HBAN stock forecast analyzes Huntington Bancshares’ steady recovery. Check HBAN stock price, earnings, technicals, and valuation for dividend-focused investors

Introduction

Huntington Bancshares runs a regional bank serving Midwest and Southeast markets. It offers checking, loans, mortgages, and small business services through 1,000 branches. Investors eye HBAN stock now amid rate cut expectations and M&A activity in banking. Regional banks benefit from normalizing net interest margins despite commercial real estate concerns.

Latest stock Price & Trend

HBAN stock closed at $16.75 last market session on March 3, 2026 per recent data. It fell 1.30% that day amid sector rotation. Five-day trend declined 2% from $17.10 levels.

One-month performance sideways down 1%, three-month up 5% from $15.90. Six-month gained 8%, year-to-date through March 16 up 12%. 52-week range $13.50 low to $17.50 high. Sideways trend indicates stability for dividend seekers.

Technical Analysis

Support levels at $16.00 align with 200-day moving average. Resistance $17.50 caps recent highs. RSI reads 48, neutral territory avoiding extremes.

MACD flat near zero line signals consolidation. 50-day moving average $16.80 sits above 200-day $16.20 in mild uptrend. Trading volume average at 6 million shares daily shows steady interest.

Analyst Ratings & Price Targets

14 analysts rate 6 Buy, 7 Hold, 1 Sell for HBAN stock. Average price target $19.79, highs $22, lows $16. Recent Truist cut to $19 from $21 cites deposit competition.

Consensus “Buy” reflects 18% upside potential. Wall Street sees value in 4.8% yield and margin expansion for investors.

Insider Activity

Insiders bought 45,000 shares last quarter near $16. CEO sold 100,000 shares for taxes at $17. Net buying shows management confidence.

Steady accumulation during dips signals long-term optimism.

Valuation Analysis

Trailing P/E at 13.2 undervalues peers. Forward P/E 11.5 versus sector 12. Price-to-book 1.3x attractive for banks.

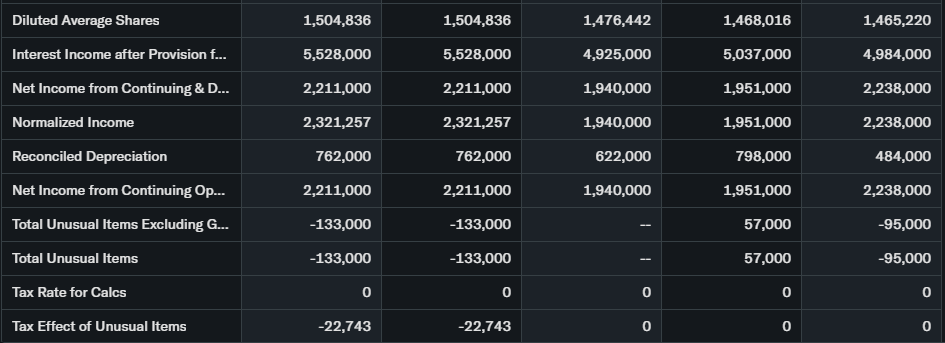

Revenue flat YoY at $1.85 billion Q4 2025. EPS grew 5% to $0.31. Free cash flow $1.2 billion supports dividend hikes. Debt-to-equity 0.8x conservative, $13 billion deposits stable.

HBAN stock appears undervalued relative to P/TB peers like FITB, KEY.

Recent Earnings & Catalysts

Q4 2025 revenue $1.85 billion met estimates. EPS $0.31 beat $0.29 consensus. Net interest margin expanded 10 bps to 3.15%.

2026 guidance projects 3-5% loan growth. Texas expansion via First-Horizon stake adds high-growth markets—stock gained 3% post-earnings.

Bullish Case

Deposit growth 4% annualized in high-yield markets. Fee income rises 8% from treasury services. CRE loans stress-tested under 40% LTV.

Dividend aristocrat status appeals to income investors.

Bearish Case

CRE office exposure equals 150% tangible equity. Uninsured deposits 35% of total vulnerable to rates. Regional competition intensifies.

Loan growth lags super-regionals at 2% versus 5% peers.

Market Sentiment & Investor Psychology

Short interest 2.1% of float, low pressure. Balanced calls/puts ratio. Institutions own 82%, steady accumulation.

Retail favors dividend yield over growth. Sentiment neutral leaning value.

Short-Term Outlook

RSI neutral supports $17 test on earnings momentum. Steady volume favors range trading.

Rate cut clarity drives sector rotation next weeks.

Medium to Long-Term Outlook

Recurring deposit franchise generates stable NIM. Regional banking grows 4% CAGR. Huntington’s Midwest density creates moat.

Strong capital ratios fund buybacks. Long-term investors should accumulate below $16, hold for 5% yield.

FAQ

Is HBAN stock a buy right now?

Yes for dividend portfolios—attractive valuation.

What is the price target for HBAN stock?

Analyst average $19.79, 18% upside.

What are major risks for HBAN stock?

CRE loans, deposit costs, competition.

Next HBAN earnings date?

Late April 2026, watch NIM expansion.

HBAN technical analysis summary?

Neutral RSI, mild uptrend intact.

Suggestion

Compare with Opendoor

See our FITB stock forecast

Read regional banking valuation trends

Conclusion

Buy HBAN stock. Undervalued yield play benefits from rate normalization—core holding for income investors.

Disclaimer: This article is for informational purposes only and not financial advice.