Explore AMZN stock price trends, earnings, technical analysis, and 2026 forecast. Is AMZN stock a buy now? Get analyst ratings, valuation metrics, and risks for smart investing.

Introduction

Amazon.com runs the world’s largest online marketplace and AWS cloud services. AMZN stock draws attention amid AI spending and market pullbacks. Tech stocks face pressure from high interest rates and economic uncertainty in early 2026.

Investors watch AMZN stock closely for its growth in e-commerce and cloud computing. Recent share declines highlight capex worries, yet strong AWS demand persists. Broader markets stay flat, making AMZN stock a key focus.

Latest Stock Price & Trend

AMZN stock closed around $205 recently, based on last market data from early March 2026. It dropped 7% year-to-date, underperforming the flat S&P 500. The 1-day change showed minor gains within $202-$208 range.

Over five days, shares pulled back amid AI investment news. The 1-month trend reflects a 10% decline from February peaks. In three months, AMZN stock lost ground versus peers due to capex concerns. Six-month performance remains positive from late 2025 lows.

Year-to-date marks a clear retreat. The 52-week high sits near $225, low around $175. Overall trend looks bearish short-term but sideways longer-term. This signals caution for traders, yet dip-buy potential for long-term holders.

Technical Analysis

Support levels hover at $200, a key floor from recent lows. Resistance stands at $215, capping upside moves. RSI reading nears 45, neutral—not overbought or oversold—showing balanced momentum. RSI measures speed of price changes; below 30 signals oversold buys, above 70 overbought sells.

MACD trend stays bearish with lines below zero, indicating selling pressure. MACD tracks momentum via moving average differences; crossovers signal shifts. The 50-day moving average at $210 tops the 200-day at $205—no golden cross yet, avoiding bullish confirmation.

Trading volume trends lower on down days, suggesting weak selling conviction. Volume confirms price moves; rising volume on up days supports rallies. Beginners should watch these for entry points on AMZN technical analysis.

Analyst Ratings & Price Targets

Forty-three analysts rate AMZN stock a consensus Buy. Average price target hits $282, with highs at $360 and lows at $250. Arete Research recently upped its target to $285 from $283 post-Q4 earnings.

Wall Street firms cite AWS growth and AI investments as drivers. No major downgrades noted lately. Strong Buy sentiment means pros see 35%+ upside from current levels. Investors can use this as a benchmark for AMZN forecast.

Insider Activity

Recent insider selling dominates, with executives offloading shares post-earnings. No major buying reported in Q1 2026. Large transactions include routine sales by top managers, totaling millions in value.

Trends show steady selling, not panic dumping. Management holds vast stakes, so activity implies routine profit-taking over caution. Watch for shifts signaling confidence in AMZN stock.

