Explore ROST stock analysis: latest price trends, Q4 earnings beat, analyst targets up to $224, and 2026 forecast. Is ROST stock a buy? Get insights now.

Introduction

Ross Stores runs off-price retail chains like Ross Dress for Less and dd’s DISCOUNTS. It sells discounted apparel, shoes, and home goods at 20-60% below full-price stores. Investors watch ROST stock closely after strong Q4 results beat estimates. Broader retail faces tariff pressures and consumer slowdowns, but off-price demand holds firm.

Latest Stock Price & Trend

ROST stock closed at around $137 on recent trading days, per last market data. It gained sharply post-Q4 earnings on March 3, 2026, leading gainers amid upbeat guidance. One-day performance surged on sales beats; five-day trend turned positive after tariff concerns eased.

One-month trend showed volatility from prior tariff news but stabilized. Three-month gains reflect steady comps growth; six-month uptrend built on Q3 strength. Year-to-date, ROST stock rose amid retail resilience. 52-week high hit near $190s earlier; low around $122 amid broader pressures.

Overall trend leans bullish short-term, signaling investor confidence in earnings momentum.

Technical Analysis

Support levels sit near $130, where buyers stepped in recently; resistance at $140-$145 tests upside. RSI reading hovered near 60 post-earnings, neutral-not overbought, showing balanced momentum without exhaustion. MACD trend flipped bullish, with line crossing signal for potential gains.

50-day moving average at $135 supports price; 200-day at $130 confirms uptrend base. No golden cross yet, but nearing if momentum holds; no death cross in sight. Trading volume spiked on earnings news, indicating strong interest. These indicators matter as they flag entry/exit points for beginners.

Analyst Ratings & Price Targets

16 analysts rate ROST stock: 13 Buy, 3 Hold, 0 Sell—strong buy consensus. Average price target $198.93; high $224, low $142. Recent boosts followed Q4 beats, per Benzinga. Wall Street firms like UBS note brand strength in slowdowns. This sentiment suggests upside potential for patient investors.

Insider Activity

Recent data shows steady insider selling in line with routine plans, no major buys noted. Management completed $1.05B buybacks in FY25, repurchasing 7.1M shares. New $2.55B authorization for FY26-27 signals confidence. Dividend hiked 10% to $0.445/share. This implies long-term optimism despite routine sales.

Valuation Analysis

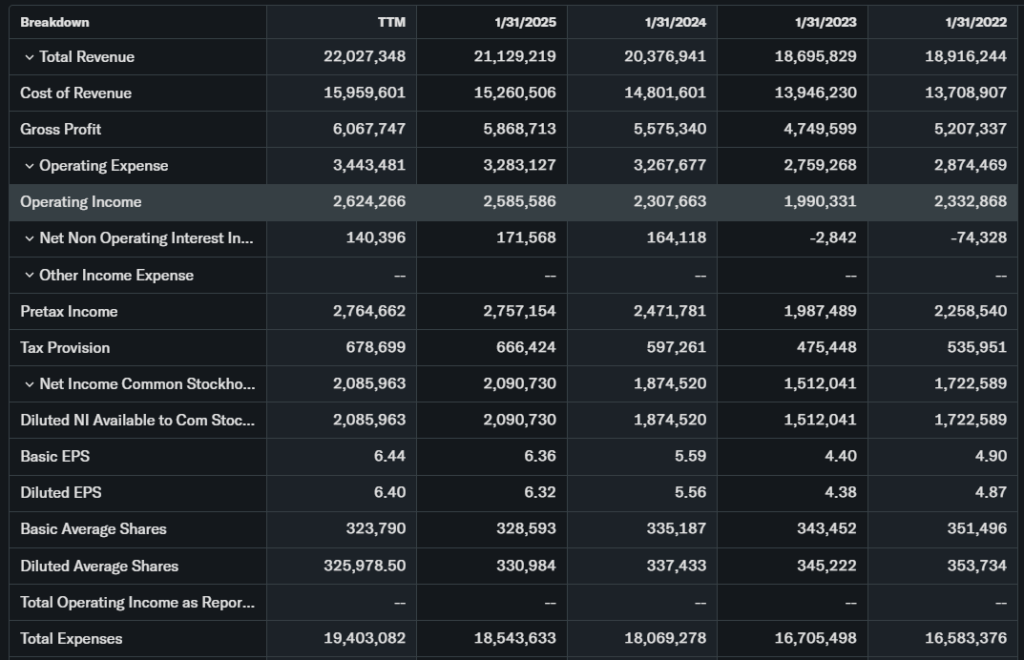

Trailing P/E around 29.8; forward P/E 26.81. Price-to-sales not specified but supported by 12% Q4 sales growth. Revenue up 12% YoY to $6.64B; EPS $2.00 beat forecasts. EPS growth strong at 9% comps. Free cash flow healthy; debt low with $92M net interest income projected.

Cash position solid for $1.1B capex. Vs. peers like TJX, ROST appears fairly valued—not cheap but justified by margins at 11.9% rising to 12-12.3%. Stock seems fairly valued for growth.

Recent Earnings & Catalysts

Q4 FY25 revenue hit $6.64B, +12% YoY, beating views; EPS $2.00 topped estimates. Comps rose 9%, COGS dipped 65bps. FY26 guidance: EPS $7.02-$7.36, sales +5-7%, comps 3-4%. Q1 outlook: sales +10-12%, EPS $1.60-$1.67.

Catalysts include supply-chain efficiencies and Spring momentum. Earnings drove post-report surge.

Bullish Case

Q4 comps strength points to sustained demand. Off-price model thrives in value-seeking economy. Margin gains from lower freight costs. $2.55B buybacks boost EPS. Store expansions via $1.1B capex fuel revenue.

Bearish Case

Tariff headwinds hit $0.05 in Q3, more possible. Consumer slowdown pressures spending. Competition from TJX, Walmart intensifies. Guidance pullback earlier on tariffs. Regulatory trade risks linger.

Market Sentiment & Investor Psychology

Short interest low, reflecting calm. Options show call buying post-earnings. Institutions hold steady; retail piled in on gains. Momentum favors bulls over value traps. Sentiment: optimistic on results.

Short-Term Outlook

Technicals show RSI stability, volume support. Earnings momentum and comps guide upside tests. Watch resistance at $145; expect volatility on retail data.

Medium to Long-Term Outlook

Strong model in off-price niche. Retail growth aids comps. Financials robust with buybacks. Hold for investors; accumulate on dips given targets.

FAQ Section

Is ROST stock a buy right now?

Yes, for growth seekers—13/16 analysts say buy.

What is the ROST stock price target?

Average $199; up to $224.

What are major risks for ROST stock?

Tariffs, competition, slowdowns.

ROST earnings outlook?

FY26 EPS $7.02-$7.36.

ROST stock forecast long-term?

Positive on margins, buybacks.

Suggestions

- Compare with Opendoor stock analysis

- See our off-price retail forecast

- Read retail sector valuation trends

Final Balanced Conclusion

Hold ROST stock—earnings strength and guidance support stability, but tariffs warrant caution. Targets suggest upside; suits patient portfolios.

Disclaimer: This article is for informational purposes only and not financial advice.