Explore SMCI stock price, latest trends, earnings, technical analysis, and forecast. Is SMCI stock a buy? Get balanced insights for investors as of March 2026

Introduction

Super Micro Computer makes high-performance servers and storage for AI and cloud computing.

Investors watch SMCI stock closely due to AI demand and recent price swings.

Tech stocks face pressure from high valuations amid economic shifts in 2026.

Latest Stock Price & Trend

SMCI stock closed at $32.39 on February 27, 2026, up 0.34% that day.

Over five days, it fell 3.93% amid volatility, with gains on February 25 but drops before.

The one-month trend shows choppy action around $30-$34, down from early February peaks near $35.

In three months, shares declined sharply from $62 highs, reflecting a bearish shift.

Six-month performance weakened by over 30%, hit by sector corrections.

Year-to-date in 2026, SMCI stock rose 8.79% from $29.68, but lags broader tech.

The 52-week range spans $27.60 low to $62.36 high, with current price near lows.

This sideways-to-bearish trend signals caution for investors, pointing to consolidation before potential rebound.

Technical Analysis

Support levels sit at $29.29, a key floor from recent lows; a break below eyes $27.07.

Resistance looms at $33.79; surpassing it could spark upside.

RSI at 52-53 reads neutral, neither overbought above 70 nor oversold under 30.

MACD at 0.22 shows mild bullish momentum for short-term trades.

The 50-day moving average hovers near recent prices, while 200-day at $41.66 caps upside—no golden cross yet.

Volume spiked to 115 million on February 4 but averages 20-30 million lately, suggesting fading interest.

These indicators matter as they gauge momentum and potential reversals for entry points.

Analyst Ratings & Price Targets

Of 17-38 analysts, consensus leans Hold, with some Buys.

Average price target is $41-568, high $1350, low $100—implying upside from $32.

Recent upgrades include Argus to Buy despite weak results.

Goldman Sachs and others issued notes in 2024-2025.

This mixed sentiment means caution; targets reflect growth bets but valuation risks.

Insider Activity

Insider data shows limited recent buys; older sales like 2016 by execs dominate records.

No major buying trends signal confidence lately.

Management activity leans neutral to selling, implying caution amid volatility.

Valuation Analysis

Trailing P/E sits at 23-29, forward around 17-25 based on EPS growth.

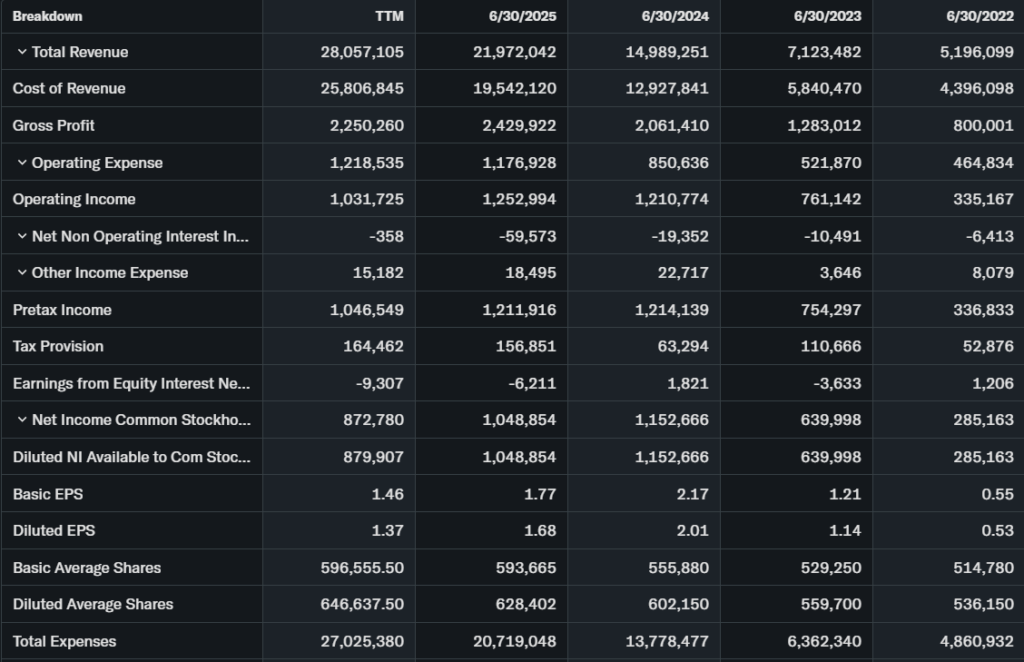

Price-to-sales reflects $28B TTM revenue, with 35% YoY growth.

