Explore NTNX stock price, latest trends, earnings, technical analysis, and forecast. Is NTNX stock a buy? Get balanced insights for investors as of February 27, 2026.

Introduction

Nutanix builds hybrid cloud software for data centers. It helps companies run apps on their own servers or in the cloud. Investors watch NTNX stock now due to strong earnings growth in AI and cloud demand. Tech stocks face pressure from high interest rates and supply chain issues.

Broader market volatility hits tech amid economic slowdown fears. NTNX stock stands out with recurring revenue from subscriptions. This NTNX stock analysis covers key metrics for everyday investors.

Latest Stock Price & Trend

NTNX stock closed at $38.45 on February 26, 2026. It rose 2.53% that day on high volume of 3.3 million shares. The stock shows a short-term downtrend, down 6.11% over five days from $40.95.

One-month performance dipped amid market selloffs. Year-to-date in 2026, NTNX stock fell 25.76% from $51.79. The 52-week range spans $35.39 low to $83.35 high. Overall, the trend looks bearish with recent lows near support.

This signals caution for short-term traders. Long-term holders see value if cloud demand rebounds. Investors should watch volume for reversal signs.

Technical Analysis

Support levels sit at $36.62, a recent low where buyers stepped in. Resistance looms at $39.10 to $42.61, capping upside. These levels matter as they show where price stalls or bounces.

RSI reads 38.3, neutral but nearing oversold below 30. This momentum oscillator flags if NTNX stock overheats. MACD stays bearish with the line below signal, hinting at more downside.

The 50-day moving average tops the 200-day, a bullish sign despite price weakness. No golden or death cross recently. Volume spiked on down days, showing selling pressure.

Analyst Ratings & Price Targets

Fifteen analysts rate NTNX stock as Buy overall. Average price target hits $90.14, with highs at $95 and lows unspecified. Upside potential reaches 29-36% from current levels.

Goldman Sachs initiated Strong Buy at $95. KeyBanc and Piper Sandler raised targets post-earnings. One downgrade from Raymond James to Hold. Positive sentiment reflects growth bets.

This means Wall Street sees upside, but investors must weigh risks. Ratings guide but don’t predict perfectly.

Insider Activity

Insiders sold net $892,414 in 11,391 shares over last 30 days. No buys reported recently. CFO Rukmini Sivaraman sold most at $78.34.

CEO Rajiv Ramaswami and directors like de Groen made large sales earlier. Trend shows ongoing selling, implying profit-taking over deep concern. Executives hold significant shares still.

This suggests caution, as buying signals stronger confidence. Watch for shifts in activity.

