Peraso (PRSO) stock analysis with price trend, earnings, valuation, and forecast to help investors decide if PRSO stock is a buy or watch.

Introduction

Peraso Inc. is a small semiconductor company focused on high‑performance 5G millimeter‑wave (mmWave) wireless chipsets and modules used in fixed wireless access, immersive video, and industrial connectivity. PRSO stock has drawn attention from speculative growth investors because it offers exposure to specialized 5G infrastructure at a micro‑cap valuation, with sharp price swings and meaningful upside if execution improves.

This interest comes against a backdrop of a mixed tech market, where large‑cap AI and cloud names have led gains while smaller, unprofitable hardware and communications plays remain volatile and heavily discounted. For investors, PRSO stock sits squarely in the high‑risk, high‑reward part of the semiconductor and communications sector.

Latest Stock Price & Trend

As of the latest Nasdaq real‑time data, PRSO stock trades around 1.45–1.65 USD, with intraday moves near 9–10% not uncommon for this micro‑cap name. On the most recent trading day, Peraso shares slipped roughly 4–9% depending on the time snapshot, reflecting the stock’s typical intraday volatility rather than any single major news event.

Over the past five trading days, PRSO stock has been choppy but generally range‑bound, oscillating roughly between the low‑1 USD area and the mid‑1 USD area as traders react to momentum rather than fundamentals. The 1‑month and 3‑month views show a stronger rebound story: TradingView data indicates the stock is up more than 50% over the last month, reversing prior weakness as speculative interest picked up. Over six months and on a year‑over‑year basis, PRSO shows only a modest single‑digit percentage gain, underscoring how recent strength follows a long period of drawdowns.

The stock’s 52‑week range is extremely wide, with an all‑time low near 0.52 USD and much higher historical levels that reflect prior reverse splits and capital raises rather than sustainable valuations. Overall, the recent trend for PRSO stock is cautiously bullish in the very short term, but still fragile and highly sensitive to news, liquidity, and sentiment. For everyday investors, this pattern suggests PRSO is more appropriate for traders who can tolerate wide swings than for conservative buy‑and‑hold portfolios.

Technical Analysis

Technical analysis for PRSO stock starts with identifying support and resistance levels, which are price zones where the stock has repeatedly stopped falling or rising. Recent trading suggests support in the low‑1 USD region, where buying has tended to appear, while resistance emerges in the mid‑1 USD to 2 USD band, where rallies have often stalled. These levels matter because a break below support can signal more downside, while a clear move above resistance can indicate a new uptrend.

Momentum indicators like the Relative Strength Index (RSI) help gauge whether PRSO is overbought or oversold. An RSI above 70 typically signals overbought conditions, while below 30 suggests oversold; micro‑caps like PRSO often swing quickly between these zones, so traders should expect rapid shifts rather than smooth trends. The Moving Average Convergence Divergence (MACD) line tracks the relationship between short‑ and long‑term moving averages; a bullish MACD crossover (signal line crossing above) can hint at upward momentum, while a bearish crossover can warn of a pullback.

The 50‑day and 200‑day moving averages are widely watched trend gauges; when the 50‑day moves above the 200‑day, technicians call it a “golden cross,” often seen as bullish, while the reverse (“death cross”) is considered bearish. Given PRSO stock’s sharp volatility and long prior downtrend, its medium‑term moving averages have spent significant time in bearish alignment, though the recent rally has likely pulled the 50‑day average higher. Trading volume has spiked during up days, a sign that speculative traders are active; higher volume on up moves generally supports a near‑term bullish bias, while fading volume on rallies can signal exhaustion.

For beginners, the key takeaway is that PRSO stock technical analysis currently points to short‑term upside potential within a still‑fragile longer‑term picture.

Analyst Ratings & Price Targets

Wall Street coverage on Peraso is limited, but the available data show a small group of analysts following PRSO stock with generally constructive views on upside potential. Benzinga data indicates Peraso has a consensus price target around 3.38 USD, based on the ratings of two analysts. The highest published target is about 3.75 USD from Ladenburg Thalmann, while the lowest recent target is around 3 USD from Benchmark.

