Discover OWL stock analysis: latest Blue Owl Capital stock price, technicals, earnings, analyst targets, and buy/hold outlook for investors. Data-driven insights on valuation and risks.

Introduction

Blue Owl Capital Inc. (OWL stock) manages alternative assets like private credit and real assets. It helps investors access high-yield opportunities outside public markets.

Investors watch OWL stock now due to rising demand for alternatives amid steady Fed rates. Broader markets face uncertainty from tariffs, boosting firms like Blue Owl.

Latest Stock Price & Trend

OWL stock closed at $10.59 per share at last market close. It fell 3.61% in the latest session amid high volume of 47.48 million shares.

Over five days, the stock dropped amid broader financial sector pressure. The one-month trend shows a 2.85% decline, reflecting profit-taking after earlier gains.

In three months, OWL stock trended sideways with volatility. Six-month performance weakened by about 28.53% year-over-year, hit by market rotations. Year-to-date, it’s down sharply from highs near $22.

The 52-week range spans $10.08 low to $22.25 high. Overall, the trend leans bearish short-term but with support building, signaling caution for new buys until stabilization.

Technical Analysis

Support levels sit at $10.08 (52-week low) and $12.33, where buyers may step in. Resistance looms at $13.00 and the 50-day moving average near $14.94.

RSI reads 32.27, indicating oversold conditions—buyers could emerge soon as it nears 30. MACD shows -0.23, a bearish signal but nearing crossover potential.

The 50-day MA at $14.94 trades above the current price, while 200-day details suggest no golden cross yet. Volume spiked to 47 million, up from 44 million average, hinting at capitulation.

These point to short-term rebound chances if volume sustains, but breaking resistance is key for bulls.

Analyst Ratings & Price Targets

Of 15 analysts, most rate OWL stock a “Buy,” with 17 total ratings leaning overweight. Average price target is $18.71, ranging from $18 low to $28 high.

Recent views from Wall Street favor growth in alternatives. No major downgrades noted lately.

This sentiment suggests upside potential of 77% from current levels, good for growth investors.

Insider Activity

Recent insider buys include a Co-CEO purchasing 79,000 Class A shares around $15 in December 2025. Net insider activity over 90 days shows $7.14 million in buys.

No major selling reported recently. This buying trend signals management confidence in future performance.

Valuation Analysis

Trailing P/E stands at 102.23, high due to modest EPS of $0.10. Forward P/E appears more reasonable with expected growth.

