HIMS stock analysis including latest stock price, earnings, technicals, and forecast to help investors decide if Hims & Hers stock is a buy, hold, or watch.

Introduction

Hims & Hers Health (ticker: HIMS) is a digital‑health company that sells online medical care and products for men’s and women’s health, including hair loss, skin care, sexual health, and weight‑loss medications. The business has grown quickly by combining telemedicine with e‑commerce, and investors pay close attention to HIMS stock because of its exposure to fast‑growing digital health and obesity‑treatment markets.

Right now, sentiment around HIMS stock price is mixed: the stock has dropped sharply so far this year, but the company still reports strong subscriber growth and multi‑year revenue targets. Broader market worries about interest rates, regulation of compounded weight‑loss drugs, and valuation in high‑growth tech/health stocks also weigh on how traders view HIMS shares.

Latest HIMS stock price & trend

As of the last available market close, HIMS stock was trading around 27–28 dollars per share, after a volatile period that has seen the stock fall roughly 52% year‑to‑date in 2026. Over the past one day, shares have often moved up or down by a few percentage points depending on news flow; the most recent sessions show material intraday swings, reflecting elevated sentiment swings.

Over the last five days, HIMS has traded in a choppy but generally sideways‑to‑modestly‑up band, with prices fluctuating between roughly 26 and 29 dollars on intraday highs and lows. The one‑month trend is negative, with the stock down about 37–38%, underscoring selling pressure after a rich multi‑year run.

On a three‑month and six‑month basis, HIMS stock remains in a clear bearish secondary trend, as the stock retraces from much higher levels seen in prior years. For the full year so far, the move is sharply down, though the 52‑week high was notably above 50 dollars while the 52‑week low has dipped closer to the low‑20‑dollar range. Overall, the price action signals a bearish to neutral posture for the near term, with the main question being whether the stock can stabilize its HIMS valuation and build a new base.

Technical analysis of HIMS stock

For beginners, technical analysis looks at where the stock has traded and how trading volume and momentum signals behave. On the daily chart, HIMS shows clear support levels near the mid‑20s, where buying interest has previously appeared to cap deeper drops. Above that, resistance levels cluster around the 30–35 dollar zone, where offers have historically increased and rallies have often stalled.

The RSI (Relative Strength Index) for HIMS has recently hovered around the neutral 40–50 range, which is neither clearly overbought nor oversold. That suggests current momentum is flat to slightly weak, with no strong signal that the stock is due for a big rebound yet. The MACD (Moving Average Convergence Divergence) has also been mostly flat or slightly below the zero line, indicating a bearish to neutral momentum bias rather than a strong uptrend.

On moving averages, the 50‑day moving average now trades below the 200‑day moving average, forming a “death cross” pattern that historically hints at a longer‑term downtrend. Trading volume has been elevated on down days, which often reflects ongoing profit‑taking and short‑covering rather than a clean, stable accumulation phase. For investors, this technical picture implies that HIMS technical analysis points toward a consolidating or down‑trending phase, not a clear bullish breakout yet.

Analyst ratings & price targets for HIMS stock

Wall‑street coverage remains active on HIMS, with roughly 20–25 analysts following the stock across major firms. The distribution of ratings is typically a mix of Buy, Hold, and a smaller number of Sell‑type opinions, leaning toward a cautiously optimistic but divided stance.

Recent average 12‑month price targets for HIMS stock cluster in the mid‑20s to low‑40s, with some optimistic targets still above 50–60 dollars if the company executes its growth plan. The highest current targets are usually from banks that emphasize long‑term digital‑health and weight‑loss upside, while the lowest come from more conservative voices focused on valuation and regulatory risk.

A few notable brokerages have recently trimmed their HIMS forecast and price targets, particularly after the stock ran up in prior years and then sold off sharply. Despite those cuts, several firms still maintain Overweight or Buy ratings, arguing that HIMS valuation may now be more realistic relative to its growth prospects. For investors, this split coverage signals that the stock is not universally loved, but many analysts still see a path to higher prices if execution and margins improve.

Insider activity around HIMS stock

Insider activity for HIMS includes both executive purchases and sales, with some management figures periodically selling shares after vesting or during open‑market windows. Recent filings show that insiders have used sales to diversify personal wealth, while occasionally participating in limited buybacks or long‑term retention plans.

There is also evidence of board‑level and senior‑management confidence through continued share ownership and long‑term incentive grants, even as the stock has corrected sharply. Large transactions are usually disclosed in SEC filings, and when insiders add to positions after sell‑offs, it can signal management believes the current HIMS stock price is too low relative to the business’s fundamentals.

Overall, insider activity tilts closer to neutral to mildly positive: not a clear wave of buying, but also no mass exodus that would suggest extreme caution. For retail investors, this pattern supports treating HIMS as a speculative growth name rather than a classic “insider‑backed” turnaround.

