Beyond Meat (BYND) stock analysis covering price trend, earnings, valuation, forecast, and whether BYND stock is a buy for 2026 and beyond.

Introduction

Beyond Meat (ticker: BYND) is a plant-based meat company that sells burger patties, sausages, and other meat alternatives to retailers and restaurants worldwide. Investors are watching Beyond Meat stock closely because the company has gone from a high-growth favorite to a deeply challenged turnaround story, with sharp swings driven by earnings, debt restructuring, and meme-style trading. The broader equity market has been volatile as interest rates remain elevated and investors rotate between growth and value, which tends to magnify moves in speculative names like Beyond Meat stock. In this environment, clear analysis of Beyond Meat stock price, fundamentals, and forecast is critical for everyday investors.

Latest Stock Price & Trend

Recent data show BYND stock trading in the low single digits after a period of extreme volatility, including multi-day moves of several hundred percent during 2025 meme-driven spikes. One notable episode saw Beyond Meat stock price jump roughly 600% in three days, with a 3‑day gain from around 0.50–0.60 dollars to above 3.60 dollars, fueled by heavy retail trading and short covering rather than fundamental news. Over a 5‑day and 1‑month view, the stock has often shown sharp spikes followed by equally steep pullbacks, leaving a choppy, high‑beta pattern rather than a steady uptrend. Over the past 3–6 months and year‑to‑date, BYND stock remains down heavily from prior years, even after short squeezes, and has traded in a 52‑week range that has stretched from well under 1 dollar up to almost 9 dollars at the highs.

This pattern suggests that the overall trend in Beyond Meat stock is still bearish, with occasional explosive rallies driven by sentiment and positioning instead of sustained improvements in earnings. For investors, that means the risk of large drawdowns remains high, and short‑term price action in BYND stock price may say more about momentum and liquidity than about long‑term value.

Technical Analysis

In technical analysis, support is a price zone where buyers tend to step in, while resistance is an area where selling pressure often appears and rallies stall. For Beyond Meat stock, recent trading suggests short‑term support has formed near the sub‑1 to low‑single‑digit region where meme spikes began, while resistance has emerged around prior squeeze highs in the mid‑single‑digits to high‑single‑digits range. These support and resistance bands matter because breaks below support can trigger fresh sell‑offs, while moves above resistance can fuel short squeezes as traders rush to cover.

The Relative Strength Index (RSI) measures whether a stock is overbought (typically above 70) or oversold (below 30) based on recent price changes. During BYND’s violent rallies, the RSI has periodically pushed into overbought territory, signaling stretched upside momentum that often precedes sharp reversals, while during long declines it has approached oversold levels. The Moving Average Convergence Divergence (MACD) indicator tracks the relationship between short‑ and long‑term moving averages; for Beyond Meat stock, MACD has tended to flip between bullish and bearish quickly, reflecting its boom‑and‑bust trading swings rather than a stable trend.

The 50‑day and 200‑day moving averages are key guides for many traders: when the 50‑day crosses above the 200‑day, it is called a “golden cross” (often seen as bullish), and when it drops below, it forms a “death cross” (seen as bearish). Given BYND’s prolonged decline and relatively low price compared to past highs, the longer‑term technical picture has largely resembled a death‑cross type setup, even though short squeezes can temporarily push the 50‑day average higher. Trading volume has periodically exploded to many times average—one session reportedly saw over 700 million shares trade—highlighting how quickly sentiment can swing. For beginners, the key takeaway is that Beyond Meat technical analysis points to a highly speculative, momentum‑driven stock where risk management is crucial.

Analyst Ratings & Price Targets

Wall Street analysts remain skeptical about Beyond Meat’s long‑term earnings power and balance sheet strength. Recent consensus data compiled by brokers and platforms show that the majority of analysts rate BYND stock as Sell, with only a small minority at Hold and very few or no active Buy ratings. Average price targets compiled for Beyond Meat stock forecast are modestly above the current depressed trading levels but far below past highs, with some sources citing an average Around‑mid‑single‑digit target and a wide spread between low and high estimates. For instance, one forecast service pointed to a 2026 price prediction above the current market price, but this estimate still reflects heavy uncertainty around revenue trends and profitability.

