CRDO stock analysis with price, earnings, valuation, forecast, and technical signals to see if Credo Technology stock is a buy for short and long-term investors.

Introduction

Credo Technology Group Holding Ltd, traded under the ticker CRDO, designs high-speed connectivity solutions used in data centers, AI infrastructure, and networking equipment. It focuses on energy-efficient, high-speed chips and optical solutions that help large cloud providers move data faster and at lower power.

Many investors are watching CRDO stock now because the company has posted very strong revenue and earnings growth tied to AI and data center demand. At the same time, the broader tech sector has been volatile as investors digest interest rate expectations and shifting sentiment toward growth stocks. These cross-currents make a careful look at CRDO stock especially important for everyday investors.

Latest Stock Price & Trend

At the last market close, CRDO stock traded around the low‑$110s per share, with after-hours moves briefly pushing it closer to the $100–$104 range following its latest earnings release. The stock fell roughly 8–13% in extended trading even though the company reported results that beat Wall Street expectations, highlighting how sensitive the market is to guidance and concentration risks. On a one-day basis, that means CRDO stock price showed notable downside volatility after the earnings event.

Over the past five trading days, the stock had been relatively strong heading into the report, as investors positioned for another robust quarter from Credo Technology. Over the past month, CRDO has seen a strong uptrend thanks to optimism around AI-related spending, with occasional pullbacks around news and macro headlines. On a three-month view, the stock has delivered significant gains, reflecting the market’s recognition of rapid revenue and earnings growth.

Looking at the past six months and year-to-date performance, CRDO stock price has moved sharply higher as the company shifted from a smaller niche player to a recognized beneficiary of AI data center build-outs. The shares have traded in a wide 52‑week range, from roughly the low double digits at the lower end to well above $100 at the high end, underscoring both the opportunity and the risk embedded in the name. Overall, the trend direction remains bullish on a multi‑month view, but the post‑earnings drop shows that volatility is likely to stay elevated and that investors must be ready for sharp swings.

Technical Analysis

Technical analysis looks at price charts and trading patterns to understand market behavior. For CRDO stock, nearby support levels can be found around recent consolidation zones and prior breakout areas, likely in the zone just above recent post‑earnings lows near the $100–$104 area. Support is a price region where buyers have historically stepped in, helping prevent further declines. Key resistance levels appear near recent highs in the $110–$120 area, where sellers previously took profits and where rallies can stall.

The Relative Strength Index (RSI) measures whether a stock is overbought or oversold on a scale from 0 to 100. An RSI above 70 often signals overbought conditions, while below 30 suggests oversold conditions. CRDO’s RSI recently moved into an overbought region before the latest pullback, indicating that the stock had run ahead of itself in the short term and was vulnerable to a correction or sideways consolidation.

The MACD (Moving Average Convergence Divergence) compares shorter- and longer-term moving averages to gauge momentum. A bullish MACD occurs when the short-term line is above the long-term line, while a bearish one is the opposite. Before earnings, CRDO’s MACD trend was broadly bullish, reflecting strong momentum, although the post‑earnings volatility may start to flatten or modestly weaken that signal in the near term.

The 50‑day and 200‑day moving averages track intermediate and long-term trends. When the 50‑day moves above the 200‑day, it is called a “golden cross” and often signals a longer-term bullish phase. CRDO stock has been trading above both its 50‑day and 200‑day moving averages, suggesting an ongoing uptrend supported by strong fundamental news. This setup resembles or approaches a golden-cross style structure, which typically supports a positive intermediate outlook.

Trading volume in CRDO has spiked around earnings releases and major news, signaling high investor interest and active debate about the stock’s fair value. Sustained elevated volume often means that big institutions and traders are actively positioning, which can amplify both upside rallies and downside corrections. For beginners, these technical signals suggest that CRDO stock technical analysis points to a strong but volatile uptrend that requires discipline and clear risk management.

Analyst Ratings & Price Targets

Wall Street coverage of Credo Technology frames it as a high-growth semis and connectivity play tied to AI and cloud demand. Major research firms and brokerage analysts generally lean toward positive ratings, with a majority in the Buy or Outperform category and a smaller portion at Hold, and very few outright Sell calls. The average analyst price target sits below the recent 52‑week high but above current trading levels, suggesting moderate upside potential over the next 12 months.

