AAL stock analysis: Latest price trends, earnings, technicals, and 2026 forecast. Is AAL stock a buy? Explore valuation, risks, and outlook for American Airlines investors.

Introduction

American Airlines Group (AAL) flies passengers and cargo worldwide. It ranks as a top U.S. carrier with a large fleet and global routes.

Investors watch AAL stock now due to oil price swings and travel demand shifts. Broader market volatility from Middle East tensions hits airline stocks hard.

Latest Stock Price & Trend

AAL stock closed at $11.11 on the last market session, based on March 10, 2026 data. It dropped 2.88% that day amid analyst cuts.

The 1-day performance showed a 1.89% gain earlier but reversed on high volume of 128.7 million shares, 108% above average. Five-day trend leaned bearish with premarket dips to $12.06 on March 3.

One-month trend fell about 27% as oil spikes weighed on airlines. Three-month decline hit similar levels, while six-month and year-to-date returns stayed negative at -18.33% YTD. The 52-week range spans $8.50 low to $16.50 high.

Overall trend looks bearish short-term but sideways longer-term. This signals caution for investors as macro headwinds persist.

Technical Analysis

Support levels sit near $10.34, the recent day’s low, where buyers may step in. Resistance looms at $12.52, Monday’s close on March 3.

RSI reading hovers near oversold territory, suggesting potential bounce if selling eases; RSI flags momentum extremes for entry points. MACD trend stays bearish, with lines below zero, indicating weak momentum—key for spotting reversals.

The 50-day moving average trails the 200-day, no golden cross (bullish signal) or death cross yet; these averages smooth price action to show trend strength. Trading volume surged 52-108% above norms, pointing to heightened interest or fear.

Analyst Ratings & Price Targets

Fifteen analysts rate AAL stock as Hold overall. Breakdown shows few Buys, more Holds, and some Sells. Average price target hits $15.28, with highs near $17.62 and lows at $14.

Recent cuts include one to $14 from higher levels on March 12. Wall Street firms cite debt and oil risks but note operational gains. This mixed sentiment means steady but not aggressive upside for investors.

Insider Activity

Recent insider selling dominates, with no major buys noted in filings. Large transactions reflect management trimming shares amid stock weakness.

Trends show caution, as executives sell during dips rather than buy dips. This implies limited confidence short-term but not outright panic.

Valuation Analysis

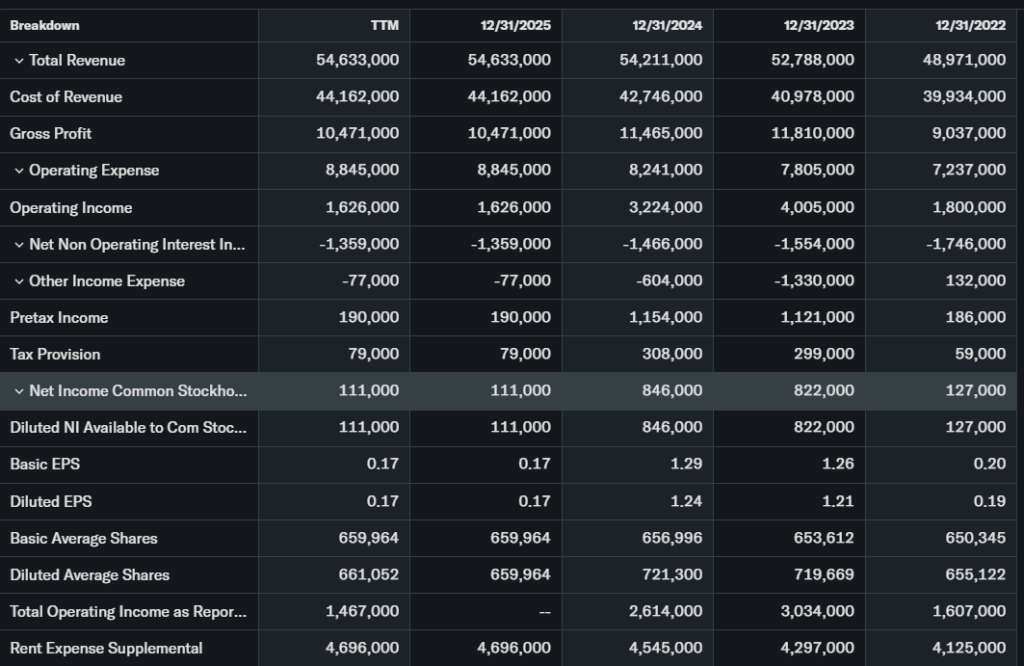

Trailing P/E stands high due to earnings pressure, while forward P/E looks reasonable at current levels. Price-to-sales ratio remains low versus peers like Delta.

Revenue growth slowed YoY amid capacity cuts; EPS dipped but free cash flow holds steady. Debt load hits $36.5 billion against modest cash, though deleveraging progresses.

Compared to United or Delta, AAL stock appears undervalued on price targets but risky on debt—fairly valued overall for patient investors.

Recent Earnings & Catalysts

Latest quarterly results missed on margins due to fuel costs, with revenue below expectations. EPS fell short, but guidance eyes Q2 2026 margin gains.

Key catalysts include premium seat push and reliability under CEO Isom. Earnings drop triggered the 27% three-month slide in AAL stock price.

Bullish Case

Strong U.S. travel demand fuels revenue growth for AAL stock. Premiumization strategy boosts yields versus rivals.

Operational fixes cut costs, closing gaps with Delta. Deleveraging builds long-term stability.

Bearish Case

Competition from low-cost carriers erodes margins. High $36.5B debt raises refinance risks in rising rates.

Oil spikes from geopolitics and labor issues add pressure. Slow growth could spur customer churn.

Market Sentiment & Investor Psychology

Short interest climbs, reflecting bearish bets. Options show more puts than calls amid volatility.

Institutional ownership holds steady; retail chases momentum dips. Sentiment leans neutral to fearful.

Short-Term Outlook

Technicals point to oversold RSI and volume spikes. Momentum stays weak with oil risks.

Expect sideways chop next weeks unless catalysts emerge—no quick rallies likely.

Medium to Long-Term Outlook

Solid business model and industry tailwinds favor growth. Competitive moat via network size helps.

Financial health improves with debt cuts; hold for long-term investors, watch for accumulation on dips. AAL forecast eyes $15+ in 2026.

FAQ

Is AAL stock a buy right now?

Hold for now; targets suggest upside but risks loom.

What is the AAL stock price target?

Average at $15.28, ranging $14-$17.62.

AAL stock forecast for 2026?

Recovery to $15+ if debt eases and travel holds.

Major risks for AAL stock?

Debt, oil prices, competition.

AAL earnings outlook?

Q2 2026 key for margins; expect modest growth.

Suggestion

Compare with Opendoor stock analysis.

See United Airlines stock forecast.

Read airline sector valuation trends.

Conclusion

Hold AAL stock. Balanced risks and recovery signs justify watching over buying now.

AAL technical analysis shows oversold potential, but AAL valuation needs debt progress. Is AAL stock a buy? For long-term, yes on dips.

Disclaimer: This article is for informational purposes only and not financial advice.