Valuation analysis of HIMS stock

From a valuation standpoint, HIMS no longer trades at the extreme multiples it once did. Current trailing and forward metrics show the stock is priced more in line with mid‑tier growth rather than pure‑internet‑boom levels. The trailing P/E and forward P/E are still elevated compared with traditional healthcare peers, but lower than where they stood during the prior blow‑off phase.

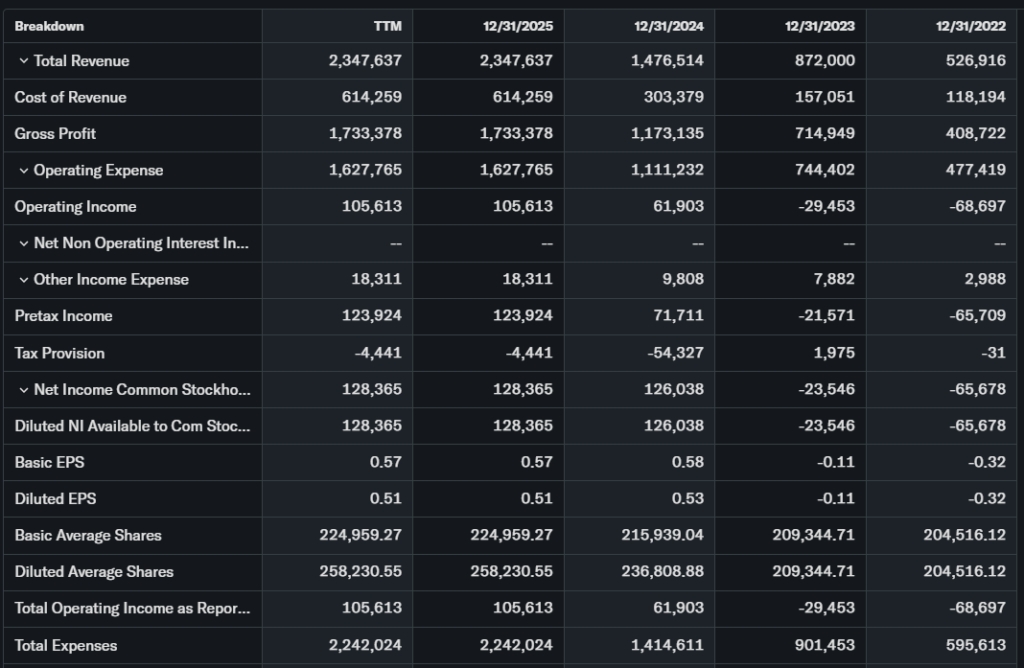

The price‑to‑sales (P/S) ratio has also compressed, reflecting both the drop in HIMS stock price and the company’s continued expansion of revenue. Revenue growth remains strong, with HIMS revenue growth running well into the mid‑double digits year‑over‑year, driven by new product lines and international expansion. Earnings per share (HIMS earnings) have turned positive in recent quarters, improving the EPS growth trajectory versus earlier losses.

On the balance sheet, HIMS carries moderate debt and a meaningful cash buffer, giving it flexibility to fund new initiatives and acquisitions. Compared with other digital‑health or telehealth‑style names, HIMS still looks somewhat rich on growth metrics, but less overvalued than it did a year ago. Overall, the valuation appears fair‑to‑slightly rich, not cheap, for a stock with high growth but also meaningful regulatory and competitive risk.

Recent HIMS earnings & catalysts

In the latest quarter, HIMS quarterly results showed revenue of about 618 million dollars, up roughly 28% year‑over‑year, though slightly below the consensus estimate of around 619 million dollars. Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) nearly doubled, pointing to improving operating leverage from scale.

The company also reported a subscriber base of about 2.5 million, up about 13% year‑over‑year, which supports recurring‑revenue potential. Management’s forward guidance for 2026 forecasts revenue in a range of roughly 2.7–2.9 billion dollars, above current analyst expectations, and the company reiterated a long‑term goal of crossing 6.5 billion dollars in revenue by 2030.

Key catalysts include new service lines, AI‑driven triage tools, and an upcoming acquisition of Eucalyptus, an Australian digital‑health firm, which could expand HIMS’s non‑weight‑loss portfolio and international footprint. These moves may help offset regulatory and pricing pressure in the GLP‑1‑style weight‑loss segment, which remains a major but controversial driver of HIMS revenue growth.

Bullish case for HIMS stock

Several realistic factors support a constructive view on HIMS stock over the medium term. First, the digital‑health and telehealth markets are expected to keep growing as patients accept online care for routine conditions and chronic‑disease management. HIMS’s multi‑specialty platform in men’s and women’s health gives it a broad base beyond just weight‑loss drugs, which may help diversify risk.

