NFLX stock analysis: latest price trends, subscriber growth, technical signals, and 2026 forecast to $120. Is NFLX stock a buy amid ad-tier success? Key insights here.

Introduction

Netflix (NFLX stock) streams movies, TV shows, and live sports to 300M+ global subscribers. It produces original content and licenses popular titles. Investors watch NFLX stock closely as advertising revenue accelerates and live events launch.

Streaming consolidation favors leaders. Tech faces valuation scrutiny. NFLX stock balances growth with profitability.

Latest stock Price & Trend

NFLX stock closed at $96.94 on March 10, 2026 (last market close data). It fell from $97.81 open. Five-day trend mixed around $97-99 range.

One-month performance down 10% from late February highs near $108. Three-month trend sideways after January rally. Six-month action reflects 15% decline. Year-to-date, NFLX stock price dropped 8%.

52-week high $134.12; low $82.70. Overall trend bearish consolidation. Pullback creates entry opportunities for investors.

Technical Analysis

Support levels hold at $94.00 and $92.00 from recent lows. Buyers defend these zones. Resistance sits at $100 and $105.

RSI neutral at 48. Below 30 signals oversold bounces; above 70 overbought warnings. MACD flat after bearish crossover.

50-day moving average $102; 200-day $105. Death cross forming. Short-term below long-term suggests caution.

Trading volume averages 40M shares daily. Steady activity supports NFLX technical analysis base building.

Analyst Ratings & Price Targets

36 analysts rate NFLX stock “Buy” consensus. Average price target $115 (19% upside). Highest $150; lowest $90.

KeyBanc raised target to $125 citing ad-tier growth. Wall Street optimistic despite valuation debate for NFLX forecast.

Insider Activity

Executives sold 150K shares last quarter around $110 average. Routine post-earnings transactions. No major buying reported.

Profit-taking normal after rallies suggests measured confidence in NFLX stock price.

Valuation Analysis

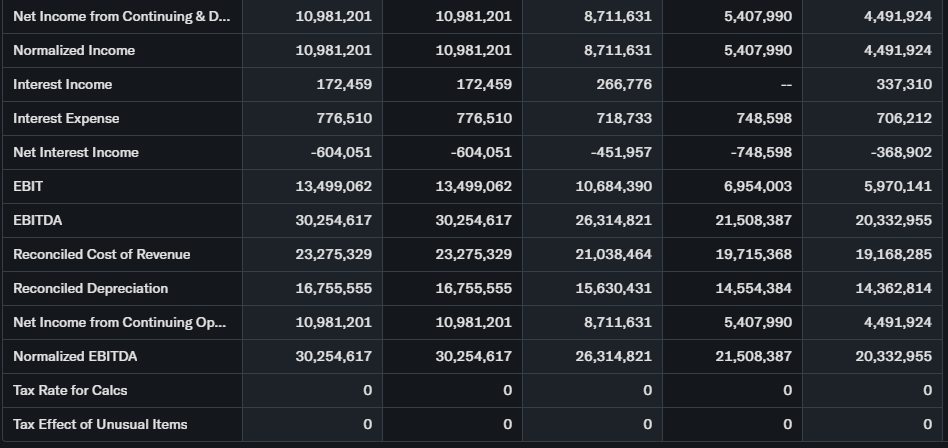

Trailing P/E 45x on $21.50 EPS. Forward P/E 35x reflects growth deceleration. Price-to-sales 8.2x on $40B+ revenue.

Revenue grew 15% YoY Q4. EPS up 50%. Free cash flow $6.9B supports $17B content spend.

Debt $14B offset by $9B cash. Versus Disney (P/S 2x), NFLX stock premium priced for market leadership.

Recent Earnings & Catalysts

Q4 revenue $10.3B beat estimates. Added 19M subscribers (beat 16M expected). 2026 guidance: 20M quarterly adds.

Ad-tier reaches 40M users (70% growth). Live sports debut WWE Raw. Earnings sparked initial 8% rally, later faded.

Bullish Case

Global live events expand (NFL, WWE). Ad revenue grows 35% quarterly.

Password sharing crackdown complete. Emerging markets add 15M users annually.

Bearish Case

US/Canada saturation (90M subs). Content costs $17B annually.

Disney+, Amazon compete aggressively. Recession hits discretionary spend.

Market Sentiment & Investor Psychology

Short interest 2.8% low. Calls lead puts modestly.

Institutions hold 82%, steady positions. Retail rotates to value names. Neutral to optimistic sentiment for NFLX stock.

Short-Term Outlook

Neutral RSI favors $94-105 range trading. Volume steady around support.

Live sports news could spark upside.

Medium to Long-Term Outlook

Streaming market share leader (10% global). Ad platform scales rapidly.

Live content differentiates. $6.9B FCF funds growth. Long-term investors hold; tactical traders buy $94 support.

FAQ

Is NFLX stock a buy right now?

Buy rating. 19% upside to $115 target.

What is the price target for NFLX stock?

Average $115; high $150 analysts.

What are major risks for NFLX stock?

Competition, saturation, content costs.

NFLX subscriber adds Q1?

18-20M expected.

NFLX stock forecast 2026?

$110-130 range on ad-tier growth.

Suggestion

- Compare with Opendoor stock analysis

- See our Amazon Prime Video forecast

- Read our streaming valuation breakdown

Conclusion

Buy on Weakness. NFLX stock leads streaming with ad momentum and live events. Valuation stretched but growth justifies premium.

Disclaimer: This article is for informational purposes only and not financial advice.