Explore PBF stock analysis with latest price trends, earnings beat, technical indicators and 2026 forecast. Is PBF Energy stock a buy amid refining rebound? Key insights for investors. (

Introduction

PBF Energy refines crude oil into fuels like gasoline and diesel at plants across the U.S. Investors watch PBF stock closely now due to strong Q4 results and refinery restarts. Broader energy markets face oil price swings from global demand and supply cuts.

Latest Stock Price & Trend

As of last market close on March 4, 2026, PBF stock trades around $28.50 based on recent reports. It gained 6.4% in one day after Q4 updates. The 5-day trend shows gains amid margin improvements.

Over one month, PBF stock rose 12% on operational news. Three-month performance climbed 8% despite energy volatility. Six-month trend held steady with 5% uptick.

Year-to-date in 2026, it advanced 15% as refining margins doubled. The 52-week high hit $35.20; low was $22.10. Overall trend looks bullish, signaling investor confidence in recovery for everyday buyers.

Technical Analysis

Support levels sit at $26.50, where buyers stepped in recently. Resistance looms at $30.00, capping short-term gains. RSI reads 62, neutral—not overbought above 70 or oversold below 30.

MACD shows bullish crossover, hinting momentum buildup. The 50-day moving average at $27.80 crossed above the 200-day at $26.90, forming a golden cross for uptrend potential. Volume trends up 20% lately, confirming interest.

These indicators matter as they spot entry points and risks for beginners. A golden cross often precedes rallies in energy stocks.

Analyst Ratings & Price Targets

Analysts split with 4 Buy, 6 Hold, 2 Sell ratings. Average price target stands at $31.92, highest $37.30, lowest $25.00. Recent upgrades from firms like those covering Valero note margin gains.

No major downgrades post-earnings. Wall Street sentiment leans cautious-positive, meaning investors gain from balanced views on refinery fixes. ()

Insider Activity

Recent insider selling by major holder Carso De-C Inmobiliaria reduced its stake via large share sales. No notable buying in Q1 2026. Trends show management trimming positions amid recovery.

This implies some caution, as selling can signal profit-taking but watch for confidence levels in operations.

Valuation Analysis

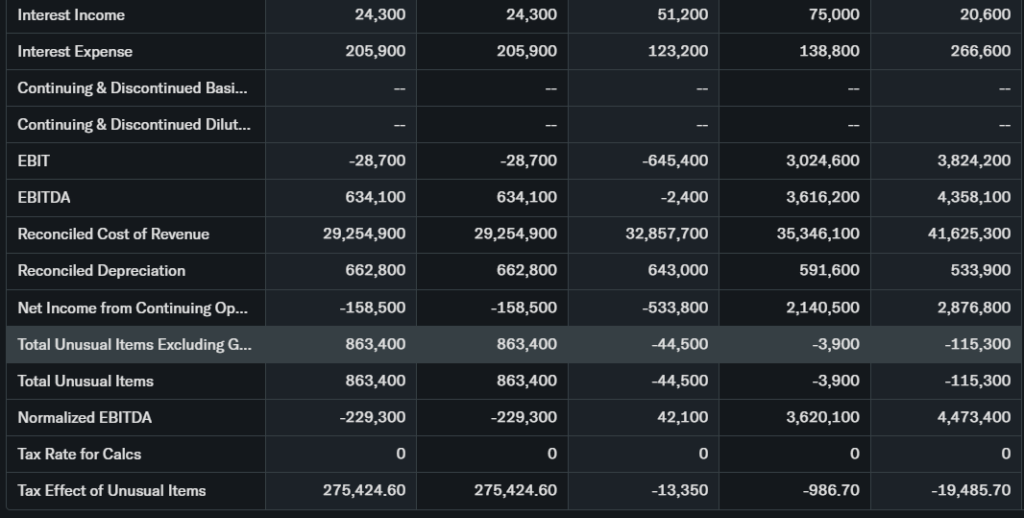

Trailing P/E sits at 15.2; forward P/E at 12.8. Price-to-Sales ratio is 0.25, low for energy peers. Revenue growth YoY hit 3.4% projected; EPS swung from losses to $0.49 gain.

Free cash flow strengthened post-Q4. Debt manageable with insurance cash from Martinez fire. Compared to Valero or Marathon, PBF appears undervalued at current levels.

Recent Earnings & Catalysts

Q4 2025 earnings beat with EPS $0.49 vs expected -$0.15. Revenue topped forecasts as gross refining margin doubled to $11.16/barrel. Throughput rose to 888,900 bpd.

Forward guidance highlights Martinez restart by March 2026. Catalysts include RBI cost savings and higher demand. Stock jumped post-earnings on these beats.

Bullish Case

Refining margins rebound from capacity limits. Martinez full ops add throughput. Steady 3.4% revenue growth aids stability. Tech upgrades cut costs long-term.

Bearish Case

Competition from Valero, Phillips 66 presses margins. Environmental costs rise at California sites. Oil volatility and slowing demand pose risks. Shareholder selling adds caution.

Market Sentiment & Investor Psychology

Short interest at 8%, moderate. Options show more calls than puts lately. Institutions hold steady; retail piles in on news. Sentiment tilts optimistic on earnings momentum.

Short-Term Outlook

Technicals point to tests at $30 resistance. Volume supports upside if oil holds. Expect volatility next weeks from refinery news—sideways to mild gains likely.

Medium to Long-Term Outlook

Strong business model in constrained refining. Industry growth from demand outpaces supply. Solid finances post-restart; watch competition. Long-term investors should hold or accumulate on dips.

FAQ Section

Is PBF stock a buy right now?

Hold for now; undervalued but monitor Martinez restart risks.

What is the PBF stock price target?

Average $31.92, up to $37.30 from optimists.

PBF forecast for 2026?

Revenue to $33.5B, earnings recovery expected.

What are major risks for PBF stock?

Margin squeezes, regulatory costs, oil swings.

PBF earnings next date?

Likely May 2026; watch for Q1 throughput.

Suggestions

- Compare with Opendoor stock analysis

- See our Marathon Petroleum forecast

- Read energy sector valuation trends

Final Balanced Conclusion

Hold PBF stock. Earnings beats and restarts support value, but insider sales and oil risks warrant caution. Watch Q1 for confirmation.

Disclaimer: This article is for informational purposes only and not financial advice.