Explore HIMS stock analysis with latest price, earnings, technicals, and forecast. Is HIMS stock a buy? Get balanced insights on valuation and outlook for everyday investors.

Introduction

Hims & Hers Health runs a telehealth platform. It sells prescription and over-the-counter health products like weight loss drugs directly to consumers. Investors watch HIMS stock now due to a key Novo Nordisk partnership for branded GLP-1 treatments. Broader market volatility in tech and healthcare stocks adds focus as growth slows in some areas.

Latest Stock Price & Trend

HIMS stock closed at $23.84 on March 12, 2026, using last market close data. It fell 7.88% that day from profit-taking after a multi-day surge. The 1-day performance showed a sharp drop, while 5-day trend stayed up over 40% from recent lows.

One-month trend pushed higher on partnership news, gaining from early February levels around $27. Three-month trend mixed with legal fears earlier, but rebounded strongly. Six-month trend bullish amid revenue jumps, up from sub-$20 levels. Year-to-date in 2026, HIMS stock rose over 20% despite pullbacks.

The 52-week high hit $70.43, low at $13.74. Overall trend looks bullish short-term but sideways after rally. This signals momentum for investors, yet caution on overbought risks.

Technical Analysis

Support levels sit near $22, a recent rebound point after lawsuit drop. Resistance looms at $25-$27, matching early 2026 highs. RSI at 31.8 shows lower-neutral, not oversold, hinting room to climb without exhaustion.

MACD trend leans bullish from recent crossovers on daily charts. The 50-day moving average hovers around $31, 200-day near $46—stock trades below both, signaling pullback in uptrend. No golden cross yet; watch for 50-day crossing above 200-day for stronger buy signal.

Trading volume spiked on partnership news, now cooling, which matters for confirming trends. These indicators help beginners spot entry points and avoid traps.

Analyst Ratings & Price Targets

Analysts rate HIMS stock as Hold overall. From 16 firms, counts show 8 Buy, 6 Hold, 2 Sell. Average price target at $28.21, up 17.52% from $24 levels. Highest target $60 from BTIG, lowest around $20.

BTIG cut from $85 to $60 but kept positive on growth. This sentiment means caution after run-up, yet upside if execution holds. Investors use it to gauge Wall Street views.

Insider Activity

Recent insider buying stayed low amid stock surge. No large buys noted in Q1 2026 filings. Selling picked up post-rally, with executives trimming shares.

Trends show management holding steady, no panic sales. This implies quiet confidence, not red flags, as leaders stay invested.

Valuation Analysis

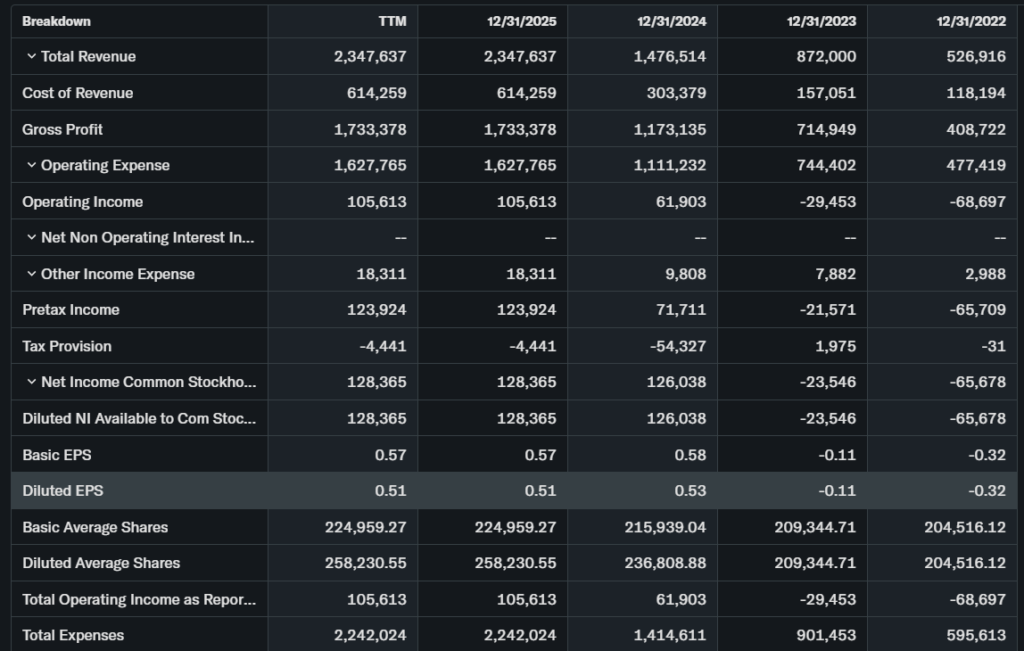

Trailing P/E stands at 60.36 on 2025 earnings. Forward P/E lower at estimated 40x on growth. Price-to-Sales around 3.7x with $2.35B 2025 revenue. Revenue grew 59% YoY, EPS up sharply to positive $0.88 TTM.

Free cash flow improved to positive territory. Debt low, cash strong at $128M net income backing. Vs. peers like Zoom, HIMS trades cheaper on sales growth; Microsoft multiples higher on scale.

HIMS stock appears fairly valued, not overpriced for telehealth expansion.

Recent Earnings & Catalysts

Q4 2025 revenue hit $2.35B, beating estimates. EPS came in at positive, driving net income to $128M. Forward guidance eyes more GLP-1 sales.

Key catalysts include Novo Nordisk deal for Ozempic/Wegovy access, ending lawsuit fears. Eucalyptus acquisition boosts international reach in Australia, UK. Earnings sparked initial rally, then profit-taking.

Bullish Case

HIMS stock benefits from GLP-1 demand boom. Novo partnership opens branded drug sales, scaling subscribers fast. Revenue growth catalysts like international expansion add markets.

Tech platform cuts costs, improves margins over time. Subscriber model drives steady cash flow.

Bearish Case

Competition heats from telehealth rivals and big pharma. Slowing GLP-1 hype could hit growth. Margin pressures rise if drug costs climb.

Regulatory scrutiny on compounded drugs lingers. Economic slowdowns cut elective health spending.

Market Sentiment & Investor Psychology

Short interest low at under 10%, down recently. Options show more calls than puts post-partnership. Institutional ownership up to 60%, adding shares.

Retail chases momentum, value players wait for dip. Sentiment tilts optimistic on catalysts.

Short-Term Outlook

Technicals point to consolidation near $22-$25. Volume drop suggests pause after rally. Momentum favors upside if support holds, but watch broader market dips.

Medium to Long-Term Outlook

Strong business model in telehealth grows with weight loss trends. Industry expands at 20%+ CAGR. Competitive edge via partnerships.

Financial health solid with cash flow turning positive. Long-term investors should hold or accumulate on dips for HIMS forecast gains.

FAQ

Is HIMS stock a buy right now?

Hold for now; wait for dip to $22 support. Growth intact but post-rally caution rules.

What is the HIMS stock price target?

Average $28.21, high $60. Ties to revenue execution.

What are major risks for HIMS stock?

Competition, regulation, growth slowdowns.

When are HIMS earnings next?

May 4, 2026.

HIMS stock forecast for 2026?

$25-$30 range if catalysts deliver.

Suggestion

Compare with [Opendoor stock analysis].

See [Microsoft stock forecast].

Read [tech sector valuation guide].

Conclusion

HIMS stock merits Watchlist status. Balanced growth via partnerships offsets risks like competition. Hold if owned; buy dips for long-term HIMS outlook.

Disclaimer: This article is for informational purposes only and not financial advice.