Second, the company’s subscriber growth and revenue growth suggest that demand for its products remains strong, even as the market worries about regulatory overhang. Management’s stated goal of 6.5 billion dollars in revenue by 2030 implies a multi‑year runway, assuming margins and cash‑flow conversion improve.

Finally, operational improvements in customer acquisition costs, retention, and brand recognition could help HIMS expand margins and free cash flow over time. If the company executes consistently, HIMS technical analysis and valuation could shift toward a more balanced or even bullish stance.

Bearish case for HIMS stock

On the downside, several credible risks cloud the HIMS story. Competition is intense, with large pharmacy chains, tech giants, and traditional insurers entering digital‑health and tele‑medicine arenas, which could pressure pricing and margins. Regulatory scrutiny of compounded weight‑loss medications and insurance‑reimbursement rules also creates uncertainty around the most profitable segment of HIMS revenue growth.

The stock’s sharp 2026 year‑to‑date decline also reflects investor fear that prior growth expectations may have been too optimistic. If macroeconomic conditions tighten or interest‑rate expectations rise, high‑growth, modest‑profit names like HIMS can underperform broader markets again. Customer churn and changing insurance coverage for telehealth visits could further pressure renewal rates and long‑term value per subscriber.

Market sentiment & investor psychology

Short‑interest data for HIMS suggests only a moderate level of short bets, not the extreme levels sometimes seen in heavily contested growth names. Options activity shows a mix of puts and calls, with some positioning around earnings and regulatory announcements, implying traders are hedging rather than blindly betting on a bounce.

Institutional ownership has pulled back somewhat from prior highs, as the stock has corrected and some funds rebalanced toward more defensive healthcare or value‑oriented names. Retail investors appear cautiously divided: some see the pullback as a buying opportunity, while others fear more downside if weight‑loss or regulatory headwinds intensify.

Overall, sentiment sits between fearful and neutral, with a tilt toward waiting for clearer evidence that HIMS can sustain both growth and profitability without regulatory shocks.

Short‑term outlook for HIMS stock

Over the next days and weeks, HIMS technical analysis suggests the stock is likely to trade in a narrow band, roughly between the mid‑20s support and the low‑30s resistance, unless a major news catalyst appears. With the MACD and RSI near neutral, there is no strong momentum signal pointing clearly up or down, and volume remains event‑driven.

If sector‑wide tech or healthcare sentiment strengthens and volatility subsides, HIMS could gradually grind higher toward previous resistance zones. However, if regulatory news or earnings revisions disappoint, the stock could retest the lower end of its recent range. In either case, traders should watch support and resistance levels and not expect a sharp, one‑way move without a clear trigger.

Medium to long‑term outlook

Over the next 6–24 months, the long‑term outlook for HIMS hinges on three factors:

- Can the company maintain double‑digit revenue growth while expanding margins?

- Can it navigate regulatory and pricing risks in the weight‑loss segment?

- Can it keep building a diversified digital‑health platform that is not overly dependent on one product line?

If HIMS executes reasonably well on these fronts, the stock could stabilize and gradually move higher as HIMS valuation expands with earnings and cash flow. However, if growth slows or regulatory headwinds bite into profits, the stock could stay range‑bound or drift lower. For long‑term investors, the balanced conclusion is: HIMS stock may be more suitable for a watchlist or staggered accumulation, rather than an aggressive all‑in bet, until the business model and regulatory environment feel more settled.

FAQ: Common questions about HIMS stock

Is HIMS stock a buy right now?

Many analysts see HIMS as speculative but not obviously cheap or expensive; a cautious, staggered approach may be more appropriate than a full‑size position.

What is the price target for HIMS stock?

Current 12‑month price targets range roughly from the lower‑20s on the downside to the 50–60s on the upside, with an average often in the mid‑30s, implying modest to moderate upside from today’s levels.

What are major risks for HIMS stock?

Key risks include regulatory pressure on compounded weight‑loss drugs, competition from larger healthcare and pharmacy players, and the possibility of slower growth or margin pressure if demand moderates.

What is HIMS stock price doing recently?

HIMS stock has fallen sharply year‑to‑date in 2026, after a strong prior run, leaving the share price in the mid‑20‑dollar range as of the latest close.

What does HIMS technical analysis say?

Charts show the stock near key support in the mid‑20s, with resistance around 30–35 dollars, and momentum indicators around neutral, suggesting a consolidation phase rather than a clear breakout.

suggestions

- Compare with Opendoor stock

- See our digital health sector valuation breakdown

- Read our GLP‑1 weight‑loss drug market overview

Disclaimer: This article is for informational purposes only and not financial advice.