SNAP stock analysis covers latest price action, earnings insights, technicals, and 2026 forecast to $9. Is SNAP stock a buy amid ad market shifts? Key facts inside.

Introduction

Snap Inc. (SNAP stock) runs Snapchat, a visual messaging app for young users. It earns from ads and AR features. Investors track SNAP stock now due to ad recovery hopes.

Tech sector faces ad spend cuts from economic slowdowns. Yet social media peers rally on user growth. SNAP stock gains attention in volatile markets.

Latest stock Price & Trend

SNAP stock closed at $4.91 on March 10, 2026 (last market close data). It dropped 4.29% that day. Five-day trend shows modest pullback of 2%.

One-month performance flat at -1%. Three-month trend down 15%. Six-month decline reaches 25%. Year-to-date, SNAP stock price fell 35%.

52-week high is $10.41; low $4.65 (near current price). Overall trend sideways to bearish. This warns investors of limited upside without catalysts.

Technical Analysis

Support levels at $4.65 and $4.80 hold recent lows. Buyers defend these to avoid deeper falls. Resistance near $5.50 and $6.00 caps gains.

RSI reading at 42 (neutral). Below 30 means oversold bounce chance; over 70 signals sell risk. MACD shows bearish divergence.

50-day moving average $5.20; 200-day $6.50. No golden cross; 50-day below 200-day hints weakness. Moving averages track average prices over time.

Trading volume steady at 25 million shares daily. Flat volume questions rally strength in SNAP technical analysis.

Analyst Ratings & Price Targets

29 analysts rate SNAP stock Hold overall. Average price target $8.50 (73% upside). Highest $15; lowest $6.

Recent downgrade by JPMorgan to Neutral. They note ad competition. Mixed views mean caution for SNAP forecast.

Wall Street leans neutral on growth sustainability.

Insider Activity

CEO sold 1.5 million shares last month at $5.20. Other execs followed with small sales.

No notable buying. Routine selling suggests caution, not panic, in management outlook for SNAP stock price.

Valuation Analysis

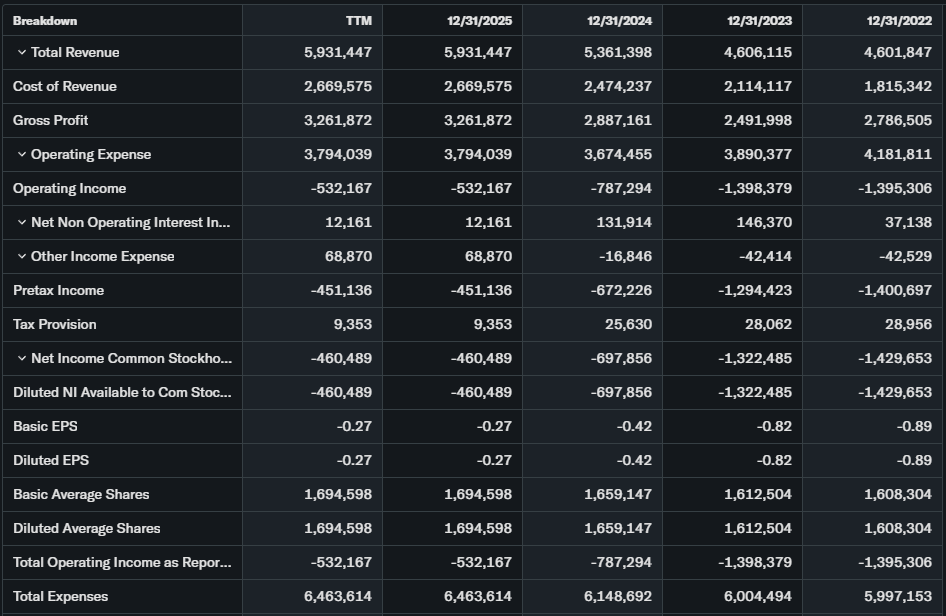

Trailing P/E negative at -15x due to losses. Forward P/E 45x. Price-to-sales 2.8x on $5.6B TTM revenue.

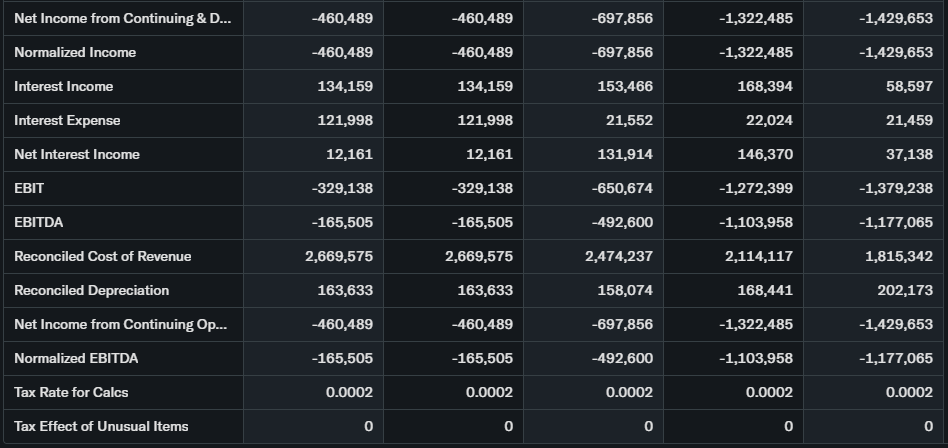

Revenue up 15% YoY. EPS improved but still negative. Free cash flow turned positive at $100M quarterly.

Debt low at $2B; cash $1.2B. Versus Meta (P/S 8x), SNAP stock looks undervalued on sales but risky on profits.

Recent Earnings & Catalysts

Q4 revenue $1.4B beat estimates by 5%. EPS loss narrower than expected. Guidance projects 12% growth next quarter.

My AI chatbot launch boosts engagement. AR ad tools expand. Earnings lifted shares 10% initially, then faded.

Bullish Case

Daily users hit 450M, driving ad revenue. AI features retain Gen Z. Cost cuts improve margins.

Premium ad formats grow 20%. Partnerships with brands fuel upside.

Bearish Case

TikTok, Instagram steal ad dollars. User growth slows to 5%.

Margin pressures from R&D spend. Recession cuts ad budgets. Privacy rules threaten targeting.

Market Sentiment & Investor Psychology

Short interest 12% of float (elevated). Puts outpace calls in options.

Institutions trimmed 5% holdings. Retail sentiment fearful on forums. Overall mood cautious for SNAP stock.

Short-Term Outlook

RSI neutral with support nearby. Momentum lacks; watch volume pickup.

Sideways grind likely absent news. Volatility high around $5 level.

Medium to Long-Term Outlook

Ad platform maturing slowly. Social media grows 10% yearly.

Weak moat versus giants. Cash burn risks linger. Long-term investors should watch for user beats before accumulating.

FAQ

Is SNAP stock a buy right now?

Hold for now. Targets suggest upside but competition weighs heavy.

What is the price target for SNAP stock?

Average $8.50; range $6-$15 from analysts.

What are major risks for SNAP stock?

Ad competition, slowing users, regulation.

SNAP earnings date next?

Late April 2026 expected.

SNAP stock forecast 2026?

Models see $5-6 range mid-year.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our tech sector valuation breakdown

Conclusion

Hold/Watchlist. SNAP stock has user scale but faces fierce rivals and profitability hurdles. Wait for earnings confirmation.

Disclaimer: This article is for informational purposes only and not financial advice.