These targets imply the potential for well over 100% upside from recent trading levels if the company can execute on its growth plans. However, Seeking Alpha’s quantitative system currently assigns Peraso a “Strong Sell” rating, with weak grades for growth and profitability but a strong grade for valuation, reflecting cheap metrics relative to fundamentals. Nasdaq’s analyst research pages emphasize that these ratings and targets should complement, not replace, an investor’s own research.

In practical terms, analyst sentiment on PRSO stock is cautiously positive in terms of upside potential but tempered by operational and financial risks, and investors should treat the small analyst sample size as a limitation.

Insider Activity

Nasdaq’s insider activity data for Peraso highlight that executives and directors must report their trades to the SEC, but recent open‑market insider buying or selling in PRSO has been limited and sporadic. Third‑party trackers like Fintel aggregate historical insider trading and sentiment, yet much of the detailed tabular activity dates back several years and earlier corporate structures, offering limited guidance on the current management team’s recent conviction.

Because no large, highly visible cluster of insider buying has been reported in the latest period, investors cannot rely on insider transactions alone as a strong bullish signal. At the same time, there is no clear pattern of aggressive insider selling that would signal acute concern. For PRSO stock, insider activity appears neutral to slightly inconclusive, meaning investors should focus more on earnings trends, cash position, and execution.

Valuation Analysis

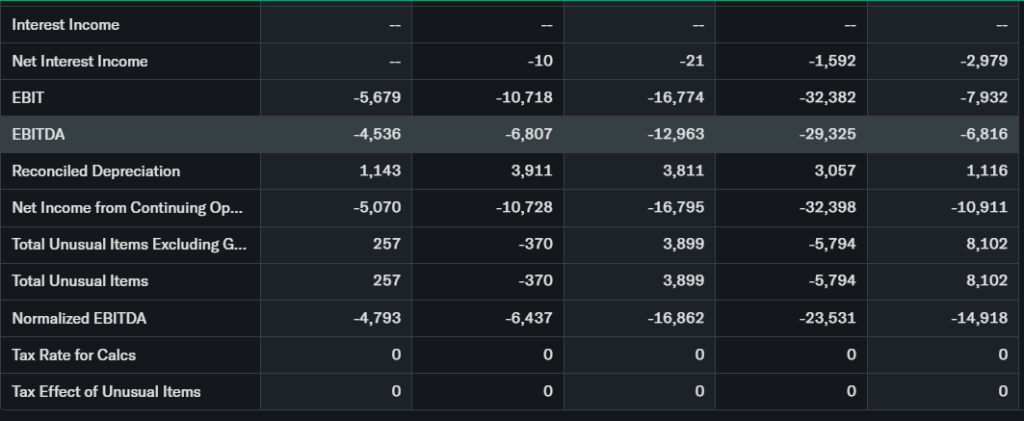

Yahoo Finance and TradingView data show that Peraso remains unprofitable on a trailing basis, with negative earnings per share and therefore a negative trailing P/E multiple. For the latest reported full year, Peraso generated total revenue of roughly 14.6 million USD, with cost of revenue around 7.0 million USD and operating expenses near 17.9 million USD, leading to operating losses. With a market capitalization in the low tens of millions of dollars, the company trades at a modest price‑to‑sales ratio relative to many larger 5G and networking peers.

Recent earnings reports show negative EPS but improving loss metrics; TradingView notes that Peraso delivered quarterly EPS of about −0.08 USD versus an estimate of −0.16 USD, beating expectations by roughly 50%. Revenue for that quarter came in around 3.87 million USD, slightly above the 3.79 million USD estimate, and management has guided for future quarterly revenue in the roughly 2.8–3.1 million USD range. GuruFocus‑based commentary highlights non‑GAAP gross margins above 50% and a cash balance near 1.9 million USD at the end of Q3 2025, indicating some efficiency but still tight liquidity.

