Explore NBIS stock forecast with $150 analyst targets, latest price trends, technical analysis, earnings, and buy/hold advice for Nebius Group AI cloud play. Balanced insights for investors.

Introduction

Nebius Group (NASDAQ: NBIS) builds AI-focused cloud infrastructure and data centers worldwide. The company spun off from Yandex and now powers AI workloads with GPU clusters. Investors watch NBIS stock closely after Missouri approved a $650M, 1.2 GW AI data center project, sparking a 10% surge.

Broader market conditions favor AI stocks amid tech rallies, but volatility hits high-valuation plays like NBIS. President Trump’s pro-business policies boost infrastructure bets.

Latest Stock Price & Trend

NBIS stock closed at $97.79 on March 4, 2026, last market data shows, up 9.8% in the session on data center news. It gained 12% over five days, reflecting momentum from the approval.

One-month trend shows 25% rise earlier, but recent pullback from $98.48 high. Year-to-date, shares soared over 193% trailing twelve months, crushing benchmarks.

52-week low sits at $84.96, high near $98.48 recently; 6-month up strongly on AI demand. Overall bullish trend signals investor confidence in growth, but watch for pullbacks in volatile tech sector.

Technical Analysis

Support levels hover at $95.72 short-term, $50.40 mid-term—key floors where buyers step in. RSI at 40 means neutral, not overbought (above 70) or oversold (below 30), showing balanced momentum.

MACD line below signal indicates mild bearish short-term, but overall bullish trend persists. 50-day moving average tops 200-day, no death cross; this “golden cross” hints at uptrend continuation.

Volume spiked to 21M vs 15M average, confirming buying interest on news. These point to strength for NBIS technical analysis, but resistance at $135 caps near-term gains.

Analyst Ratings & Price Targets

Six Buy, one Hold ratings give Strong Buy consensus. Average target $150.86, high near that, low unspecified—implies 54% upside from $97.79.

DA Davidson held steady; TipRanks backs optimism. Positive sentiment from Wall Street means pros see AI growth outweighing risks for NBIS stock.

Insider Activity

Limited recent SEC Form 4 data shows no major buys or sells highlighted. Charts track ongoing activity, but no large transactions noted lately.

Neutral trends imply steady confidence without red flags; watch for future filings signaling caution or buys.

Valuation Analysis

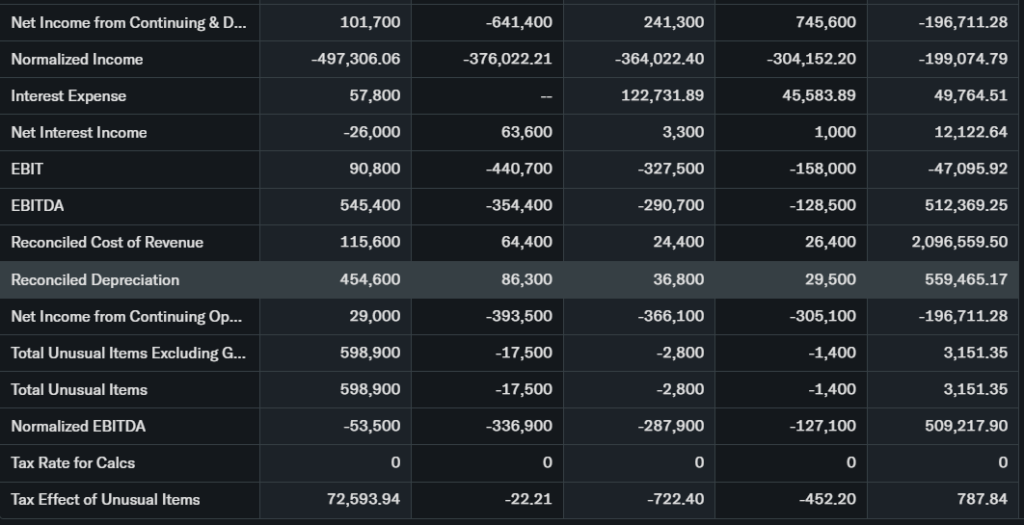

Trailing P/E at 243x or higher reflects growth premium; forward likely lower on EPS improvement. Price/Sales 46.81, high vs peers like Oracle (lower) or Microsoft.

Revenue grew 351% YoY to $530M TTM, EPS $0.40; free cash flow positive but capex heavy. Debt/equity promising, cash strong with 6.57 current ratio.

Compared to Zoom or Microsoft, NBIS looks overvalued on P/E but justified by AI hype; appears fairly valued for growth.

Recent Earnings & Catalysts

Q3 revenue hit $105M, near $105M estimates; EPS -0.38 beat -0.50 forecast. Guidance eyes $155M next quarter.

Missouri 1.2GW campus ($650M investment, 1200 jobs) drove 10% jump; Microsoft deal prior boosted 42%. Earnings beat lifted shares, catalysts fuel AI demand.

Bullish Case

AI cloud demand surges; 16 global data centers by year-end position NBIS well. Revenue catalysts from partnerships like Microsoft, operational scale via GPU clusters.

Tech edges in neocloud compete with CoreWeave; 193% TTM gain shows market buy-in.

Bearish Case

High capex, 5.3% pretax margins pressure profits amid $20B+ valuation. Competition from hyperscalers, slowing AI hype risk churn.

Economic slowdowns or regulatory hurdles could hit infrastructure builds.

Market Sentiment & Investor Psychology

Short interest data sparse; mixed options with calls on up days. Institutional ownership rising, retail piles in on news.

Optimistic sentiment from 193% gains, momentum bias strong.

Short-Term Outlook

Technicals show bullish trend with volume support, but MACD bearish hints pullback to support. Momentum from catalyst may hold gains next week.

Medium to Long-Term Outlook

Strong AI model, industry boom (1.2GW projects), solid finances favor growth. Competitive moat via scale; hold for long-term investors eyeing 74% upside.

FAQ Section

Is NBIS stock a buy right now?

Strong Buy ratings and $150 target suggest yes for growth seekers, but high valuation adds risk.

What is the price target for NBIS stock?

Analyst average $150.86, up 54% from current.

What are major risks for NBIS stock?

Capex burdens, competition, margin squeezes in AI cloud.

NBIS earnings outlook?

Next EPS -0.56, revenue $155M; improving trajectory.

NBIS long term outlook?

Bullish on AI infrastructure expansion.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our AI sector valuation breakdown

Final Balanced Conclusion

Hold NBIS stock for AI exposure; growth drivers outweigh risks, but monitor valuations. Watchlist if risk-averse.

Disclaimer: This article is for informational purposes only and not financial advice.