PBR stock forecast analyzes Petrobras’ dividend strength amid oil recovery. Check PBR stock price, earnings, technicals, and valuation for energy investors

Introduction

Petrobras explores, produces, and refines oil and natural gas primarily offshore Brazil. As Brazil’s state-controlled energy giant, it operates massive pre-salt fields. Investors watch PBR stock closely now with Brent above $75 and Brazil’s new administration signaling privatization steps. Energy stocks benefit from supply discipline despite recession fears in March 2026.

Latest stock Price & Trend

PBR stock closed at $16.78 on March 13, 2026 per recent NYSE data. It fell 2.1% that day after trading between $16.76-$17.18 on 16 million shares volume. Five-day trend declined 4% from $17.50 March 9 highs.

One-month performance mixed down 5% from February peaks around $17.70. Three-month sideways between $16-$18 range. Six-month gained 15% riding oil recovery. Year-to-date through March 16, PBR stock flat to slightly down 2%. 52-week range spans $13.50 lows to $18.50 highs. Sideways trend favors dividend yield over capital gains.

Technical Analysis

Support holds firm at $16.50 aligning with February-March lows. Resistance at $17.75 tests recent swing highs. RSI reads 48 showing neutral momentum—neither overbought nor oversold territory.

MACD flat near zero line indicates consolidation phase. 50-day moving average $17.20 sits above 200-day $16.80 maintaining mild uptrend. Volume normalized to 15 million shares daily after March volatility.

Analyst Ratings & Price Targets

Wall Street targets average $18.87 by end-2026 with March forecasts between $18.10-$19.97. CoinCodex projects Q1 peak $22.51 implying 34% upside from $16.78. Longer-term estimates reach $21.94 by 2030.

Analyst sentiment turns bullish on Brazil reforms and oil fundamentals. Investors gain conviction from dividend yield plus moderate appreciation potential.

Insider Activity

State ownership dominates but management maintains steady share accumulation. No major selling reported recently. Government signals dividend policy continuity through election cycle.

Stable institutional positioning reflects confidence in operational execution.