Compared with much larger and profitable tech names like Microsoft or broad‑based communications leaders, Peraso trades at a far lower absolute valuation but also carries far greater risk due to its small scale, recurring losses, and dependence on a narrow product set. On balance, PRSO stock appears optically cheap on sales multiples yet risky due to negative earnings and limited cash; it may be viewed as speculatively valued rather than clearly undervalued or overvalued.

Recent Earnings & Catalysts

Peraso’s recent earnings results have been mixed but show pockets of operational progress. In its Q3 2025 report, the company highlighted record mmWave revenue and a sequential revenue increase driven by design wins and strategic partnerships, even though total net revenue of about 3.2 million USD was down year over year from 3.8 million USD. Non‑GAAP gross margin improved to 56.2% from 48.3% in the prior quarter, and GAAP net loss narrowed to 1.2 million USD (0.17 USD per share) from 1.8 million USD (0.31 USD per share).

Peraso’s Q3 2025 outlook called for Q4 revenue in the 2.8–3.1 million USD range, reflecting ongoing demand in its mmWave pipeline and a double‑digit number of customer devices in preproduction. Earnings‑related commentary from Zacks and other services notes that Peraso has occasionally beaten EPS expectations, such as the −0.08 USD result versus a −0.16 USD consensus. These earnings have influenced PRSO stock price with short‑term spikes when results or guidance surprise positively, although gains often fade as broader market risk appetite shifts.

Key catalysts going forward include additional design wins in fixed wireless access, expansion of AI‑adjacent and edge‑computing applications that rely on high‑bandwidth connectivity, and any strategic moves such as partnerships, licensing deals, or capital raises that strengthen the balance sheet.

Bullish Case

The bullish case for PRSO stock centers on three main pillars: technology positioning, revenue growth opportunities, and potential operating leverage. Peraso is a specialist in mmWave chipsets and modules, which are critical for high‑throughput 5G applications such as fixed wireless broadband, industrial automation, and immersive video. If demand for these use cases accelerates, especially in telecom and edge computing, Peraso could see faster revenue growth from its existing pipeline of preproduction customer devices.

Q3 2025 results show improving non‑GAAP gross margins and narrowing net losses, suggesting that incremental sales could scale more efficiently if volumes rise. With a small market cap and low price‑to‑sales ratio, even modest success in converting design wins to recurring production revenue could meaningfully move PRSO stock price. Analyst price targets in the 3–3.75 USD range underscore the possibility of substantial upside if the company executes well and market conditions remain supportive.

For growth‑oriented investors comfortable with high risk, PRSO stock offers leveraged exposure to a niche but strategically important part of the 5G ecosystem.

Bearish Case

On the downside, Peraso faces intense competition and persistent financial pressure. Larger semiconductor players and networking companies can outspend Peraso on R&D, sales, and customer support, making it harder for a micro‑cap specialist to win and retain major design slots. Revenue has been lumpy and, in some periods, down year over year, indicating that demand is not yet stable or broad‑based.

The company remains unprofitable, with negative EPS, ongoing operating losses, and a relatively small cash balance of about 1.9 million USD as of the end of Q3 2025. That raises the risk of future dilution through equity offerings or the need for other financing, especially if macroeconomic conditions tighten or customer ramps are delayed. Quantitative ratings flag weak growth and profitability grades, reflecting these structural challenges.

Investors must also consider broader risks, including economic slowdowns, slower 5G deployment timelines, and potential regulatory or trade disruptions affecting chip supply chains. These factors could weigh on PRSO stock and limit the realization of its bullish forecast.

Market Sentiment & Investor Psychology

Market sentiment around PRSO stock is shaped by its micro‑cap status, volatility, and speculative appeal. Quantitative tools on platforms like Seeking Alpha currently label the stock as “Strong Sell,” influenced by poor growth and profitability metrics despite attractive valuation grades. At the same time, analyst price targets that sit far above the current share price create a narrative of potential deep value for risk‑tolerant investors.