Some analysts have downgraded Beyond Meat stock over the past two years as sales slowed, cash burn persisted, and dilution increased, while others have maintained Neutral ratings but cut targets. A few more optimistic notes highlight the potential for margin recovery and product innovation if management executes on cost cuts and new product launches. Overall, analyst sentiment suggests investors should treat Beyond Meat stock as a high‑risk turnaround, not a stable growth story, and that any BYND stock price recovery depends heavily on delivering better earnings over the next several years.

Insider Activity

Insider activity—purchases and sales by executives, directors, and large shareholders—can offer clues about management’s confidence. Recent coverage of Beyond Meat has focused more on debt restructuring and equity issuance than on large insider buying, suggesting insiders have not been aggressively accumulating shares in the open market at current prices. At the same time, the company has converted nearly 1 billion dollars of convertible debt into equity, which, while not traditional insider selling, has diluted existing shareholders and shifted ownership dynamics.

In previous years, stock‑based compensation and secondary offerings meaningfully increased the share count, which acts similarly to continual insider and institutional monetization. The trend of limited insider buying combined with ongoing dilution signals caution rather than strong internal conviction in rapid share price recovery. For investors, the lack of clear, sustained insider accumulation is one more reason to treat Beyond Meat stock as speculative until the fundamental picture improves.

Valuation Analysis

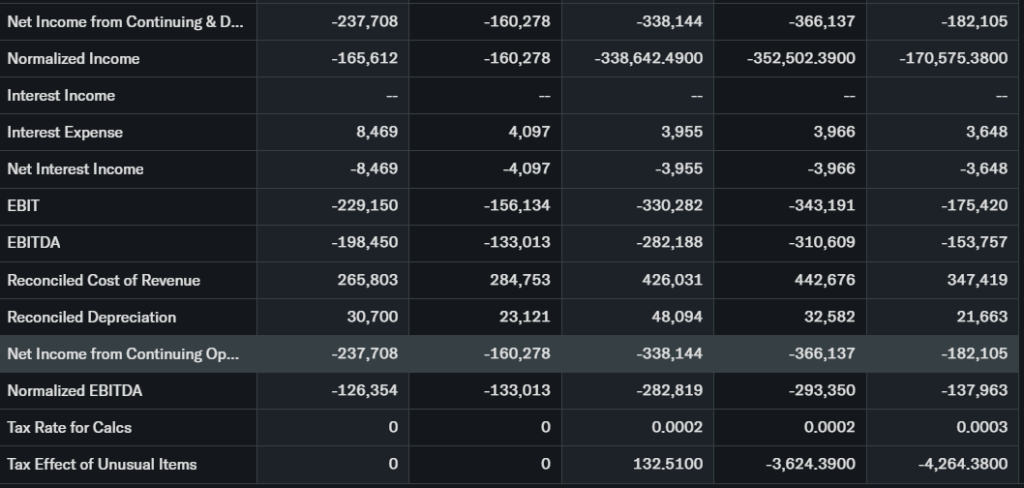

Traditional valuation metrics such as the price‑to‑earnings (P/E) ratio are difficult to use for Beyond Meat because the company remains unprofitable, generating negative earnings per share. Recent trailing data show annual revenues in the roughly 280–290 million dollar range, with net losses exceeding 230 million dollars and net profit margins around minus 80%. In this context, investors often look to price‑to‑sales (P/S); based on recent market caps cited during 2025 and 2026, Beyond Meat has at times traded near 6 times sales and at other points substantially lower after large price declines.