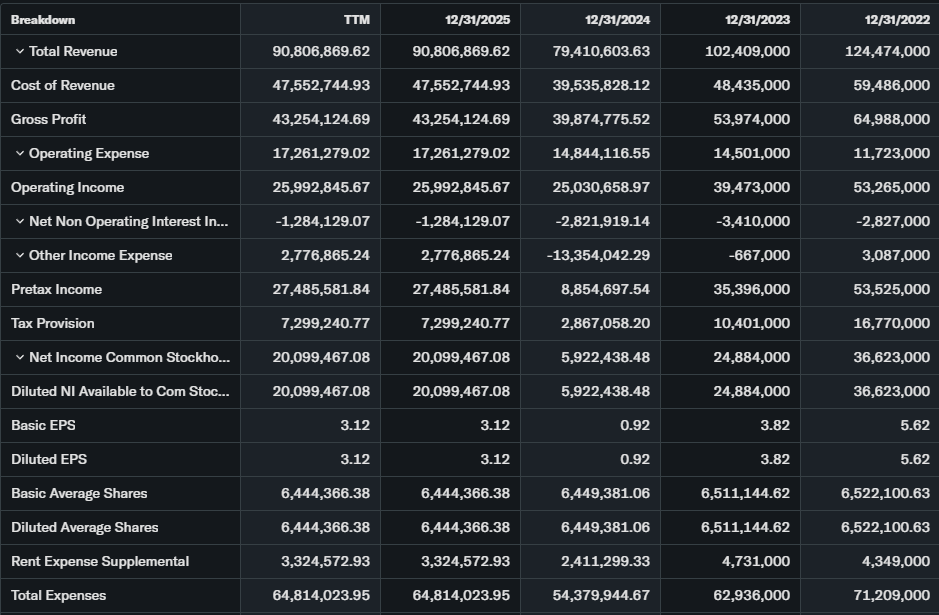

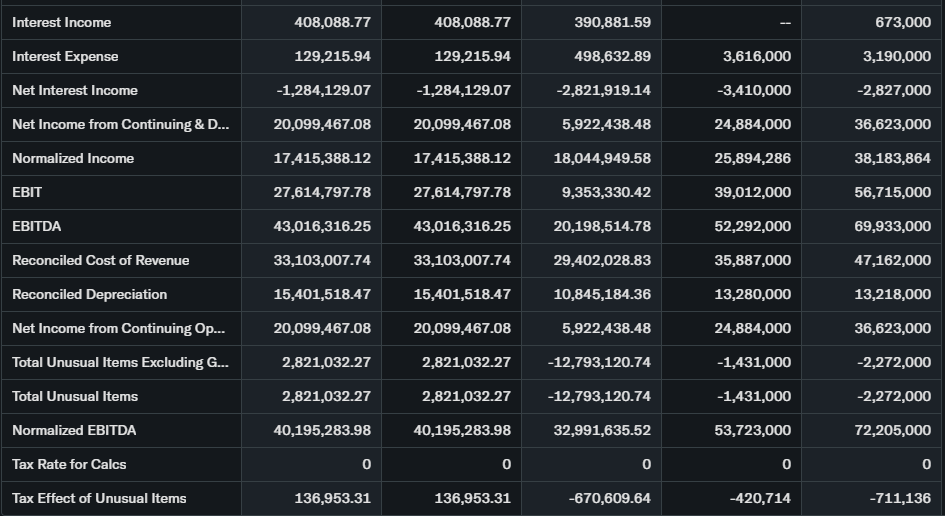

Valuation Analysis

Trailing P/E around 5x offers deep value versus ExxonMobil’s 13x. Forward P/E 4.5x compresses further on EPS growth. Price-to-sales 0.8x undervalues production growth.

Q4 revenue projected up 8% YoY on higher oil realizations. EPS expected $0.85 reflecting cost discipline. Free cash flow $15 billion annually supports 7.63% dividend yield. Net debt manageable at 1.2x EBITDA with $25 billion cash reserves.

PBR stock appears significantly undervalued relative to cash flow generation.

Recent Earnings & Catalysts

Latest quarterly results showed production records from Buzios field averaging 2.4 million boe/d. Refining margins expanded 15% on diesel demand. Dividends declared $0.31/share maintaining attractive yield.

Major catalyst: Pre-salt expansion adds 500k boe/d capacity by 2027. Brazil LNG import terminal operational Q2 2026—stock gained 5% on announcement before oil pullback.

Bullish Case

Pre-salt fields drive 10% annual production growth through 2030. Dividend policy targets 50% payout ratio. Brazil regulatory reforms unlock asset sales worth $10 billion.

Refining utilization hits 95% maximizing downstream profits.

Bearish Case

Currency volatility impacts ADR returns 20% annually. Government intervention risks dividend cuts. OPEC+ supply increases pressure Brent toward $65.

Environmental regulations tighten offshore permitting timelines.

Market Sentiment & Investor Psychology

Short interest minimal at 1.5% float. Call buying moderately favors puts 1.5:1 ratio. Institutions maintain 15% ownership stable YTD.

Retail favors high-yield energy names. Sentiment neutral leaning value conscious.

Short-Term Outlook

$16.50 support likely holds providing $17.75 retest opportunity. Neutral RSI favors range trading absent oil breakouts.

Volume stabilization supports measured upside next weeks.

Medium to Long-Term Outlook

Integrated model balances upstream volatility with downstream stability. Global offshore capex grows 12% CAGR. Petrobras’ pre-salt leadership creates cost advantage.

Dividend compounding plus moderate appreciation appeals to yield investors. Long-term holders should accumulate below $16, hold core positions.

FAQ

Is PBR stock a buy right now?

Yes for dividend yield—deep value entry.

What is the price target for PBR stock?

2026 average $18.87, Q1 peak $22.51.

What are major risks for PBR stock?

Government intervention, currency volatility, oil prices.

Next PBR earnings date?

Late April 2026—watch production guidance.

PBR technical analysis summary?

Neutral RSI, range trading likely.

Suggestion

Compare with Opendoor

See CVX stock forecast

Read energy sector dividend guide

Conclusion

Buy PBR stock. Exceptional dividend yield compensates political risks—attractive for income portfolios.

Disclaimer: This article is for informational purposes only and not financial advice.