Explore Hecla Mining (HL stock) latest price, technical analysis, earnings, and forecast. Is HL stock a buy? Get balanced insights on valuation, trends, and outlook for investors.

Introduction

Hecla Mining Company (NYSE: HL) produces silver, gold, lead, and zinc from mines in the U.S. and Canada. Investors watch HL stock closely now due to strong 2025 earnings and fresh 2026 production guidance from its key Greens Creek mine. Broader market conditions, like rising metal prices amid industrial demand and economic shifts under President Trump, boost silver miners like HL.

Latest Stock Price & Trend

As of the last market close on March 6, 2026, HL stock traded at $23.15, down 6% from $24.63 the prior day amid broader market weakness. Over five days, it held steady near $23, while the one-month trend shows a 9.37% gain, reflecting tailings progress at Greens Creek. The three-month trend climbed steadily, with six-month and year-to-date gains part of a 385.91% one-year total return, though recent dips signal caution. The 52-week high hit above $25, with a low near $15.84; overall, the trend leans bullish but sideways short-term, hinting at consolidation for patient investors.

Technical Analysis

Support levels sit at $22.96 (20-day MA) and $23.14 (50-day MA), key floors where buyers may step in to prevent deeper drops. Resistance looms near $25, the recent high that could cap upside without volume breakout.

RSI hovers around 56.6%, neutral—not overbought above 70 or oversold below 30—showing balanced momentum for beginners. MACD trends mildly bullish as lines converge positively, signaling potential upward shifts if volume rises. The 50-day MA ($23.14) sits just above the 200-day, no golden cross (bullish) or death cross (bearish) yet. Trading volume stays low on dips, lacking confirmation for sells, which matters as it flags weak conviction in down moves.

Analyst Ratings & Price Targets

Of 24 analysts covering HL stock, most lean “sector perform” or hold, with 4 Buy ratings noted recently. Average price target stands at $25, with highs at $28 and lows near $20; Scotiabank raised theirs to $25 from $15 in January 2026. No major upgrades this week, but sentiment improved post-2025 earnings. Wall Street views reflect optimism on silver output but caution on costs—this means moderate confidence, urging investors to weigh production beats against volatility.

Insider Activity

Recent SEC filings show limited large insider buys or sells in Q4 2025, with executives holding steady amid board changes. First Eagle Investment cut its stake by 8.2% in Q3 2025, selling 1.75 million shares, signaling some caution from big holders. No aggressive buying trends, implying neutral management confidence—watch for Q1 2026 filings to gauge if leaders add shares on dips.