Within that, the highest price targets imply more aggressive expectations for continued AI-driven revenue growth and margin expansion, while the lowest targets bake in more conservative assumptions and greater risk around customer concentration. Analyst commentary following the recent earnings report has highlighted both the impressive revenue and EPS beat and the concerns about heavy reliance on a small number of large customers. Some firms have reiterated Buy ratings but with cautious language, while others have maintained more neutral stances, reflecting a balanced, but still constructive, sentiment.

For everyday investors, this means analyst sentiment on CRDO stock is broadly positive but not universally enthusiastic. CRDO stock forecast ranges show that professionals see meaningful upside if execution continues, but they also recognize that the risk profile is higher than more diversified, mature tech names.

Insider Activity

Insider activity refers to trading by company executives, directors, and large beneficial owners. When insiders buy, it can indicate confidence in the company’s future; when they sell, it can sometimes signal caution, though sales can also be for personal diversification or tax reasons. Recent filings show that Credo Technology insiders and major shareholders have periodically sold shares, often linked to stock-based compensation vesting or planned selling programs.

At the same time, there is limited evidence of large, open-market insider buying at recent elevated prices, which is not unusual after a strong run-up. The pattern appears more like regular liquidity events than sudden, large bearish bets by management. For investors, current insider activity skews slightly toward selling rather than buying, which is worth monitoring but not, on its own, a clear negative signal. It does, however, remind investors that much of management’s wealth is still tied to the company’s long-term performance.

Valuation Analysis

Credo Technology’s valuation reflects its rapid growth and exposure to AI and high-speed connectivity, and it trades at a premium compared with many more mature tech firms. Trailing and forward price-to-earnings (P/E) ratios on CRDO are significantly higher than those of large-cap software and hardware leaders like Microsoft, and often above levels seen at more established communication chip peers. Its price-to-sales (P/S) multiple is also elevated, implying that investors are willing to pay a high price for each dollar of current revenue because they expect strong future growth.

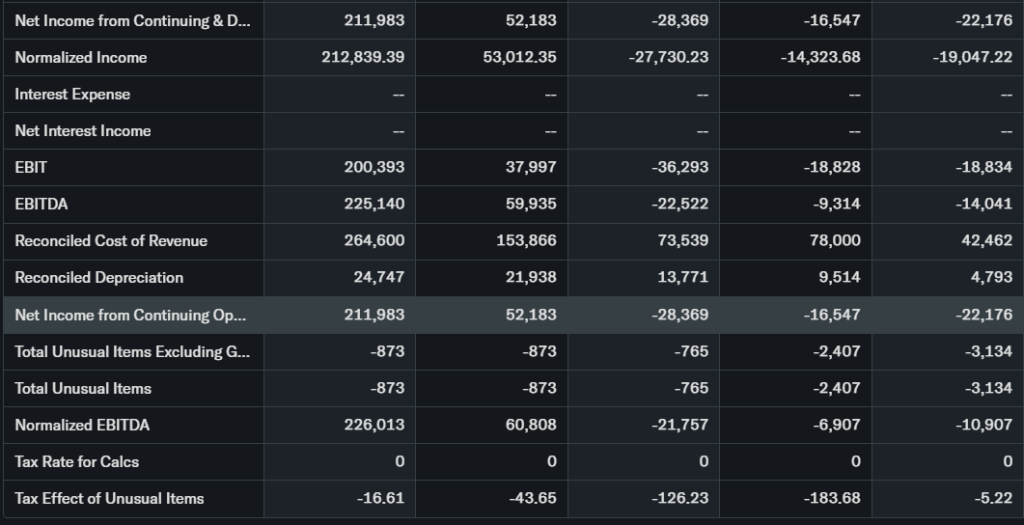

Fundamentally, the company has delivered exceptional revenue growth. In its most recent quarter, Credo reported revenue of about $407 million, up more than 50% sequentially and more than 200% year over year, underscoring explosive expansion. Non‑GAAP EPS jumped to around $1.07, far above the roughly $0.25 level a year earlier, showing dramatic earnings leverage. The company also posted non‑GAAP gross margins in the mid‑to‑high 60% range, highlighting strong pricing power and product differentiation.