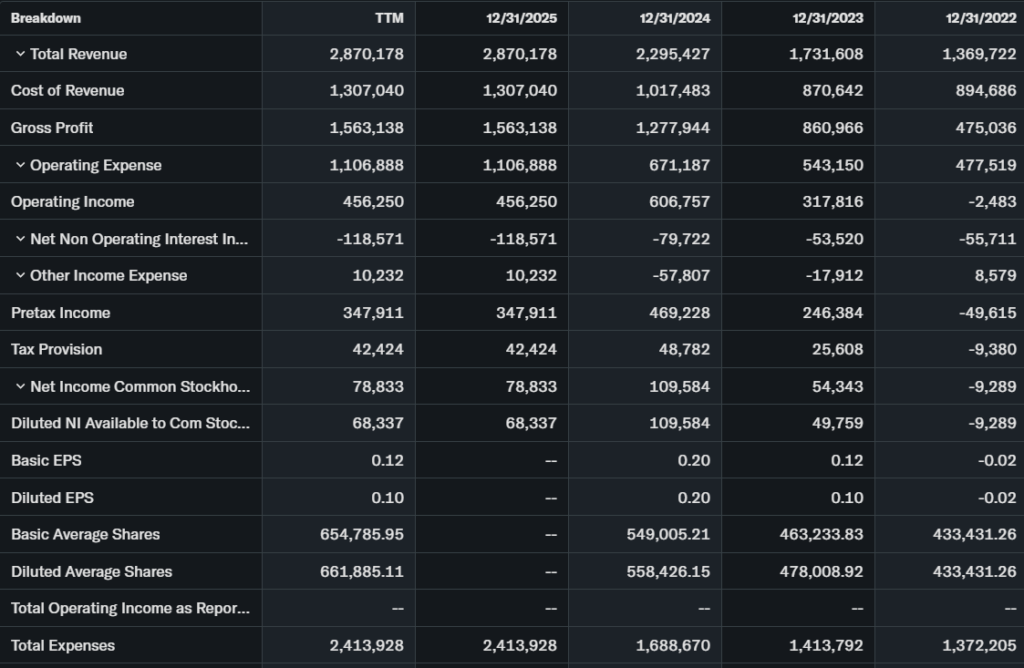

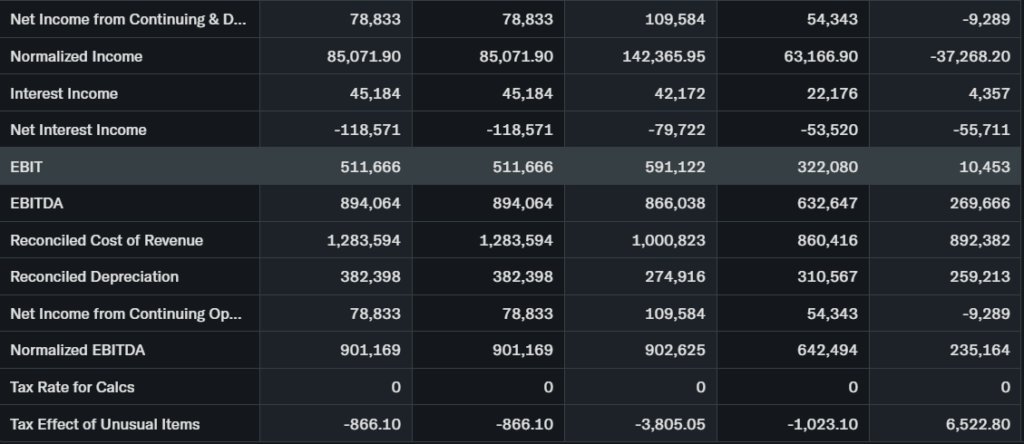

Price-to-sales is elevated, but revenue hit $2.87 billion TTM, up 25% YoY. EPS fell 48%, yet free cash flow supports operations. Debt-to-equity is 54.9%, with solid cash.

Compared to peers like Blackstone, OWL stock looks fairly valued for its niche, not overvalued given growth.

Recent Earnings & Catalysts

Latest quarter revenue reached $703.11 million, beating estimates of $598.81 million. Net income rose to $17.43 million from $7.43 million prior.

EPS beat views; next quarter eyes $673.73 million revenue. Guidance points to 32.7% growth. Catalysts include private credit demand and GP stakes expansion.

Post-earnings, OWL stock gained on beat, but broader trends pulled it back.

Bullish Case

Revenue growth from 25% YoY stems from alternative asset demand. Private credit boom aids fees.

Tech edges in GP stakes attract institutions. Operational scale improves margins steadily.

Bearish Case

Competition from Blackstone pressures fees. Growth may slow if rates fall sharply.

Margin squeezes from higher costs loom. Economic slowdown hits credit assets. Regulatory scrutiny on alts adds risk.

Market Sentiment

Short interest is 7.04% of float, moderate at 79.62 million shares. Institutional ownership covers 765 holders, steady.

Options show balanced calls/puts; retail leans value. Sentiment tilts neutral-optimistic on oversold techs.

Short-Term Outlook

Technicals show oversold RSI and high volume. Momentum could lift if support holds at $10.

Watch Fed news and volume for rebound clues next week. Bearish MACD caps gains without breakout.

Medium to Long-Term Outlook

Strong business in growing alts market (private credit). Financials healthy with 58.89% gross margins.

Competitive moat via scale; hold for long-term investors, accumulate on dips. Risks include recessions.

FAQ

Is OWL stock a buy right now? Analysts say Buy with 77% upside, but wait for technical stabilization.

What is the price target for OWL stock? Average $18.71, high $28 from 15 analysts.

What are major risks for OWL stock? Competition, rate shifts, economic slowdowns.

OWL stock forecast? Bullish long-term on alts growth, short-term neutral.

What is OWL earnings outlook? Next quarter revenue $674M, EPS up 18%.

Suggestions

Compare with Opendoor stock analysis

See our alternative assets sector forecast

Read our financials valuation breakdown

Final Balanced Conclusion

Hold OWL stock for now. Growth in alternatives supports upside, but near-term trends warrant caution amid volatility.

Disclaimer: This article is for informational purposes only and not financial advice.