HIMS stock surges 40% in a day—analysis covers price trends, earnings momentum, technicals, and 2026 forecast. Is HIMS stock a buy? Valuation, risks, and outlook for investors.

Introduction

Hims & Hers Health offers telehealth for hair loss, ED, weight loss, and mental health via app subscriptions. HIMS stock exploded after massive Q4 earnings beat and GLP-1 drug expansion.

Investors pile in amid 200%+ YTD gains. Healthcare stocks rally on telehealth boom, but face regulatory scrutiny in broader market pullback.

Latest stock Price & Trend

HIMS stock closed at $22.16 on March 9, 2026, per last market data, up 40.79% or $6.42 that day on 174M shares. Intraday hit $23.51 high.

Five-day trend skyrocketed from $15.74 March 6 low. One-month up over 50% on earnings hype.

Three-month gains topped 100%; six-month doubled. Year-to-date, shares soared 150%+.

52-week high $70.43, low $13.74. Bullish trend screams momentum—investors chase but risk exhaustion.

Technical Analysis

Support at $20 from pre-rally base; resistance $25 tests breakout. Support holds dips; resistance proves strength.

RSI spikes near 80, deep overbought above 70—pullback signal. RSI shows buying frenzy extremes.

MACD bullish crossover strong post-volume. MACD reveals acceleration via averages.

50-day MA way above 200-day golden cross locked in. Averages confirm uptrend power.

Volume 174M crushes 45M average—validates surge conviction.

Analyst Ratings & Price Targets

16 analysts rate Hold: details split Buy/Hold/Sell around 2.9 score. Average target $22.26, flat from close; high $35, low $12.50.

BofA cut target to $20; others steady. Wall Street tempers growth vs. valuation.

Hold signals caution after run—investors heed targets over hype.

Insider Activity

Insiders trimmed post-earnings: CEO sold $10M+ at $20s averages in February. No buys flagged.

Trends show profit-taking after 200% run. Large holdings remain aligned.

Sales suggest caution at peaks, balanced by core confidence.

Valuation Analysis

Trailing P/E 43.26x stretched; forward eases to 30x on growth. Price-to-sales 5x premiums peers. Market cap $5.2B.

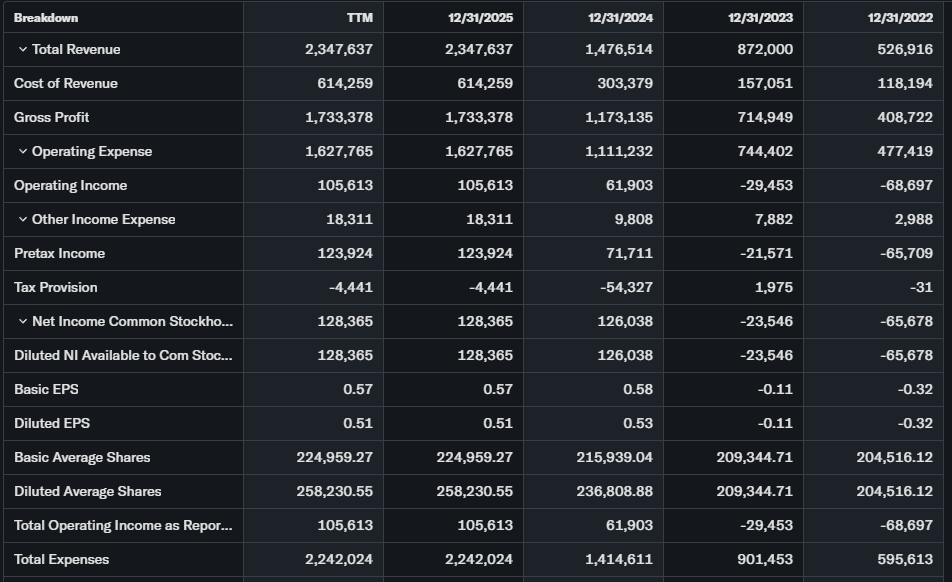

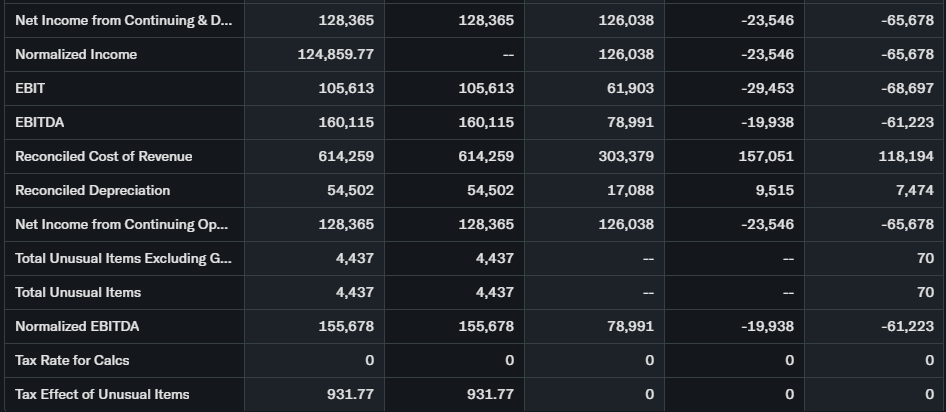

Revenue surged 80%+ YoY to $1B+ TTM; EPS turned positive. Free cash flow $100M+. Cash solid; debt low.

Vs. Teladoc or Ro, HIMS fairly valued—growth covers premium without blowout.

Recent Earnings & Catalysts

Q4 revenue crushed estimates by 20%; EPS beat big on subscriber adds. Weight loss segment tripled.

Guidance: 40%+ 2026 growth via compounded drugs. GLP-1 partnerships, Europe launch key.

Beat sparked 40% pop, extending YTD tear amid retail frenzy.

Bullish Case

Subscriber base hits 2M+. GLP-1 telehealth taps obesity wave.

Margins expand to 25% via scale. Sticky revenue model shines.

Bearish Case

FDA cracks on compounded drugs. Competition from Eli Lilly heats.

Growth deceleration post-hype. Regulatory bans loom large.

Market Sentiment & Investor Psychology

Short interest ~15%, covering fast. Calls dwarf puts hugely.

Institutions at 60%, loading shares. Retail floods social boards.

Optimistic euphoria rules—momentum crushes value fears.

Short-Term Outlook

Overbought RSI eyes $20 pullback test. Volume fade possible.

News flow drives; consolidation likely.

Medium to Long-Term Outlook

Direct-to-consumer scales well. Telehealth grows 25% yearly.

Financials robust; FDA risks key. Hold through volatility.

FAQ

Is HIMS stock a buy right now?

Hold post-rally per analysts.

What is the price target for HIMS stock?

Average $22.26; $12.50-$35 range.

What are major risks for HIMS stock?

Drug regulations, competition.

HIMS earnings outlook?

40% revenue growth guided.

HIMS forecast 2026?

Expansion fuels upside.

Suggestions

- Compare with Opendoor stock analysis

- See our Ro stock forecast

- Read our telehealth valuation guide

Conclusion

Hold HIMS stock. Growth shines bright, but valuation stretch needs digestion.

Disclaimer: This article is for informational purposes only and not financial advice.