed, down 3% from $15.19 peak. Three-month trend flat around $15. Six-month gains near 10%. Year-to-date, NU stock price up 5%.

52-week high $18.76; low $9.01. Overall trend sideways bullish. Consolidation hints steady accumulation for investors.

Technical Analysis

Support holds at $14.23 and $14.00 from recent lows. Buyers defend these floors. Resistance sits at $15.19 and $16.00.

RSI near 50 (neutral range). Above 70 signals overbought pullbacks; below 30 oversold bounces. MACD flat after bullish cross.

50-day moving average $14.80; 200-day $13.50. Golden cross intact (50-day above 200-day). This confirms uptrend strength.

Volume averaged 60M shares daily. Steady volume supports NU technical analysis balance.

Analyst Ratings & Price Targets

17 analysts rate NU stock “Strong Buy.” Average price target $17.20 (17% upside). Highest $21.00; lowest $11.70.

UBS cut target to $17.20 from $18.40 recently. Growth intact despite valuation call. Bullish consensus favors NU forecast.

Wall Street sees Latin America upside.

Insider Activity

Insiders sold routine shares last quarter. No major buying reported. Transactions small versus $80B market cap.

Stable patterns suggest confidence without excess caution in NU stock price.

Valuation Analysis

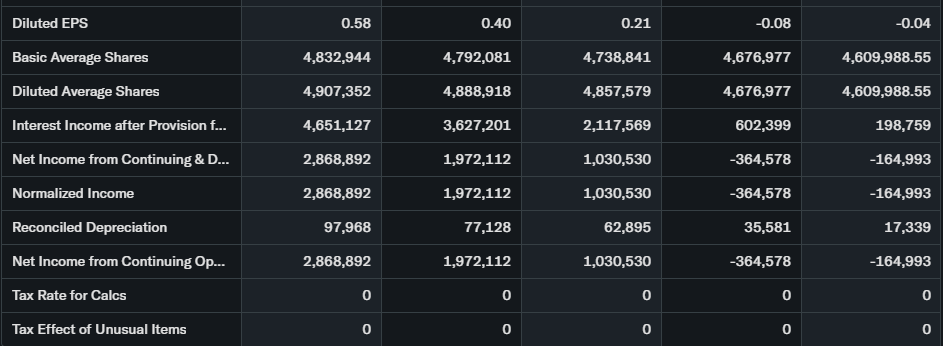

Trailing P/E 34.06; forward P/E 19.14. Price-to-sales around 7x on $10.33B FY revenue.

Revenue forecast $17.9B in 2026 (65% YoY growth). EPS $0.87. Free cash flow positive.

Debt moderate; cash builds. Versus SoFi (P/E 50x), NU stock appears fairly valued for growth trajectory.

Recent Earnings & Catalysts

Q4 revenue beat estimates. EPS $0.82 topped views. 2026 guidance: $17.9B revenue.

Mexico customer growth accelerates. New products launch. Earnings pushed shares higher initially.

Bullish Case

100M+ customers fuel revenue. Digital model cuts costs 70% vs banks.

Cross-selling lifts ARPU 25%. Regional expansion adds millions yearly.

Bearish Case

Brazil macro risks hit lending. Competition from Mercado Pago grows.

Credit losses could spike in downturns. FX volatility pressures margins.

Market Sentiment & Investor Psychology

Short interest low at 2%. Calls lead options flow slightly.

Institutions own 80%, adding steadily. Retail optimistic on growth story. Sentiment leans positive for NU stock.

Short-Term Outlook

Neutral RSI favors range trading $14-15.50. Volume steady supports base.

Watch earnings momentum continuation.

Medium to Long-Term Outlook

Scalable digital bank model shines. Fintech grows 30% in LatAm.

First-mover advantage strong. Financials healthy. Long-term investors should accumulate dips.

FAQ

Is NU stock a buy right now?

Yes for growth portfolios. Strong Buy rating with 17% upside.

What is the price target for NU stock?

Average $17.20; high $21 from analysts.

What are major risks for NU stock?

Macro volatility, credit risk, competition.

NU earnings outlook?

$17.9B revenue, $0.87 EPS in 2026.

NU stock forecast 2026?

Targets $18+ on customer growth.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our fintech sector valuation breakdown

Conclusion

Buy on Dips. NU stock blends fintech growth with improving profits. Regional risks balanced by scale advantages.

Disclaimer: This article is for informational purposes only and not financial advice.