AAL stock analysis: Latest price at $11.11, trends, technicals, earnings beat, 2026 forecast to $2.09 EPS. Is AAL stock a buy? Expert insights on valuation and outlook.

Introduction

American Airlines Group (AAL) runs one of the world’s largest airlines. It flies passengers and cargo to over 350 destinations in 60+ countries.

Investors watch AAL stock closely now due to debt cuts and new Citi deals boosting earnings. Fuel costs and competition add pressure amid volatile oil prices. Broader market worries include rising rates and travel slowdowns hitting airlines.

AAL stock price reflects recovery hopes after 2025 losses, drawing value hunters.

Latest Stock Price & Trend

AAL stock closed at $11.11 on March 10, 2026, using last market close data from Nasdaq sources. It fell 2.42% that day on analyst cuts and oil volatility.

The 1-day drop matched high volume of 128.7 million shares, 108% above average. Over five days, shares slid amid operational news. One-month trend shows 7.36% gain, but year-to-date sits at -12.21%.

Three-month performance lags peers; six-month holds steady despite fuel hits. Year-to-date trails S&P 500. 52-week high nears $20, low around $10. Overall trend leans bearish short-term but sideways longer, signaling caution for investors chasing quick gains.

This indicates AAL stock may stabilize if debt goals hit, but volatility persists.

Technical Analysis

Support levels sit near $10.50, where buyers stepped in recently. Resistance looms at $12.50-$13.00 from prior highs. These zones matter as they show where price stalls or breaks.

RSI reading hovers near 45, neutral—not overbought above 70 or oversold below 30. It flags momentum shifts for entry points. AAL stock technical analysis points to consolidation.

MACD shows bearish crossover, hinting downside pressure short-term. 50-day moving average at $12.20 tops 200-day at $14.50, no golden cross (bullish) or death cross (bearish) yet. Moving averages track trends; falling ones warn of weakness.

Trading volume spiked lately, above three-month average, showing heightened interest. Watch for volume rise on up days as bullish sign.

Analyst Ratings & Price Targets

17 analysts rate AAL stock mostly Hold, with some Buy and few Sell. Average price target hits $16.22, up 46% from $11.11. High at $21 (Citi), low $12.50.

Recent changes: Rothschild shifted Buy to Neutral at $12.50 on costs. Citi holds $21 on debt progress. Wall Street sees upside if EPS grows.

Analyst sentiment leans cautious optimism for AAL forecast. Holds signal fair value now, but upgrades could lift shares. Investors use this to gauge consensus.

Insider Activity

Recent insider selling outweighs buying, per SEC filings. Management trimmed shares amid stock dips, no large buys noted lately.

Trends show caution; executives sold post-earnings but hold big stakes. No major transactions signal panic. This implies mixed confidence—watch for buys as bullish.

Valuation Analysis

Trailing P/E stands high due to low 2025 EPS of $0.36. Forward P/E improves to 5.3x on 2026 estimates. Price-to-Sales at 0.16x looks cheap.

