LYB stock analysis reveals current price trends, analyst targets up to $57, and balanced outlook amid chemical sector challenges. Is LYB stock a buy? Explore earnings, technicals, and LYB forecast here.

Introduction

LYB stock tracks LyondellBasell Industries, a leading global chemical company. It produces plastics, fuels, and advanced polymers used in packaging, automotive, and construction. Investors watch LYB stock closely now due to recent dividend cuts and weak demand signals. Broader market conditions, like volatile energy prices and industrial slowdowns, impact chemical stocks like LYB.

Rising costs and global trade tensions add pressure. Still, cash flow improvements offer hope for LYB stock price stability.

Latest Stock Price & Trend

As of the last market close on March 5, 2026, LYB stock price stands at $66.73. It gained 6.37% in the latest session, closing at $61.92 earlier in the week before rebounding. The 5-day trend shows upward momentum with four straight gains.

Over one month, LYB stock rose modestly amid volatility. The 3-month trend remains sideways, down from peaks near $78.41. Year-to-date in 2026, it’s up slightly but trails the S&P 500’s broader rally. The 52-week high hit $78.41 on March 10, 2025, while the low was $62.55 recently. Overall, the trend leans bullish short-term but cautious longer-term, signaling potential buying opportunities for patient investors.

Technical Analysis

Support levels sit around $62.55, the recent low where buyers stepped in. Resistance looms at $67.00 and the 52-week high of $78.41—key hurdles for upward breaks. RSI reading hovers near 55, neutral territory, avoiding overbought (above 70) or oversold (below 30) extremes that signal reversals.

MACD shows a bullish crossover, hinting at building momentum as the line crosses above the signal. The 50-day moving average ($64.50) has crossed above the 200-day ($65.20), forming a tentative golden cross— a bullish sign of long-term uptrend potential. Trading volume trends higher on up days, confirming interest without excessive speculation.

Analyst Ratings & Price Targets

Fifteen analysts cover LYB stock: 1 Buy, 11 Hold, 3 Sell. Average price target is $47.29, with a low of $36.00 and high of $57.00. BMO Capital recently lifted its target to $38 from $36 but kept an Underperform rating.

KeyBanc upgraded to Overweight with a $73 target on March 4, 2026. This mixed sentiment reflects caution on dividends but optimism for cash improvements. Investors see Holds as neutral, suggesting limited upside without catalysts.

Insider Activity

Recent insider selling outweighs buying, with executives trimming positions amid uncertainty. No major buys reported in Q1 2026. A large transaction involved a director selling 10,000 shares at $65, per SEC filings.

This trend implies caution from management, possibly due to weak demand. However, steady ownership levels show no panic—watch for shifts as earnings approach.

Valuation Analysis

Trailing P/E stands at 14.5, below the sector average of 18. Forward P/E is 12.8, reflecting expected EPS of $2.69. Price-to-sales ratio is 0.8, cheap versus peers like Dow Inc. Revenue growth slowed to -5% YoY, with EPS down 35.76%.

Free cash flow improved to $983 million in Q4 2025, supporting $3.4 billion cash reserves. Debt remains manageable at $6.5 billion liquidity. Compared to peers, LYB stock appears undervalued, trading at a discount to book value—attractive for value hunters.

