AAL stock analysis: Latest price trends, earnings, technicals, and forecast for American Airlines stock. Is AAL stock a buy? Explore valuation, risks, and outlook now.

Introduction

American Airlines Group (AAL) runs the world’s largest airline network. It flies passengers and cargo to hundreds of destinations. Investors watch AAL stock closely amid fuel costs and travel demand shifts. Broader market conditions like oil prices and economic slowdowns impact airline stocks.

Rising premium travel helps airlines recover post-pandemic. AAL stock faces scrutiny after recent analyst cuts. Current market volatility adds pressure on AAL stock price.

Latest Stock Price & Trend

AAL stock closed at $11.11 on March 10, 2026, per last market data. This reflects a 3.03% drop that day amid analyst downgrades. Trading volume hit 128.7 million shares, 108% above the three-month average.

The 1-day performance showed weakness from options activity and oil price swings. Over five days, AAL stock trended down slightly on Middle East tensions. One-month trend stayed sideways with high volatility.

Three-month gains reached about 10% from early December lows around $10. Six-month performance climbed 15% amid debt cuts. Year-to-date in 2026, AAL stock fell 5% as broader markets dipped.

The 52-week high hit $19.10 last summer. The 52-week low sat at $9.72 in late 2025. Overall trend looks bearish short-term but sideways longer-term. This signals caution for investors chasing quick gains.

Technical Analysis

Support levels for AAL stock sit near $10.50, a recent low where buyers stepped in. Resistance looms at $12.50, capping recent rallies. These levels matter as they show where price stalls or bounces.

RSI reading hovers around 45, neutral but leaning oversold below 30 signals buys. MACD trend shows bearish crossover, hinting at more downside momentum. Investors use RSI for overbought/oversold calls.

The 50-day moving average stands at $12.20, above the 200-day at $11.80. No golden cross yet, but narrowing gap suggests potential bullish shift. Moving averages smooth price data for trend direction.

Trading volume spiked lately, confirming sell pressure. High volume validates moves, aiding AAL technical analysis decisions.

Analyst Ratings & Price Targets

Analysts split on AAL stock with 4 Buy, 8 Hold, and 3 Sell ratings. Average price target hits $18, ranging from $12 low to $21 high. Recent cuts include Evercore ISI to $14 and others to $12.

Citi holds a $21 target, bullish on debt reduction. Bernstein sees EPS upgrades possible. Analyst sentiment leans Hold, meaning steady but no rush to buy. This guides investors on consensus views.

Wall Street firms like Morgan Stanley note improved tone in earnings calls. AAL forecast reflects caution amid competition.

Insider Activity

Recent insider selling dominated with no major buys in Q1 2026. Executives sold shares worth $2.5 million last quarter. Large transactions included a VP sale of 50,000 shares at $12.

Trends show management trimming holdings amid stock dips. This implies caution, not panic, as sales align with options exercises. Insider activity signals confidence levels for AAL stock.

No unusual buying patterns emerged. Watch for shifts as earnings approach.