Credo’s balance sheet is another strength. The company holds a sizeable cash and short-term investment position of roughly $1.3 billion, giving it ample resources to invest in R&D, capacity, and strategic initiatives. Inventory levels have risen as Credo supports surging demand, but its free cash flow profile has improved alongside earnings growth. Compared with slower-growing tech giants such as Microsoft or communication equipment players with more moderate growth, CRDO’s valuation can appear rich on standard metrics.

Putting it together, CRDO stock valuation looks more aggressive than many peers but is partly supported by exceptional growth and high margins. Given the premium multiples and concentration risks, the stock appears closer to fully valued to modestly overvalued rather than clearly cheap, especially if growth normalizes.

Recent Earnings & Catalysts

Credo Technology’s latest quarterly earnings were a major catalyst for CRDO stock price. The company reported fiscal Q3 2026 revenue of about $407 million, beating consensus estimates that were closer to the high‑$300 million range. Year over year, revenue grew more than 200%, and sequential growth exceeded 50%, driven by strong demand from AI data centers and high-speed networking customers. Non‑GAAP EPS reached around $1.07, surpassing expectations near $0.90 and marking a huge increase from roughly $0.25 a year earlier.

Despite these robust numbers, CRDO stock fell after hours as investors reacted to modestly slower, though still solid, sequential growth guidance for the upcoming quarter and to the concentration of revenue among a small set of large customers. For Q4, management guided revenue to roughly $425–$435 million, implying mid single‑digit sequential growth, and projected non‑GAAP gross margins in the mid‑60% range. These figures still point to a healthy business but suggest that the explosive acceleration may be normalizing.

Key catalysts include expanding AI workloads, new product launches in optics and gearboxes, and deepening relationships with large hyperscale customers. The company’s strong cash position allows it to continue investing in new technologies and capacity to serve this growing market. Overall, the earnings report confirmed the strength of Credo’s business but also highlighted how high expectations and customer concentration can weigh on the CRDO stock forecast in the short term.

Bullish Case

The bullish case for CRDO stock centers on several factors:

- Rapid revenue and earnings growth driven by AI data centers, cloud providers, and high‑speed networking demand.

- Strong non‑GAAP gross margins in the mid‑60% range, reflecting product differentiation and pricing power in advanced connectivity solutions.

- A significant cash and short-term investment balance of around $1.3 billion, giving the company financial flexibility to fund R&D, capacity expansion, and potential strategic moves.

- Technology advantages in power-efficient, high-speed connectivity components that are increasingly critical for AI workloads and modern data centers.

If Credo continues to gain share in AI-related infrastructure and maintains high margins, long-term revenue and EPS growth could remain robust. In that scenario, CRDO stock price could justify its elevated valuation, and further upside becomes possible over time.

Bearish Case

The bearish case focuses on equally real risks:

- Heavy customer concentration, with a large portion of revenue coming from a small number of hyperscale clients, raises the risk that any slowdown or shift in orders could have a major impact.

- Growth may decelerate from extremely high rates to more moderate levels as the company scales, which could pressure the premium valuation.

- Competition in high-speed connectivity and AI infrastructure is intense, with larger, well-funded rivals capable of reducing Credo’s pricing power over time.

- Margin pressures could emerge if customers negotiate harder, if new technologies require heavy R&D investment, or if the product mix shifts.

- Broader macroeconomic or regulatory concerns affecting tech spending could also hurt demand, particularly if cloud or AI capital expenditures slow.

If any of these risks materialize, CRDO stock could see multiple compression and sharper drawdowns, especially given how far it has already run.

Market Sentiment & Investor Psychology

Market sentiment toward CRDO stock currently appears mixed but still tilted positive. The strong fundamental results have attracted growth investors and AI-focused funds, while the sharp post‑earnings pullback shows that some traders are quick to take profits or reduce risk. Short interest, while not extreme based on available data, indicates that some market participants are betting on downside or at least hedging their positions.