Valuation Analysis

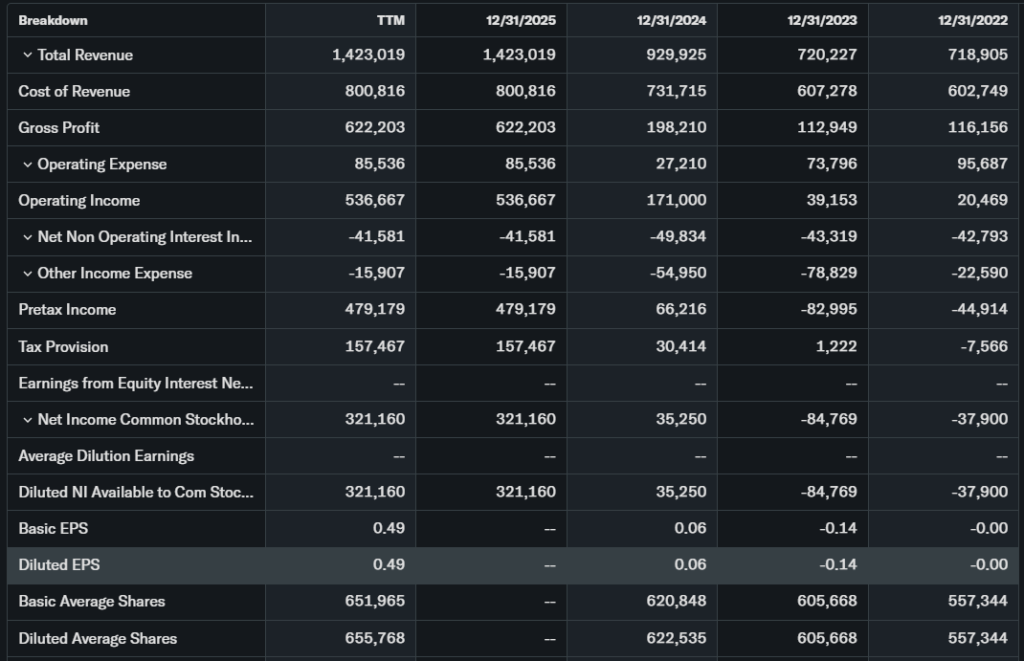

HL’s trailing P/E sits high due to earnings growth, with forward P/E more reasonable at around 20x expected 2026 EPS. Price-to-sales ratio appears attractive versus peers, backed by YoY revenue growth from higher silver volumes.

EPS grew strongly in 2025, with free cash flow improving on mine expansions; debt levels manageable, cash position solid post-guidance. Compared to silver peers like Pan American or Coeur, HL looks fairly valued—not screaming undervalued but not overpriced given 2026 output hikes. Overall, it trades at a balanced multiple for growth potential.

Recent Earnings & Catalysts

Hecla’s 2025 full-year earnings beat forecasts, driven by Greens Creek tailings progress and higher metal prices, with Q4 revenue topping expectations. EPS exceeded estimates, though exact beats tied to silver leverage; forward 2026 guidance lifted production targets. Key catalysts include AI-driven demand for silver in tech and new board additions for strategy. Post-earnings, HL stock surged 9% in a month, showing positive market reaction.

Bullish Case

Silver demand rises from solar panels and electronics, favoring HL’s low-cost Greens Creek output. 2026 guidance promises higher volumes, with operational tweaks cutting costs. Tech advantages in mine efficiency and U.S.-focused assets shield from global risks. Steady revenue growth could push shares higher if metals hold firm.

Bearish Case

Competition from larger miners pressures margins, while slowing silver price gains could hit revenue. Recent 6% plunge on low volume flags exhaustion; customer churn low but economic slowdowns curb industrial use. Regulatory hurdles at tailings sites add caution, plus broader metal market volatility under trade policies.

Market Sentiment & Investor Psychology

Short interest remains moderate at under 5%, with mixed options flow—calls edge puts slightly. Institutional ownership dipped with First Eagle’s trim, but overall steady; retail piles in on momentum. Sentiment tilts neutral to optimistic, blending value bias with short-term fear from dips.

Short-Term Outlook

Technicals point to tests at $22.96 support, with low volume suggesting range-bound action near $23. Momentum fades without catalysts, so expect sideways grind unless metals rally—realistic pause before next leg.

Medium to Long-Term Outlook

HL’s business model thrives on silver leverage, with industry growth from green tech. Competitive edge at premium mines and healthy balance sheet support accumulation. Long-term investors should hold or watch for dips to add, given forecast upside to $28.

FAQ Section

Is HL stock a buy right now?

Neutral hold; buy on dips below $23 if silver trends up, per analyst targets.

What is the price target for HL stock?

Average $25, high $28—tied to 2026 production beats.

What are major risks for HL stock?

Volume lulls, metal price drops, and mine delays.

What is HL earnings outlook?

2026 guidance strong, building on 2025 beats.

HL stock forecast for 2026?

Bullish to $28 on output growth, balanced risks.

Suggestions

- Compare with Opendoor stock analysis

- See our silver mining sector forecast

- Read Coeur Mining stock technicals

Conclusion

Hold for now, watchlist for dips. HL stock offers solid growth via silver exposure and earnings momentum, but short-term volatility warrants caution—strong fundamentals justify patience over aggressive buys.

Disclaimer: This article is for informational purposes only and not financial advice.