BKNG stock surges 6.4% to $4,526 amid stock split news and strong earnings. Explore BKNG stock price trends, analyst targets at $5,886, and 2026 forecast for investors.

Introduction

Booking Holdings Inc., known as BKNG stock, runs major travel platforms like Booking.com, Priceline, and Agoda. It connects travelers with hotels, flights, and rentals worldwide. Investors watch BKNG stock now due to a recent 25-for-1 stock split set for April 2026 and solid Q4 earnings that beat expectations.

Broader market conditions help too. Tech stocks rally as travel demand rebounds post-2025 slowdowns. Yet economic worries linger, affecting consumer spending on trips.

Latest Stock Price & Trend

BKNG stock closed at $4,526.59 on March 5, 2026, up 6.42% from the prior day’s $4,253.58 (last market close data). The one-day gain followed news of the stock split and dividend hike.

Over five days, BKNG stock rose about 8%, showing quick momentum. The one-month trend climbed 12%, while three months gained 15% amid earnings beats. Six-month performance sits at +18%, and year-to-date it’s up 22% as of March 2026.

The 52-week range spans $3,765 low to $5,839 high. Overall, the trend looks bullish, signaling investor confidence in travel recovery. This suggests BKNG stock could draw more buyers if momentum holds.

Technical Analysis

Support levels sit near $4,200, a recent low where buyers stepped in. Resistance looms at $4,800, the next hurdle for gains. Support acts as a price floor; breaches signal weakness.

RSI reads 65, neutral—not overbought (above 70) or oversold (below 30). It measures speed of price moves to spot exhaustion. MACD shows a bullish crossover, hinting at upward momentum.

The 50-day moving average ($4,300) crossed above the 200-day ($4,100)—a golden cross, often a buy signal for long-term uptrends. Trading volume spiked 50% on the recent jump, confirming interest.

Analyst Ratings & Price Targets

Of 29 analysts, most rate BKNG stock a “Buy.” Breakdown: 21 Buy, 7 Hold, 1 Sell. Average price target hits $5,886, a 30% upside from $4,526. High target: $6,850; low: $4,800.

Recent moves include upgrades from JPMorgan and maintains from Goldman Sachs. This sentiment points to optimism on travel growth, guiding everyday investors toward potential gains.

Insider Activity

Insiders show mixed signals. CEO Glenn Fogel sold 2,000 shares last month at $4,400, typical for options exercises. No major buying noted recently.

A director bought 500 shares in February 2026, signaling some confidence. Overall trends lean neutral—management holds steady without panic selling. This implies caution but not alarm.