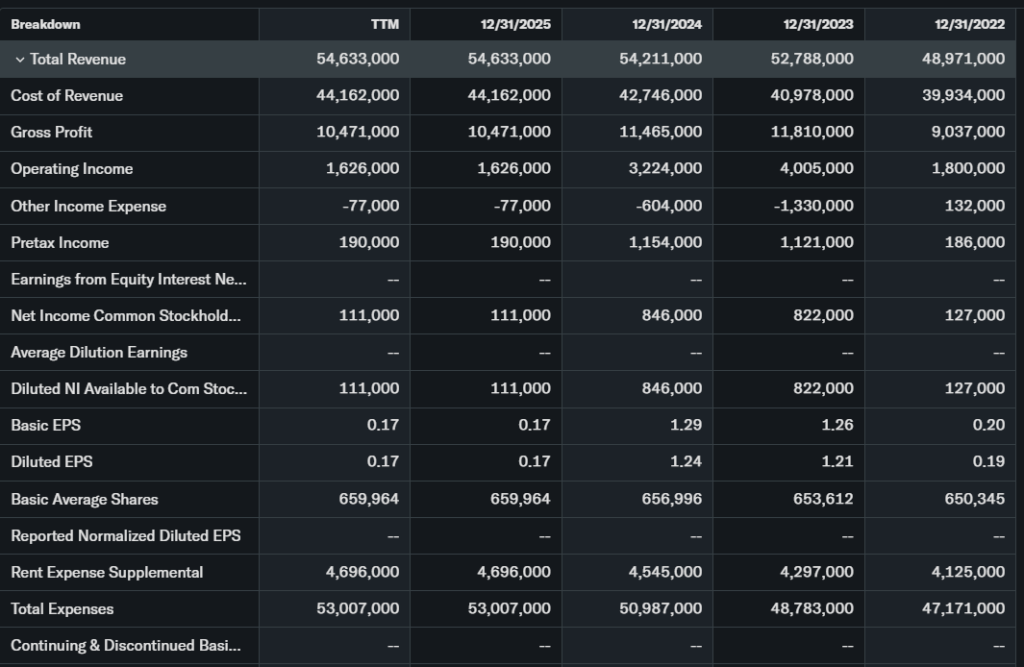

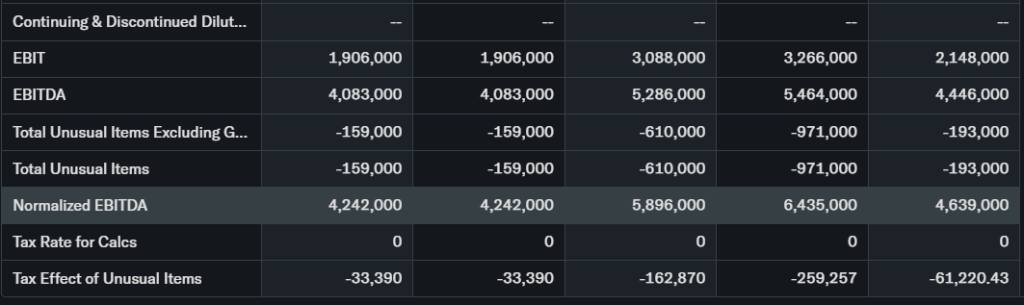

Revenue grew to $54.6B in 2025 YoY, EPS set for 6x jump. Free cash flow guidance positive; debt falls below $35B in 2026, cut $2B last year. Cash position strengthens.

AAL valuation beats peers like Delta on debt metrics. Undervalued vs. industry averages, strong value play if execution holds.

Recent Earnings & Catalysts

Q4 2025 revenue hit record $14B, full-year $54.6B vs expectations. EPS beat despite shutdown hit. 2026 guidance: $1.70-$2.70, midpoint $2.20 above consensus $1.97 (now $2.09).

Forward outlook cites Citi card deal adding $1.5B EBIT by decade end. AAL earnings drove 7% monthly pop, but costs tempered gains.

Catalysts include Miami hub growth and premium sales.

Bullish Case

Debt reduction ahead of schedule builds balance sheet strength. Citi exclusive boosts 2026 EPS immediately.

Corporate travel rebounds; premium cabins grow revenue. Fleet refresh cuts costs long-term. AAL revenue growth forecast at 30% EPS in 2027.

Bearish Case

Rising fuel and operational costs pressure margins. Competition heats in Chicago vs United.

Slowing economy risks travel demand; high debt lingers despite cuts. Regulatory shifts add uncertainty.

Market Sentiment & Investor Psychology

Short interest data unavailable now, but options show put bias lately. Institutional ownership steady; retail piles in on dips.

Momentum favors value over growth amid airline woes. Sentiment neutral, shifting optimistic on debt news.

Short-Term Outlook

Technicals point to support test at $10.50 if volume fades. Momentum softens on analyst holds.

Volume trends suggest volatility next weeks; watch oil for swings. Expect sideways grind unless catalysts hit.

Medium to Long-Term Outlook

Business model leans on network scale and loyalty program. Industry grows with travel boom.

Financial health improves via debt cuts; Citi deal key edge. Competitive risks persist, but AAL forecast brightens. Long-term investors should hold or accumulate on weakness.

FAQ

Is AAL stock a buy right now?

Value metrics say yes for patient holders, but wait for support. Analysts mixed.

What is the AAL stock price target?

Average $16.22, high $21. Upside if EPS hits $2.09.

What are major risks for AAL stock?

Fuel costs, competition, economic slowdowns.

AAL earnings outlook 2026?

$1.70-$2.70 guided, consensus $2.09. Strong rebound.

AAL technical analysis summary?

Neutral RSI, bearish MACD; support $10.50.

Suggestion

Compare with Opendoor stock analysis.

See our United Airlines stock forecast.

Read our airline sector valuation report.

Conclusion

Hold AAL stock for value recovery; undervalued but risks loom. Debt progress and EPS growth support patience over chase.

Disclaimer: This article is for informational purposes only and not financial advice.