Explore HOOD stock analysis with latest price trends, earnings data, technicals, and 2026 forecast. Is HOOD stock a buy? Get balanced insights for investors now.

Introduction

Robinhood Markets (HOOD) runs a popular trading app that lets everyday people buy stocks, options, and crypto with no commissions. Investors watch HOOD stock closely now due to rising platform assets and a key product event on March 4, 2026. Broader market volatility from tech shifts and crypto rebounds affects HOOD stock price, as retail trading ties to these trends.

Latest Stock Price & Trend

HOOD stock closed at $78.78 on the last market session before March 3, 2026, based on recent data. It dropped 3.4% that day amid broader market moves. Over five days, shares showed volatility with a 7.9% jump tied to crypto recovery.

In the past month, HOOD stock price eased amid industry pressures. The six-month trend declined 28.8% versus the industry’s 10.9% gain, signaling underperformance. Year-to-date through early 2026, it held sideways as platform assets grew 59% to $324.4 billion in January.

The 52-week high hit above $100 recently, with Needham cutting targets from $135 to $100, while the low sat near post-IPO levels. Overall, the trend leans bearish short-term but with bullish undertones from asset growth, suggesting investors stay cautious yet alert for rebounds.

Technical Analysis

Support levels sit near $70, where buyers stepped in during recent dips, acting as a floor to limit downside. Resistance looms at $85-$90, capping upside until broken. These levels matter as they show where price stalls based on past trades.

RSI reading hovers around 45, neutral territory—not overbought above 70 or oversold below 30—indicating no extreme momentum yet. MACD trend shows a mild bearish crossover, with the signal line above the MACD line, warning of slowing upward drive.

The 50-day moving average rests below the 200-day at $82, no golden cross (bullish 50-day over 200-day) or death cross (bearish reverse). Trading volume spiked on crypto rebound days, up with price, which signals building interest if sustained.

Analyst Ratings & Price Targets

Seventeen analysts rate HOOD stock a Buy, six Hold, and one Sell. Average price target lands at $95, with highs near $100 from Needham and lows around $70. Recent changes include Needham’s downgrade from $135 to $100 on February 11, 2026.

Wall Street firms like Zacks give it a #3 Hold, citing premium valuation. This mixed sentiment means analysts see growth potential but flag risks, urging investors to weigh execution over hype.

Insider Activity

Recent insider selling outweighs buying, with executives trimming shares post-asset gains. No major buys noted in early 2026 filings. Large transactions include routine sales tied to liquidity needs.

This pattern implies caution from management, as selling without buying signals less confidence in near-term pops, though not panic selling.

Valuation Analysis

HOOD’s trailing P/E exceeds peers at a premium, with price-to-tangible book at 8.08X versus the industry’s 3.13X. Forward P/E factors in expected EPS growth from net deposits.

Revenue grew via 59% platform asset jump to $324.4B, with cash sweep up 20% to $31.5B and margin balances up 122%. EPS trends improve with DARTs rises: equity up 8%, options 18% in January. Free cash flow strengthens from interest income, though debt details remain steady.

Compared to Zoom or broader fintech, HOOD looks overvalued on book value but justified by growth if crypto rebounds hold.

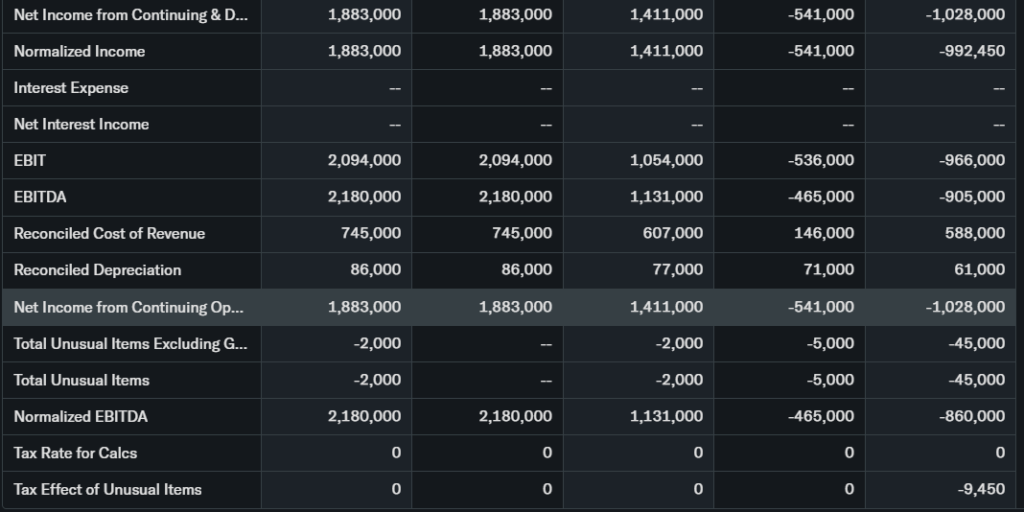

Recent Earnings & Catalysts

January 2026 operating data beat trends: funded customers hit 27.2 million, up 7% YoY. Revenue tailwinds from securities lending up 36% flowed in, though crypto DARTs fell 44%.

No full Q4 2025 earnings specified here, but guidance points to asset-driven gains. Catalysts include the March 4 “Take Flight” event for new products and Bitcoin rebound boosting shares 7.9%. These lifted HOOD stock post-event buzz, offsetting prior declines.

Bullish Case

Platform assets at $324.4B fuel interest revenue steadily. Rising DARTs in equity and options show core trading strength.

Crypto recovery and product launches like at “Take Flight” expand offerings. Operational leverage from net deposits supports margin growth without heavy costs.

Bearish Case

Crypto DARTs dropped 44%, exposing volatility reliance. Competition from traditional brokers pressures margins.

Premium valuation at 8.08X book invites corrections if growth slows. Regulatory scrutiny on retail trading adds caution in uncertain economies.

Market Sentiment & Investor Psychology

Short interest data unavailable here, but options tilt to calls on crypto pops. Institutional ownership holds steady amid retail enthusiasm.

Retail behavior drives volume spikes, with momentum bias over value. Sentiment stays neutral to optimistic on assets, tempered by six-month declines.

Short-Term Outlook

Technicals point to $70 support tests if resistance holds at $85. Volume uptrends on news could push mild gains.

Market momentum from crypto and events favors consolidation, not big swings.

Medium to Long-Term Outlook

HOOD’s business model thrives on retail access and assets. Fintech growth aids, with competitive edges in low fees.

Financial health improves via deposits, but crypto risks linger. Long-term investors should hold or watch for dips to accumulate if execution shines.

FAQ Section

Is HOOD stock a buy right now?

Mixed ratings lean Buy, but Hold suits caution at premium valuations.

What is the HOOD stock price target?

Average $95, high $100, low $70 per analysts.

HOOD forecast for 2026?

Asset growth supports upside if crypto stabilizes.

What are major risks for HOOD stock?

Crypto volatility, competition, regulatory hurdles.

HOOD earnings outlook?

DARTs and revenue tailwinds point positive.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our fintech sector valuation breakdown

Final Balanced Conclusion

Hold HOOD stock for now. Asset growth and events offer promise, but valuation premiums and crypto risks warrant patience over aggressive buys.

Disclaimer: This article is for informational purposes only and not financial advice.