Cash flow has been negative, with continued cash burn and limited free cash flow, forcing the company to rely on debt and equity markets to fund operations. One analysis noted that total debt was around 1.1–1.2 billion dollars in recent years, while cash and equivalents sat near 100–120 million dollars, leaving a highly leveraged balance sheet despite some debt conversion. Compared with profitable large‑cap names like Microsoft or stable enterprise software companies, Beyond Meat’s valuation is stretched relative to its weak earnings profile, while even against other challenged consumer brands, its combination of high leverage and shrinking revenues stands out. On balance, the stock appears more speculative than fundamentally cheap, and many observers argue that BYND stock is not clearly undervalued despite its big drop from early highs.

Recent Earnings & Catalysts

Recent quarterly results from Beyond Meat show declining revenue and continued losses, even as management focuses on cost reductions and efficiency. For example, commentary on 2025 results indicates that revenue for the first nine months of 2025 fell around 14% year over year, while gross margin compressed to the mid‑single‑digits, reflecting weak demand and operational pressures. Full‑year expectations around that period called for a mid‑teens percentage revenue decline and a net loss above 200 million dollars, underscoring the depth of the challenge. Some forecasts note that Beyond Meat aims to lift gross margin toward 20% and achieve a positive EBITDA run rate by the second half of 2026, but this remains a target, not a current reality.

Key catalysts have included large retail distribution wins, such as expanded placement at big‑box chains, as well as international exits and product rationalizations. The stock has also reacted violently to debt restructuring announcements that reduced bankruptcy risk but caused heavy dilution, plus any news tied to plant‑based meat demand trends. Earnings reports often trigger substantial moves in Beyond Meat stock price, as investors attempt to gauge whether the turnaround is on track or further delays are likely.

Bullish Case

The bullish case for Beyond Meat stock centers on a few key points. First, management is actively cutting costs, optimizing manufacturing, and focusing on higher‑margin products, which could gradually lift gross margin toward its 20% target if execution improves and input costs moderate. Second, the global plant‑based meat market still has long‑term growth potential, especially as consumers look for healthier and more sustainable alternatives to animal protein, giving Beyond Meat a chance to stabilize or grow sales if it can better match taste, price, and nutrition expectations.

Third, recent debt conversions have reduced near‑term bankruptcy risk and simplified the capital structure, giving the company some breathing room to pursue its turnaround plan. New partnerships, reformulated products with cleaner labels, and strategic marketing initiatives could also provide upside surprises if they resonate with consumers and food‑service partners. For aggressive investors, these factors support a speculative BYND stock forecast where successful execution could lead to outsized returns from depressed levels.

Bearish Case

The bearish case remains substantial. Beyond Meat’s revenue has been shrinking as consumer demand for plant‑based meat has softened in key markets and competition from cheaper traditional meat and private‑label alternatives has intensified. Profitability remains far out of reach, with net profit margins deeply negative and ongoing cash burn that erodes the balance sheet. High leverage and the need for repeated capital raises have led to heavy shareholder dilution, which spreads future upside across a larger share base.

Additionally, the brand faces perception challenges around taste, price, and health, while regulatory or labeling debates around plant‑based products add further complexity. If gross margin improvements fall short, or if the category’s growth stagnates, the company may struggle to justify even its reduced valuation. In that scenario, BYND stock could continue to experience painful volatility and potential downside, especially if broader risk sentiment worsens.

Market Sentiment & Investor Psychology

Market sentiment around Beyond Meat stock is highly polarized. On one side, high short interest—reported in some periods as exceeding half of the free float—has created a fertile environment for short squeezes and meme‑style rallies. On the other side, many institutional investors have either reduced exposure or avoided the name due to its weak fundamentals and dilution risk, leaving a base dominated by traders and speculative retail investors.

Options markets have frequently seen elevated call volume during squeeze episodes, as traders bet on rapid upside moves, while put activity has been used by skeptics hedging or speculating on declines. Overall, sentiment appears cautiously negative among fundamental investors but opportunistic among momentum traders, resulting in a mix of fear and greed. For most long‑term investors, Beyond Meat stock sentiment can be described as neutral to cautious, with optimism limited to high‑risk turnaround and trading strategies.