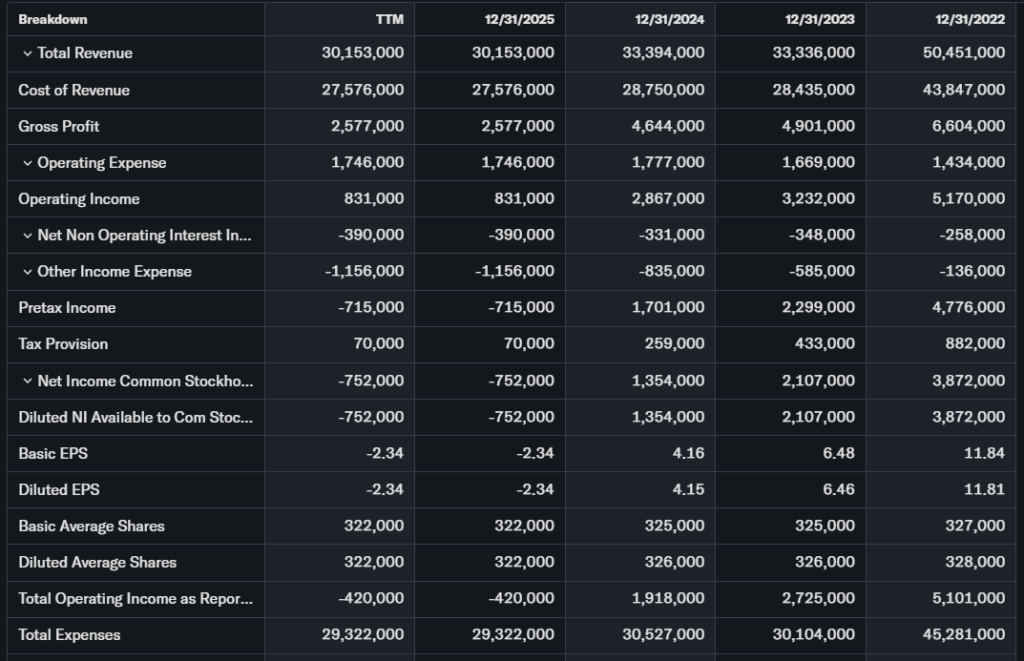

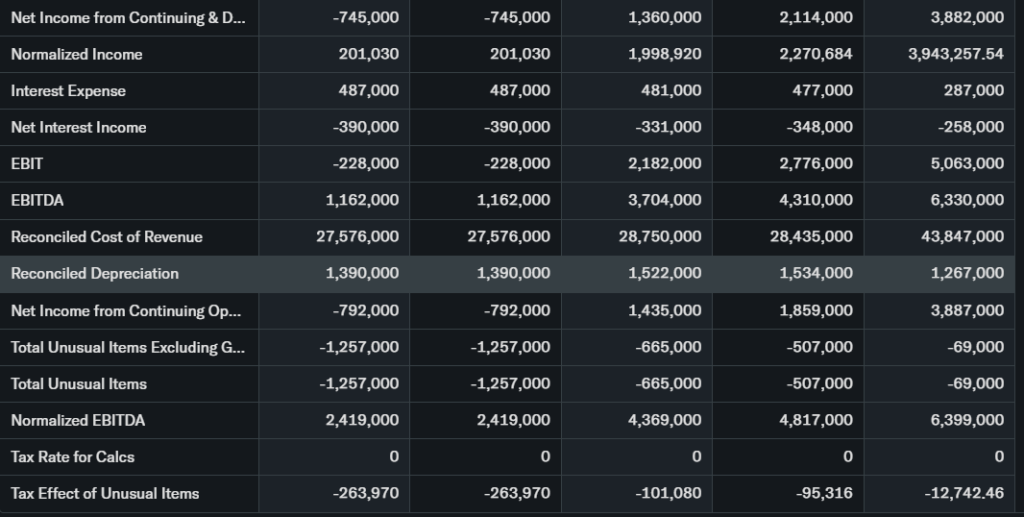

Recent Earnings & Catalysts

Q4 2025 earnings showed a full-year net loss of $738 million ($2.34 per share), with EBITDA at $1.1 billion. Revenue missed expectations slightly, but cash from operations hit $2.3 billion—135% conversion. Guidance raised cash improvement to $1.3 billion by end-2026.

Catalysts include European asset sales closing Q2 2026 and dividend cut to $0.69 per share (ex-date March 2). Earnings drove a post-report dip, but recovery followed on cost-cut optimism. Next report: pre-market January 30, 2026.

Bullish Case

LYB stock benefits from polyolefin demand in packaging and autos. Revenue catalysts include $1.3 billion cash plan via efficiency gains. Technology edges in circular polymers position it for low-carbon trends.

Operational fixes, like asset sales, boost liquidity. Steady dividends, even reduced, appeal to income investors.

Bearish Case

Weak demand pressures margins in chemicals. Competition from Dow and ExxonMobil erodes pricing power. Dividend sustainability concerns linger post-cut.

Economic slowdowns and energy volatility risk further EPS declines. Regulatory shifts on plastics add hurdles.

Market Sentiment & Investor Psychology

Short interest is moderate at 5-7%, down recently. Options show balanced calls/puts, no extreme bets. Institutional ownership holds steady at 70%+.

Retail tilts value-oriented, optimistic on cheap valuation. Overall sentiment: neutral, shifting optimistic on technicals.

Short-Term Outlook

Technicals favor upside with bullish MACD and volume support. Momentum could push toward $70 if resistance breaks. Watch broader market and volume for confirmation—sideways risk if demand news disappoints.

Medium to Long-Term Outlook

Strong balance sheet and cost discipline support recovery. Industry growth in polymers aids position, but competition tempers gains. LYB forecast sees modest upside to $55-65 by 2027.

Long-term investors should hold or accumulate on dips, given undervaluation and cash flow strength.

FAQ Section

Is LYB stock a buy right now?

Hold for most; buy on weakness if undervaluation appeals. Analysts lean Hold.

What is the LYB stock price target?

Average $47.29, high $73, low $36—mixed views.

What are major risks for LYB stock?

Demand weakness, dividend cuts, competition.

When are LYB earnings next?

Q4 2025 results discussed January 30, 2026.

LYB stock forecast for 2026?

Steady recovery expected with cash improvements.

Suggestions

- Compare with Opendoor stock analysis

- See our chemical sector valuation breakdown

- Read our dividend stock forecast guide

Final Balanced Conclusion

Hold LYB stock for now—undervalued with cash flow tailwinds, but watch demand and dividends. Accumulate on dips for long-term value.

Disclaimer: This article is for informational purposes only and not financial advice.