Valuation Analysis

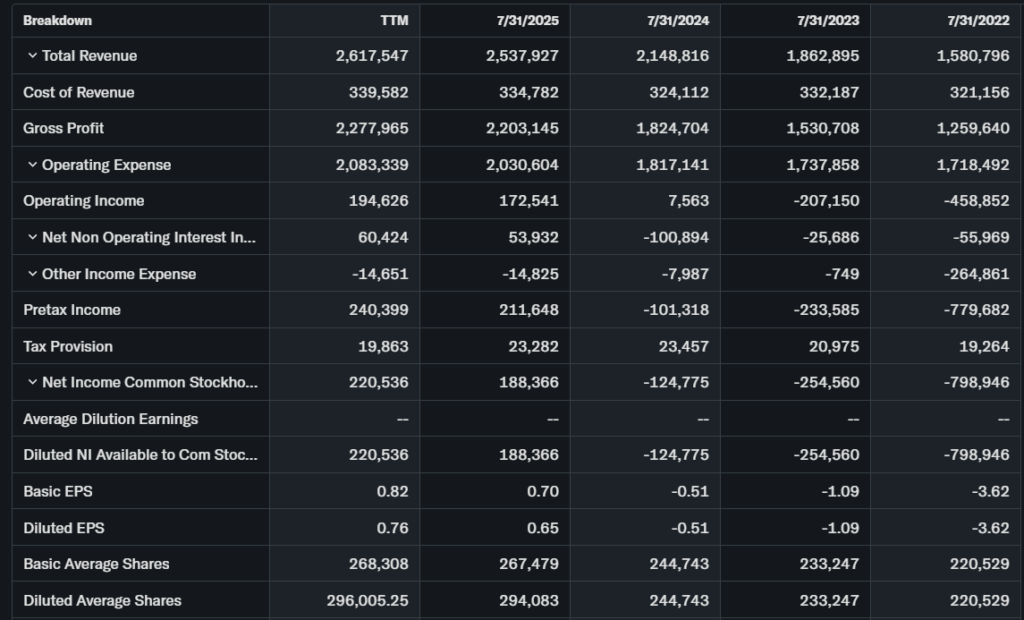

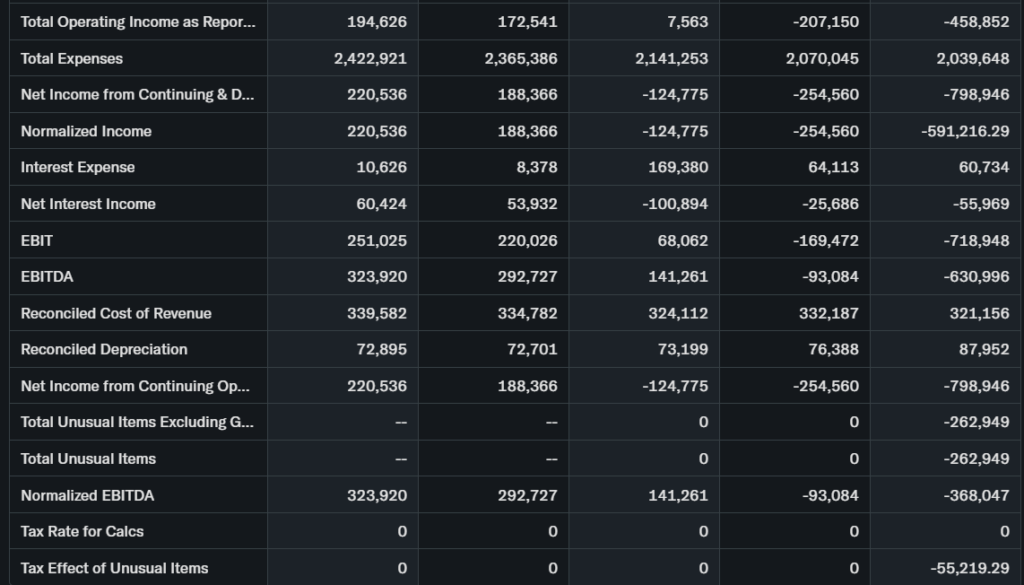

Trailing P/E unavailable due to past losses; forward metrics improve with EPS growth. Price-to-sales around 3-4x based on $2.8B revenue guidance. YoY revenue grew 10-16% in Q2.

EPS growth hit 107% quarterly YoY. Free cash flow strong at $191M in Q2, $745-775M yearly guide. Cash at $2.06B tops $1.49B debt, net cash $577M.

Versus peers like VMware remnants or cloud firms, NTNX looks fairly valued. Not cheap, but growth justifies premium. Stock appears fairly valued for quality.

Recent Earnings & Catalysts

Q2 FY2026 revenue hit $722.8M, up 10% YoY, beating estimates. ARR rose 16% to $2.36B. Non-GAAP margin at 26.2%, operating income $84M.

EPS topped views; guidance lifted to $2.80-2.84B revenue FY2026. Supply delays noted for Q3. Stock dipped post-earnings on timing worries.

Catalysts include AI integrations and hybrid cloud wins. Partnerships boost pipeline. Earnings drove initial gains but faded.

Bullish Case

Subscription ARR grows steadily at 16% YoY. Cloud market demand surges with AI needs. Nutanix tech unifies on-prem and cloud better than rivals.

Margins expand via efficiency. Bookings strong despite supply hiccups. Operational fixes cut costs.

Bearish Case

Competition from VMware, AWS heats up. Growth may slow if economy weakens. Supply chain delays pressure near-term revenue.

Margin squeezes possible on R&D spend. Customer shifts to public cloud risk churn. Regulatory scrutiny on tech grows.

Market Sentiment

Short interest at 4.18% of float, low at 11.2M shares. Days to cover 4.88, not extreme. Institutional ownership high with 940 holders.

Options show balanced calls/puts; no heavy bets. Retail chases momentum down. Sentiment neutral to optimistic on growth.

Short-Term Outlook

Technicals point bearish with MACD and volume. Momentum fades near support. Expect sideways to lower in days ahead. Watch $36 for bounce.

Medium to Long-Term Outlook

Strong business model with recurring revenue. Cloud industry booms 20%+ yearly. Competitive edge in hybrid setups. Financials healthy with cash flow.

Hold for long-term investors; accumulate on dips. Risks from competition persist.

FAQ

Is NTNX stock a buy right now? Analysts say yes with Buy ratings, but wait for technical stabilization.

What is the NTNX stock price target? Average $90.14, up to $95 from firms like Goldman.

NTNX forecast for 2026? Revenue $2.8B+, ARR growth continues.

Major risks for NTNX stock? Supply delays, competition, economic slowdown.

NTNX earnings next quarter? EPS $0.44 expected on $699M revenue.

Suggestions

Compare with Opendoor stock analysis

See our cloud computing sector forecast

Read VMware alternatives breakdown

Final Balanced Conclusion

Hold NTNX stock. Growth shines, but short-term trends and sales warrant patience. Valuation fair for quality. Long-term potential strong.

Disclaimer: This article is for informational purposes only and not financial advice.