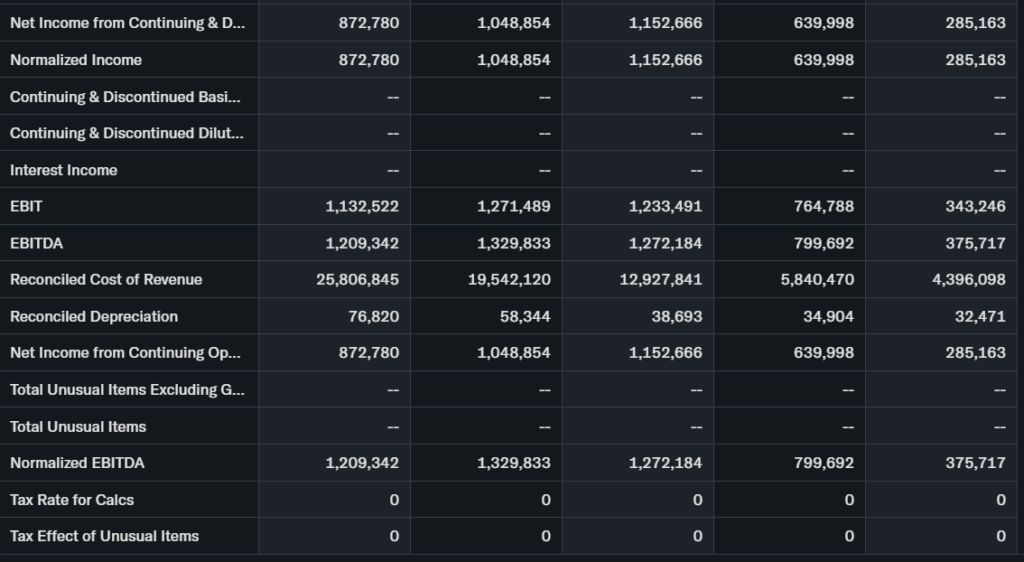

EPS at $1.37 TTM, down 40%, but expected up 19% to $2.22.

Free cash flow supports ops; debt low with solid cash from AI sales.

Versus peers like Dell, SMCI looks fairly valued post-drop, not overvalued.

Recent Earnings & Catalysts

Q2 revenue hit $5.76B, up 8.5% YoY but missed $5.88B estimates.

EPS beat but trailed forward views at $1.66 TTM.

Guidance points to AI-driven growth; catalysts include Nvidia ties and server launches.

Earnings caused initial dips, but partnerships lifted sentiment slightly.

Bullish Case

AI server demand fuels revenue growth at 35% TTM.

Tech edges in liquid-cooled systems aid market share.

Nvidia partnerships and efficiency gains support ops.

Bearish Case

Competition from Dell, HPE squeezes margins.

Growth slowed to 8.5% in latest quarter.

Regulatory probes and economic slowdowns add risks.

Market Sentiment

Short interest at 17.19% of float, down 2%, with 2.8 days to cover.

Institutions own 51%, steady but value dipped lately.

Retail shows momentum fade; overall neutral to fearful.

Short-Term Outlook

Technicals neutral with RSI balanced and light MACD buy.

Volume trends mixed; expect range-bound near $30-34 absent catalysts.

Medium to Long-Term Outlook

Strong AI model and industry tailwinds favor growth.

Financials healthy despite EPS dip; watch competition.

Long-term investors should hold or watch for accumulation below $30.

FAQ

Is SMCI stock a buy right now?

Hold for most; Buy if AI catalysts hit, per analysts.

What is the price target for SMCI stock?

Average $41-568, implying 27-700% upside potential.

What are major risks for SMCI stock?

Competition, margin pressure, growth slowdowns.

SMCI earnings outlook?

19% EPS growth expected next year.

SMCI long term outlook?

Positive on AI, but volatile.

Suggestions

Compare with Opendoor stock analysis.

See Nvidia stock forecast.

Read AI server sector breakdown.

Final Balanced Conclusion

Hold SMCI stock. Valuation fair post-correction, AI upside balanced by risks and weak recent earnings.

Disclaimer: This article is for informational purposes only and not financial advice.