Short-Term Outlook

Over the next few days and weeks, Beyond Meat stock is likely to remain driven by technical factors and news flow rather than a sudden fundamental transformation. Elevated volatility, high historical short interest, and a history of sharp moves around headlines or social‑media chatter suggest that short‑term traders should be prepared for wide intraday swings. If the stock trades near recent support zones with declining volume, sideways consolidation is possible; a fresh catalyst or renewed meme attention could instead spark another squeeze toward resistance levels.

Because indicators like RSI and MACD can flip quickly in such a name, short‑term forecasts for BYND stock price should be treated with caution and viewed as probability ranges rather than precise predictions. Conservative investors may prefer to avoid near‑term trading in Beyond Meat stock unless they have clear risk limits and position sizes tailored to the high volatility.

Medium to Long-Term Outlook

Over the next 6–24 months, Beyond Meat’s prospects will depend mainly on its ability to stabilize revenue, restore gross margins, and manage cash burn. Management targets of achieving at least 20% gross margin and a positive EBITDA run rate by the second half of 2026 are ambitious but not impossible if cost cuts, pricing, and product mix all improve. However, consensus expectations still call for flat to slightly declining revenues into 2027 and ongoing net losses, which means that the turnaround case remains unproven.

The broader plant‑based meat industry could return to moderate growth, but competition will stay intense, and Beyond Meat’s brand and distribution advantages must translate into consistent market share and better unit economics. Given the leverage, dilution, and uncertain demand, many long‑term investors may view the stock as a “watch” rather than a core holding, waiting for clearer evidence of sustainable profitability. For those with high risk tolerance, a small, speculative position in Beyond Meat stock might make sense as a potential turnaround play, but only with a long horizon and acceptance of possible capital loss.

FAQ Section

Is Beyond Meat (BYND) stock a buy right now?

Beyond Meat stock is currently a high‑risk speculative turnaround with declining revenues, persistent losses, and heavy dilution. Most analysts rate it as Sell or Hold, so many conservative investors may prefer to wait for clearer signs of margin and cash‑flow improvement before considering BYND stock a buy.

What is the price target for Beyond Meat stock?

Recent consensus estimates show an average Beyond Meat stock price target modestly above current levels but far below historical highs, with a wide gap between high and low forecasts. These targets reflect uncertainty about whether management can hit its 2026 profitability goals and stabilize revenue.

What are the major risks for Beyond Meat stock?

Key risks include shrinking revenue, intense competition from traditional meat and other plant‑based brands, negative margins, and ongoing cash burn. High leverage and repeated dilution also threaten existing shareholders if performance does not improve quickly.

What is the long-term outlook for Beyond Meat stock?

The long‑term outlook depends on whether Beyond Meat can turn its brand recognition and distribution into sustainable profits. If gross margins recover and revenue stabilizes, the stock could recover from depressed levels, but failure to deliver could lead to further downside and potential restructuring risk.

Suggestions

You could internally link this article to pieces such as:

- “Compare with Opendoor stock”.

- “See our Microsoft stock forecast” for readers seeking steadier large‑cap tech exposure.

- “Read our tech sector valuation breakdown” for a broader view on how speculative growth valuations compare with profitable leaders.

These links help readers place Beyond Meat stock in context within their overall portfolio decisions.

Final Balanced Conclusion

Beyond Meat (BYND) stock sits at the intersection of a challenged business model, a volatile investor base, and a still‑developing plant‑based meat industry. Fundamentals—declining revenue, weak margins, and dilution—argue for caution, while occasional meme‑style rallies and ambitious management targets keep the speculative upside narrative alive. For most long‑term, risk‑aware investors, a Watchlist/Hold stance appears more reasonable than an outright aggressive Buy, with any position sized conservatively and based on personal risk tolerance.

Disclaimer: This article is for informational purposes only and not financial advice.