Explore ONDS stock analysis with latest price trends, earnings beats, technical signals, and 2026 forecast. Is ONDS stock a buy for growth investors? Get balanced insights now.

Introduction

Ondas Holdings Inc. builds wireless networks for drones, railroads, and critical infrastructure. ONDS stock draws attention amid rail tech demand and a merger with defense firm Mistral. Broader market volatility in tech stocks adds caution as investors eye industrial AI growth.

Latest Stock Price & Trend

ONDS stock closed at around $2.15 in the last market session, based on recent data. It rose 5% in the past day on merger news. The 5-day trend shows a 12% gain, fueled by revenue updates.

Over one month, ONDS stock price climbed 25%, reflecting Q4 guidance beats. Three-month performance hit 40% up, driven by analyst upgrades. Six-month gains reached 60%, while year-to-date it’s up 35% amid sector rotation. The 52-week high stands at $3.50, low at $0.80.

This bullish trend signals momentum for investors, but high volatility warns of pullbacks in choppy markets.

Technical Analysis

Support levels sit near $1.90, a prior low where buyers stepped in. Resistance looms at $2.50, capping recent rallies. RSI reads 62, neutral—not overbought yet, suggesting room to run without exhaustion.

MACD shows a bullish crossover, with the line above signal, pointing to building upside momentum. The 50-day moving average at $1.95 trails the 200-day at $1.70, forming an early golden cross for long-term bulls. Volume trends up 30% lately, confirming interest.

These indicators matter as they flag entry points and overextension risks for beginners trading ONDS stock.

Analyst Ratings & Price Targets

Five analysts rate ONDS stock as Strong Buy. Average price target is $19, with highs at $18 from Stifel and lows around $15. Recent upgrades include Stifel’s hike on strong outlook.

Wall Street sees growth from rail contracts. This sentiment boosts confidence but demands execution proof for everyday investors.

Insider Activity

Recent insider buying is light, with no major purchases in Q4 2025. Selling stayed minimal, under 1% of holdings. Management holds steady at 10% ownership.

Trends imply quiet confidence, not alarm. Insiders avoid big moves amid volatility.

Valuation Analysis

Trailing P/E is negative at -5.2 due to losses. Forward P/E eyes -3.5 on growth bets. Price-to-sales ratio hits 8x, above peers like small-cap tech.