Valuation Analysis

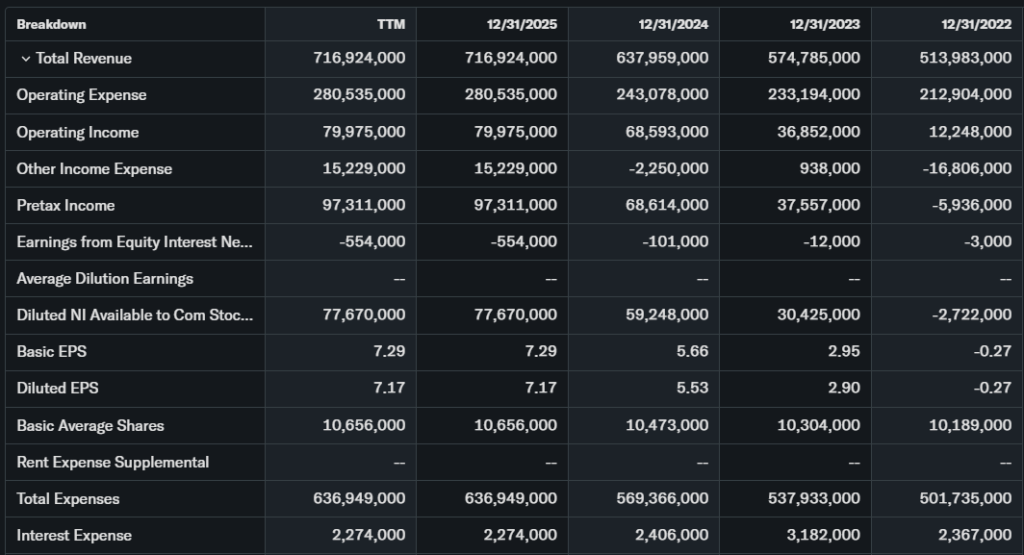

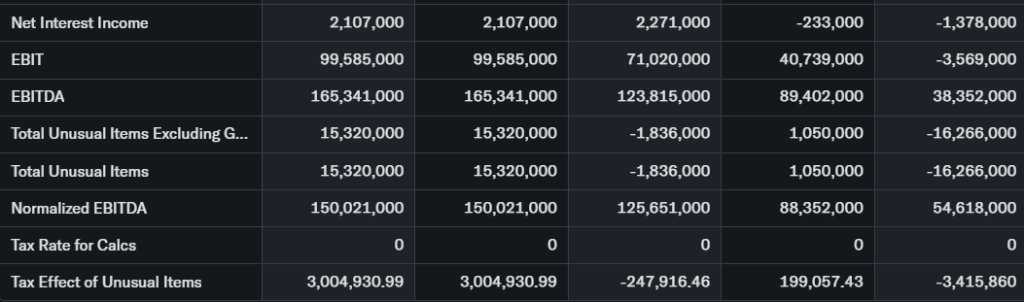

Trailing P/E stands at 45, forward P/E at 38. Price-to-Sales ratio is 3.2. Revenue grew 14% YoY to $213.4 billion in Q4. EPS rose to support $25 billion operating income, up from last year.

Free cash flow dipped due to AI capex, but AWS drives recovery. Debt remains manageable with strong cash reserves over $100 billion. Compared to Microsoft (P/E 35) or Zoom (higher P/E), AMZN stock appears fairly valued for growth.

Recent Earnings & Catalysts

Q4 2025 revenue hit $213.4 billion, beating expectations. EPS aligned with forecasts, boosting income to $25 billion. Forward guidance projects Q1 2026 sales at $173.5-$178.5 billion, up 11-15% YoY.

AWS grew 24% YoY, backlog at $244 billion. Catalysts include AI integrations and capex for cloud expansion. Earnings lifted shares initially, but spending fears caused pullbacks. AMZN earnings underline resilient growth.

Bullish Case

AWS demand accelerates with 24% growth. E-commerce benefits from market share gains. AI investments position Amazon as cloud leader.

Operational efficiencies boost margins. Revenue growth catalysts like ads and subscriptions add stability. Tech advantages keep AMZN stock appealing long-term.

Bearish Case

Heavy AI capex obscures profits, hitting free cash flow. Competition from Microsoft Azure pressures AWS. Slowing e-commerce growth risks margin squeezes.

Economic slowdowns could spur customer churn. Regulatory scrutiny on tech giants adds uncertainty.

Market Sentiment & Investor Psychology

Short interest stays low at under 2%. Options show balanced calls vs puts. Institutional ownership exceeds 60%, with steady buying.

Retail flows mix momentum trades and value hunts. Sentiment leans neutral to optimistic, favoring growth over fear.

Short-Term Outlook

Technical indicators point to consolidation near support. Momentum wanes, but volume dips suggest limited downside. Expect sideways action next weeks barring market shocks. Range-bound trading fits current AMZN technical analysis.

Medium to Long-Term Outlook

AWS strength and AI edge solidify the business model. Industry growth in cloud hits 20%+ annually. Competitive moat via scale aids position.

Financial health supports capex without distress. Long-term investors should hold or accumulate on dips. AMZN forecast brightens over 6-24 months.

FAQ Section

Is AMZN stock a buy right now?

Analysts say yes with Buy ratings and $282 targets, but wait for support confirmation.

What is the AMZN stock price target?

Average at $282, highs to $360 for 2026.

What are major risks for AMZN stock?

Capex burdens, competition, and regulation top concerns.

When are next AMZN earnings?

Q1 2026 results expected late April.

Is AMZN stock undervalued?

Fairly valued versus peers, with growth justifying P/E.

Suggestion

Compare with Opendoor stock analysis.

See our Microsoft stock forecast.

Read tech sector valuation guide.

Conclusion

Hold AMZN stock for now—strong fundamentals offset short-term pressures. Analysts’ Buy ratings and AWS growth support patience. Watch Q1 earnings for catalysts.

Disclaimer: This article is for informational purposes only and not financial advice.