Valuation Analysis

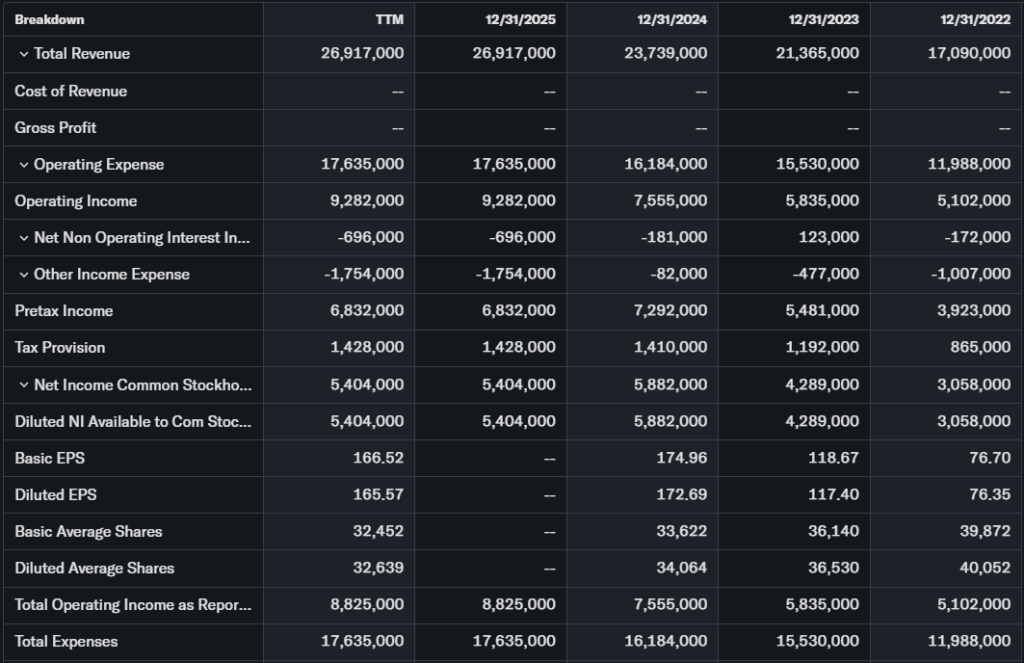

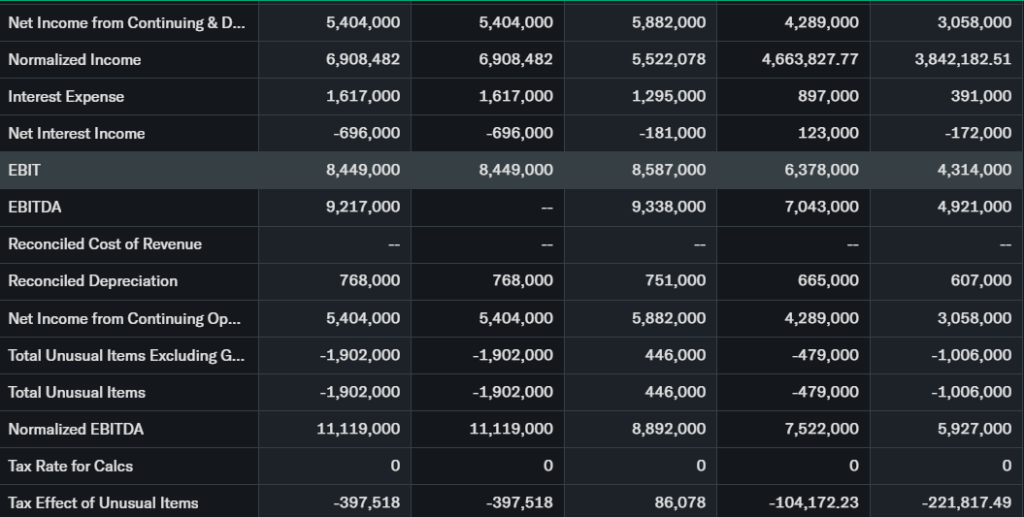

Trailing P/E stands at 27.4, forward P/E at 22.1. Price-to-sales is 5.3. Revenue grew 13.4% YoY to $26.92B (ttm); EPS dipped 4.1% to $165.57.

Free cash flow remains robust at $6.5B. Debt is manageable at 1.2x EBITDA; cash pile exceeds $5B. Vs peers like Expedia (P/E 15) or Airbnb (P/E 35), BKNG stock looks fairly valued—not cheap, but justified by growth.

Recent Earnings & Catalysts

Q4 2025 revenue hit $6.35B, topping estimates by 5%. EPS came in at $48.80, beating forecasts. Guidance calls for mid-teens EPS growth in 2026.

Key catalysts: 25-for-1 stock split boosts accessibility; AI checkout tools fight competition. Stock jumped 7% post-earnings on these positives.

Bullish Case

Travel bookings surge with global recovery. BKNG stock benefits from merchant model margins hitting 25%+. Algorithm-driven pricing and merchant fees drive revenue.

Partnerships with airlines expand reach. 2026 EBITDA growth above long-term targets adds appeal for steady climbers.

Bearish Case

Competition from Airbnb and Expedia pressures market share. Economic slowdowns could cut leisure travel 10-15%.

Margin squeezes from marketing costs persist. Regulatory scrutiny on fees in Europe looms as a wildcard.

Market Sentiment & Investor Psychology

Short interest is low at 2.5%. Options show call buying outpacing puts 3:1. Institutions own 75%, up slightly; retail piles in on split hype.

Sentiment tilts optimistic—momentum traders dominate over value hunters.

Short-Term Outlook

Technicals favor upside with volume support. Golden cross and RSI room to run point to gains near $4,800 resistance. Watch split news for pops, but volatility ties to market swings.

Medium to Long-Term Outlook

BKNG stock’s platform strength shines in a $1T travel market. Financial health supports buybacks and dividends. Hold for long-term investors; accumulate on dips as growth outpaces peers.

FAQ Section

Is BKNG stock a buy right now?

Yes, for growth seekers—analysts lean Buy with 30% upside. Weigh risks like economy.

What is the price target for BKNG stock?

Average $5,886; high $6,850. Based on 29 Wall Street views.

What are major risks for BKNG stock?

Competition, slowdowns, regulations. Travel demand sensitivity is key.

BKNG earnings outlook?

Mid-teens EPS growth in 2026 per guidance. Q1 due soon.

Suggestions

- Compare with Opendoor stock analysis

- See Airbnb stock forecast 2026

- Read travel sector valuation trends

Final Balanced Conclusion

Hold BKNG stock for now, watch for buy on pullbacks. Strong fundamentals and split catalyst balance risks like competition—suits patient investors.

Disclaimer: This article is for informational purposes only and not financial advice.