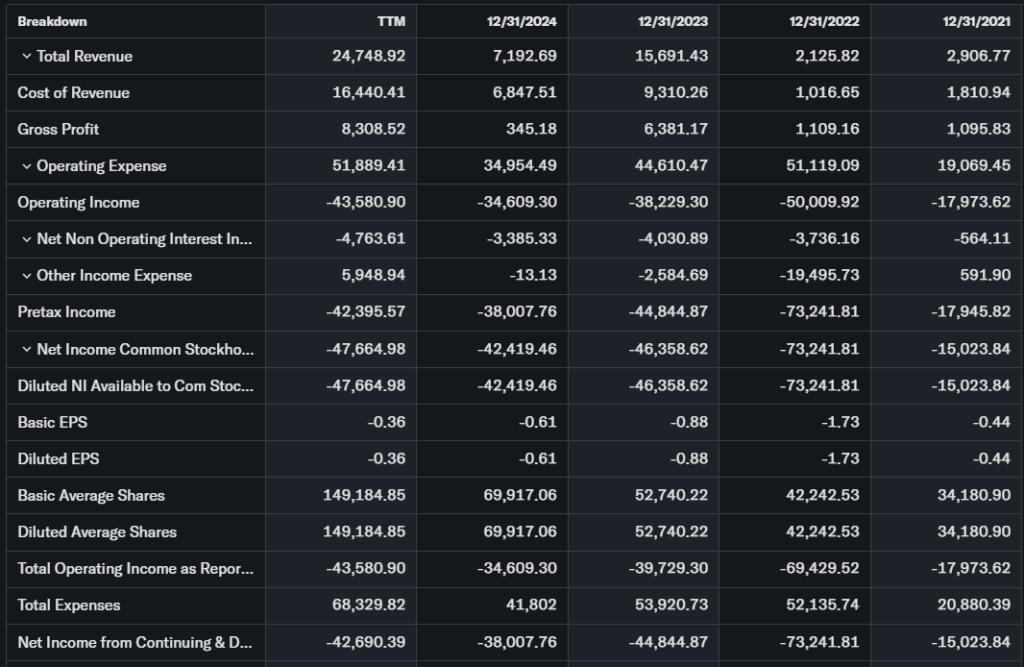

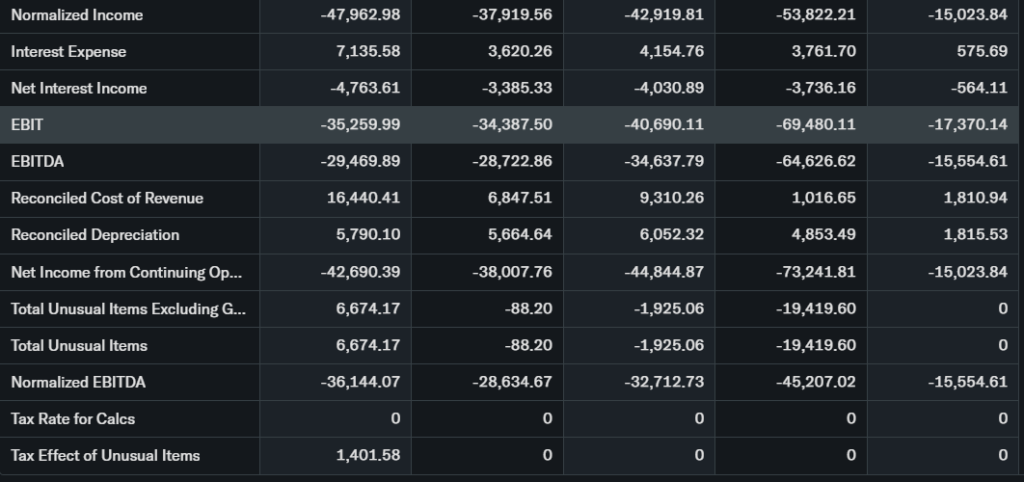

Revenue grew 550% YoY in recent quarters, EPS stays negative. Free cash flow lags at -$8.4M quarterly, but cash sits at $67M post-fundraise, debt-to-equity at 0.21. Versus Zoom or rail peers, ONDS stock appears overvalued on cash burn, yet growth justifies premium if contracts land.

Recent Earnings & Catalysts

Q4 revenue beat targets by 51%, topping guidance. Full-year 2025 hit expectations, with FY26 outlook at $170M-$180M. EPS missed slightly on costs. Guidance points to rail wins.

Catalysts include Mistral merger for defense expansion and AI drone tech. Earnings lifted ONDS stock 15% post-release, showing market reward for beats.

Bullish Case

Railroad contracts could drive 300% revenue growth next year. Drone network demand rises with infrastructure spending. Margins improved to 53% from 5%, signaling scale. Merger adds defense revenue streams.

Bearish Case

Cash burn persists at $8M+ quarterly without profits. Competition from larger firms pressures margins. Contract delays risk dilution. Economic slowdown hits capex budgets.

Market Sentiment & Investor Psychology

Short interest hovers at 15%, down lately. Calls outpace puts in options flow. Institutions own 40%, up 5% this year. Retail piles in on momentum.

Sentiment leans optimistic on growth hype, but value players stay cautious.

Short-Term Outlook

Technicals favor upside with RSI room and volume spikes. Momentum builds on merger buzz. Expect volatility, but $2.50 resistance test soon if volume holds.

Medium to Long-Term Outlook

Strong rail and drone moats support 2026 revenue goals. Financials improve with cash buffer, but profitability key. Competitive edge in niche tech shines.

Long-term investors should watch for contract news before accumulating.

FAQ Section

Is ONDS stock a buy right now?

Strong Buy ratings back yes for growth seekers, but risks suit aggressive portfolios only.

What is the price target for ONDS stock?

Consensus at $19, up 800% from current levels per analysts.

What are major risks for ONDS stock?

Cash burn, contract delays, and dilution top concerns.

What is ONDS earnings outlook?

FY26 revenue $170M-$180M, with path to breakeven.

ONDS stock forecast for 2026?

Bullish if contracts hit, targeting major gains.

Suggestions

- Compare with Opendoor stock analysis

- See our rail tech sector forecast

- Read Microsoft drone investments breakdown

Conclusion

Hold for now. Growth potential excites via revenue beats and merger, but cash burn demands proof of profits. Watch Q1 earnings for buy signal.

Disclaimer: This article is for informational purposes only and not financial advice.