Options activity around earnings has involved elevated volumes in both calls and puts, reflecting speculation on near-term moves rather than purely long-term positioning. Institutional ownership has been rising as more funds add Credo Technology to their AI and high-speed connectivity baskets, but retail investors have also been active, drawn by headline growth rates and CRDO stock forecast commentary.

Overall, sentiment can be described as cautiously optimistic. Many see CRDO as a high-growth, high-risk play, and price action reflects a momentum bias with bouts of volatility rather than a steady value-oriented pattern.

Short-Term Outlook

In the short term, over the next several days and weeks, CRDO stock is likely to remain volatile as the market digests the latest earnings and guidance. Technical indicators such as RSI and MACD suggest that the stock was recently overbought and is now in a phase of consolidation or modest correction. Trading volume spikes around earnings show that both bulls and bears are active, and near-term direction may depend on how investors interpret subsequent analyst notes and sector news.

Given current levels and the recent pullback, a realistic expectation is for CRDO stock price to trade in a range, with support near recent lows and resistance around prior highs. Short-term traders may look to key support and resistance levels, along with CRDO stock technical analysis indicators, to time entries and exits. However, sudden news about AI demand, large customer orders, or macro factors could easily push the stock out of any expected range.

Medium to Long-Term Outlook

Looking out 6–24 months, the story for CRDO stock depends heavily on the durability of AI-driven data center spending and Credo’s ability to maintain its technology edge. The company’s business model—selling high-speed, power-efficient connectivity solutions—sits at the heart of growing AI and cloud workloads. Industry growth for AI infrastructure remains robust, and Credo appears well-positioned to benefit if it continues to execute.

The firm’s balance sheet strength, high margins, and strong revenue growth suggest solid financial health and an ability to invest through cycles. Competition and customer concentration remain key risks, but successful diversification of the customer base and continued product innovation could help mitigate them over time.

For long-term investors, CRDO stock may fit best as part of a diversified portfolio for those comfortable with volatility. Given the premium valuation and risk factors, a balanced view would lean toward a Hold to gradual Accumulate stance on pullbacks for investors with a multi‑year horizon who believe in the AI infrastructure theme.

FAQ Section

1. Is CRDO stock a buy right now?

CRDO stock offers strong growth and high margins but trades at a premium valuation and carries concentration risk. For aggressive, long-term investors comfortable with volatility, it may be a selective buy on dips. More conservative investors may prefer to watch or hold existing positions.

2. What is the price target for CRDO stock?

Analyst price targets for CRDO stock generally sit above current prices but below recent highs, implying moderate upside over the next 12 months if execution remains strong. Targets vary widely depending on assumptions about AI spending and customer concentration.

3. What are major risks for CRDO stock?

Key risks include reliance on a small number of large customers, potential growth deceleration, intense competition, and broader macro or tech spending slowdowns. These factors could pressure both earnings and valuation.

4. How are CRDO earnings trending?

Credo’s latest quarter delivered revenue of about $407 million and non‑GAAP EPS near $1.07, both well above year‑ago levels and consensus forecasts. Guidance still points to growth, though at a more moderate sequential pace.

5. What is the long-term outlook for CRDO stock?

Over the long term, CRDO’s fate depends on sustained AI and data center demand, its ability to diversify customers, and its continued technology leadership. If these factors hold, the long-term outlook is constructive but high-risk.

Suggestions

You can internally link to related content such as:

- “Compare with Opendoor stock”

- “See our Microsoft stock forecast”

- “Read our tech sector valuation breakdown”

These links help readers place CRDO stock valuation and growth in a broader tech and AI context.

Final Balanced Conclusion

CRDO stock stands at the intersection of powerful AI and data center trends, with exceptional recent revenue and earnings growth, strong margins, and a robust balance sheet. At the same time, the shares already price in a lot of optimism and face real risks from customer concentration, competition, and potential growth normalization.

Balancing these factors, CRDO stock currently looks best categorized as a Hold for existing shareholders and a candidate for watchlists or selective accumulation on meaningful pullbacks for new investors. The long-term opportunity is attractive but carries above-average risk.

Disclaimer: This article is for informational purposes only and not financial advice.