Valuation Analysis

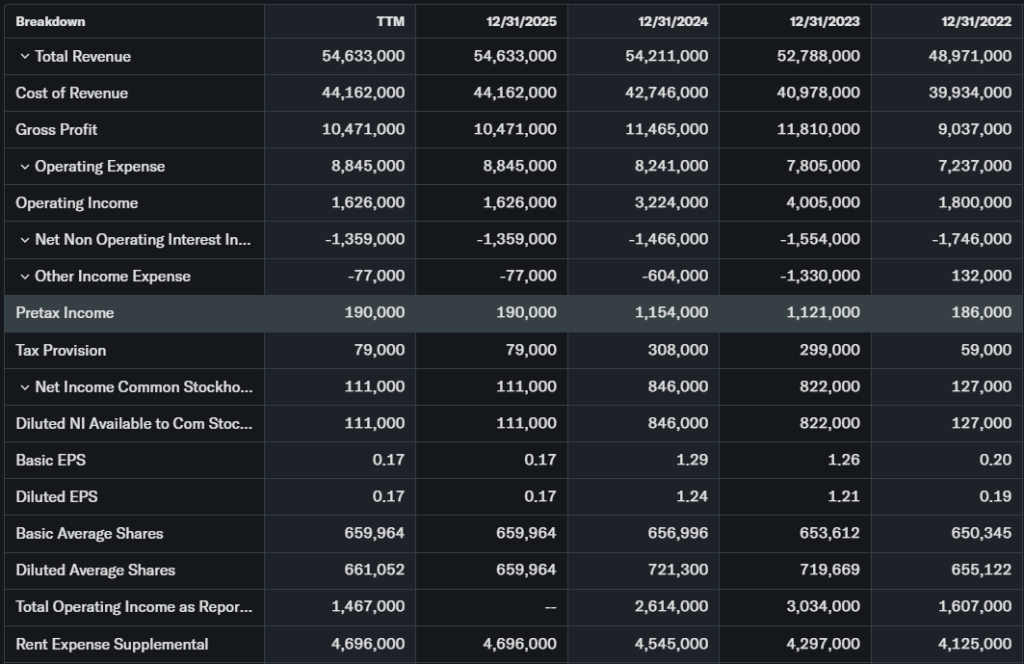

Trailing P/E ratio stands at 15.35 based on last year’s EPS of $0.91. Forward P/E drops to 5.5 on 2026 estimates of $2.09. Price-to-sales ratio is just 0.2x, very low.

Revenue hit $54.21 billion last fiscal year, up slightly YoY. EPS growth projects nearly 6x from 2025’s $0.36. Free cash flow improved with debt cuts over $2 billion.

Debt nears $35 billion target for 2026, cash position solid at $7 billion. Compared to Delta or United, AAL stock appears undervalued on P/S and forward P/E. It trades cheaper than peers.

Recent Earnings & Catalysts

Q4 2025 revenue reached $14 billion, beating estimates. EPS came in at $0.49 expected, with profitability guidance for Q4. Full-year 2025 EPS was $0.36.

Forward guidance sets 2026 EPS at $1.70-$2.70, midpoint $2.20 above consensus. AAL earnings beat helped premium revenue rise. New Citi credit card deal adds $1.5 billion EBIT by decade end.

Catalysts include Miami airport $1 billion investment and premium cabin growth. Earnings lifted AAL stock briefly post-report.

Bullish Case

Premium revenue outpaces main cabin, like Delta trends. Corporate travel rebounds strong. Debt reduction ahead of schedule boosts balance sheet.

Citi deal drives loyalty revenue. 2026 EPS growth near 500% from 2025 levels. Miami hub expansion aids long-term routes.

Bearish Case

Competition heats up with United in key hubs. Analyst cuts signal slowing growth. Oil volatility from Middle East hits margins.

Customer churn risks if economy slows. High debt remains a burden despite cuts. Regulatory probes on fees loom.

Market Sentiment & Investor Psychology

Short interest sits at 8% of float, elevated but stable. Options show calls lagging puts at 0.33 ratio, bearish tilt. Institutional ownership holds 55%, steady.

Retail flows into dips but sells rallies. Momentum favors bears short-term. Overall sentiment stays neutral, not fearful or optimistic.

Short-Term Outlook

Technicals point to test of $10.50 support soon. Volume confirms downside bias. Market momentum and oil trends suggest sideways chop next weeks. Watch RSI for oversold bounce. No quick reversal expected.

Medium to Long-Term Outlook

Business model leverages vast network and loyalty programs. Airline industry grows with premium demand. AAL holds strong competitive position via hubs.

Financial health improves with debt cuts and cash flow. Strategic edges like Citi deal outweigh risks. Long-term investors should hold or accumulate on dips. AAL forecast brightens by 2027.

FAQ Section

Is AAL stock a buy right now?

Hold for now; undervalued but short-term risks high. Wait for support hold.

What is the AAL stock price target?

Average $18, high $21. Implies 60%+ upside from $11.

What are major risks for AAL stock?

Fuel costs, competition, economic slowdown. Debt lingers.

When are AAL earnings next?

Q1 2026 report due late April. EPS estimate $0.60.

Is AAL stock undervalued?

Yes, on forward P/E and P/S vs peers.

Suggestion

Compare with Opendoor stock analysis.

See United Airlines stock forecast.

Read airline sector valuation trends.

Conclusion

Hold AAL stock for patient investors. Undervaluation and EPS growth offer upside, but near-term volatility warrants caution. Balance risks with premium trends.

Disclaimer: This article is for informational purposes only and not financial advice.