Short interest data for very small stocks like Peraso can fluctuate, but its modest float and frequent sharp moves suggest that both short‑term traders and short sellers are active. Options liquidity appears limited compared with larger names, so sentiment is more visible in common‑stock volume spikes than in call‑versus‑put balances. Institutional ownership is relatively low, consistent with many micro‑caps, which leaves PRSO stock more influenced by retail investors and momentum‑driven trading.

Overall sentiment looks neutral to cautiously optimistic: value‑oriented and speculative investors see upside, while quant models and conservative investors remain wary.

Short-Term Outlook

In the near term, PRSO stock is likely to remain highly sensitive to technical levels, market momentum, and news flow rather than gradual fundamental shifts. Recent price action above short‑term support in the low‑1 USD area, combined with stronger volume during up days, points to a mildly bullish short‑term bias as long as support holds. However, any reversal in risk sentiment in small‑cap tech or negative company‑specific headlines could quickly pressure the stock back toward its recent lows.

Short‑term traders may look for breakouts above recent resistance zones to confirm further upside, while cautious investors might prefer to wait for pullbacks or clearer evidence of sustained buying interest. Without making any price promises, the realistic expectation is continued volatility with the potential for sharp swings both higher and lower in the coming weeks.

Medium to Long-Term Outlook

Looking out over the next 6–24 months, the outlook for PRSO stock hinges on execution, funding, and the broader 5G adoption curve. Peraso’s business model as a focused mmWave chip and module provider positions it in a high‑growth niche of the communications and edge‑computing industry, where demand could expand as fixed wireless, industrial IoT, and immersive media mature. If the company can convert its pipeline of preproduction devices into sustained volume shipments, revenue growth could accelerate from the current low‑to‑mid single‑digit millions per quarter.

Financial health remains the key swing factor: continued operating losses and limited cash mean that Peraso must either reach near‑breakeven more quickly or secure additional capital on reasonable terms. Compared with diversified giants like Microsoft or larger communications platforms, Peraso’s competitive position is narrow and vulnerable, but that also allows for focused innovation in its chosen niche.

For long‑term investors, PRSO stock looks more suitable as a small speculative allocation to accumulate gradually or hold/watch rather than a core holding, with close monitoring of quarterly results, cash runway, and customer wins.

FAQ Section

1. Is PRSO stock a buy right now?

PRSO stock may appeal to aggressive, speculative investors who understand the company’s small size, ongoing losses, and volatility, but it is not a low‑risk buy for conservative portfolios.

2. What is the price target for PRSO stock?

Recent data show a consensus analyst price target near 3.38 USD, with individual targets ranging from about 3 USD to 3.75 USD.

3. How did the latest PRSO earnings look?

Peraso’s Q3 2025 results showed revenue around 3.2 million USD, improved gross margins, and a narrowed net loss compared with prior quarters, while still remaining unprofitable.

4. What are the major risks for PRSO stock?

Key risks include ongoing operating losses, a small cash position, competition from larger chipmakers, potential dilution, and cyclical or delayed 5G spending.

5. What is the long‑term outlook for PRSO stock?

Over 6–24 months, upside depends on converting design wins into recurring revenue and improving profitability; without that, dilution and volatility could dominate returns.

Suggestions

You could internally link this article to pieces such as:

- “Compare with Opendoor stock analysis”

- “See our Microsoft stock forecast” for readers interested in more stable large‑cap tech.

- “Read our tech sector valuation breakdown” for context on how PRSO stock fits into broader tech and semiconductor valuations.

Conclusion

PRSO stock offers a high‑risk, high‑potential setup tied to a niche but important part of the 5G ecosystem. The company’s improving gross margins, design‑win pipeline, and analyst price targets support a cautiously optimistic long‑term forecast, yet persistent losses, limited cash, and fierce competition mean downside risk remains substantial.

On balance, PRSO stock looks most appropriate as a watchlist to small speculative buy for experienced investors who can tolerate volatility, while more conservative investors may prefer to simply monitor future earnings and financing developments before committing capital.

Disclaimer: This article is for informational purposes only and not financial advice.