Latest CRWV stock price, technicals, earnings growth, and forecast. Is CRWV stock a buy in AI infra? Balanced CoreWeave analysis with targets and risks 2026.

Introduction

CoreWeave provides cloud computing for AI workloads, renting GPUs to model trainers. CRWV stock volatility spikes on AI demand and recent 18% drop amid sector rotation. Tech faces profit-taking after 2025 rallies, with rates impacting growth names.

Q3 revenue backlog highlights demand, but losses persist.

Latest Stock Price & Trend

CRWV closed at $79.50 February 27, down from $97.63 prior amid high volume 30M shares. One-day range $78.87-$89.11, net -18.5% implied from open $84.22.

Five-day volatile with 14.79% weekly gain pre-drop; one-month sideways, three-month down from peaks. Six-month bearish post-IPO hype fade; YTD mixed in 52-week $33.52 low to $187.00 high.

Trend sideways-to-bearish, signaling caution for chasers but opportunity near lows.

Technical Analysis

Support at $78.87 intraday low and $33.52 yearly bottom cushions falls. Resistance $89.11 recent high, $187 tests strength.

RSI (14) 52.43 neutral, balanced after swings. MACD unspecified but volatility beta 0.40 suggests steady under market.

50-day/200-day MAs not detailed; no cross noted. Volume 30M vs. avg 23M confirms selloff conviction.

Analyst Ratings & Price Targets

35 analysts average $125.59 target (high $200 Argus, low $32 HSBC), 30% upside from $77.75. Recent Mizuho neutral $95, Truist/DA Davidson holds; Deutsche up to $140 Jan.

Mostly buy/hold mix. Sentiment bullish on AI tailwinds, guiding investors to growth despite risks.

Insider Activity

Limited recent SEC buys/sells detailed; Form 4 routine post-IPO. Trends stable per filings, no panic dumps.

Holdings align with expansion; implies confidence in GPU demand ramp.

Valuation Analysis

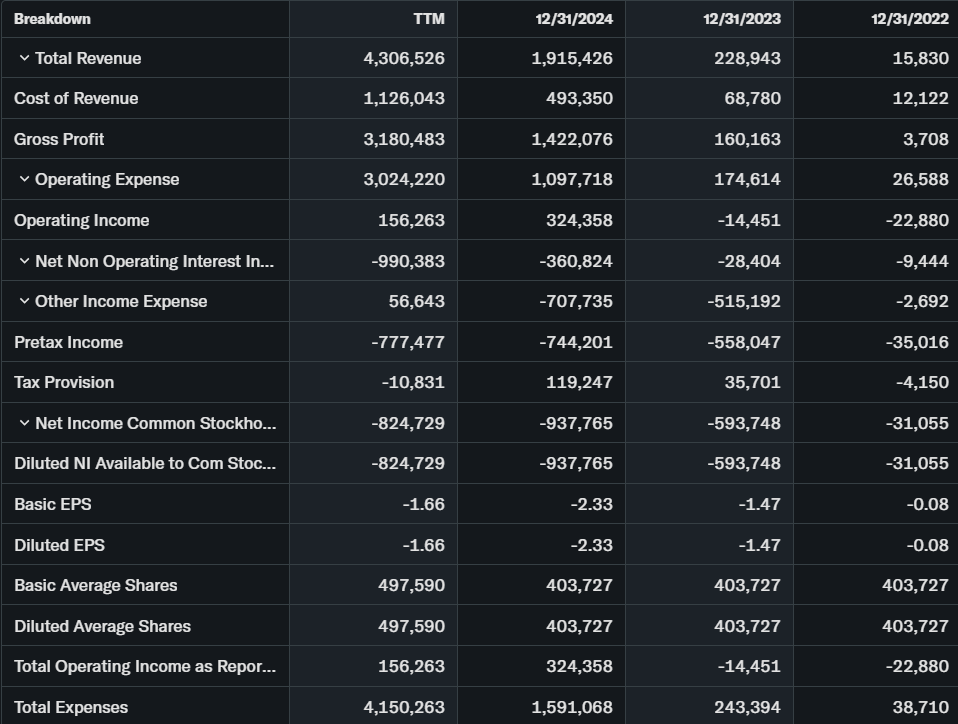

Trailing P/E -53.71 reflects losses; forward premium on revenue. P/S high ~20x TTM $4.3B revenue (235% YoY).

EPS diluted -2.32 TTM, FCF -8B heavy capex, debt elevated cash burn. Vs. AWS peers or Nvidia ecosystem, overvalued on profits but growth-justified. Appears overvalued absent margin inflection.

Recent Earnings & Catalysts

Q1 2025 revenue $981.6M (vs. -$314M net), Q4’24 $747M up big YoY. Losses widened on R&D/capex; backlog record signals demand.

GPU supply pacts with Nvidia, AI hyperscaler deals catalysts. Stock dipped on execution fears despite beats.

Bullish Case

AI compute shortage drives bookings. Revenue backlog unprecedented.

Nvidia ties secure supply. Gross margins 74% scale with utilization.

Bearish Case

Capex burn erodes FCF; competition from hyperscalers intensifies. Loss trajectory pressures amid rate hikes.

Customer concentration risks; regulatory AI scrutiny grows.

Market Sentiment & Investor Psychology

Short interest 8.53% (33M shares) up 25%, moderate bets against. Options volume high calls historically.

Institutions build; retail AI frenzy cools. Optimistic long but fearful near-term on valuation.

Short-Term Outlook

Neutral RSI, volume surge eyes stabilization; momentum fade risks tests support.

Medium to Long-Term Outlook

AI infra moat strong in exploding market. Finances strained by invest; hold for AI conviction, accumulate lows.

FAQ

Is CRWV stock a buy right now? Analyst buy tilt, but valuation high—wait for pullback.

What is the price target for CRWV stock? Avg $126, high $200.

What are major risks for CRWV stock? Losses, competition, capex drain.

CRWV earnings next? Q4 focus backlog conversion.

CRWV forecast long-term? Revenue hypergrowth if AI sustains.

Suggestions

- Compare with Opendoor

- See our Microsoft stock forecast

- Read our AI cloud sector breakdown

Final Balanced Conclusion

Watchlist CRWV stock; AI potential huge but profitability key amid overvaluation.

Disclaimer: This article is for informational purposes only and not financial advice.