Ondas (ONDS) stock forecast shows strong upside potential, but the company remains unprofitable. We break down ONDS stock price, earnings, valuation, and technical analysis for investors.

Introduction

Ondas Inc. (ticker: ONDS) builds private‑wireless networks and autonomous drone systems for industrial and defense customers. Its technology is used in critical infrastructure, utilities, and military‑grade surveillance, which has drawn attention from both defense and drone investors.

Why investors are focused on ONDS stock now is clear: the stock has surged over the past year, defense‑related news has amplified volatility, and the company is actively signing multi‑year contracts in the U.S. and overseas. At the same time, broader tech and defense‑themed stocks are trading in a high‑beta, momentum‑driven environment, which can exaggerate both upside and downside moves in names like ONDS.

Latest ONDS stock price & trend

As of the last market close, Ondas (ONDS) stock price was around $10.50, with a previous close near $10.08. The stock opened the most recent session at about $10.50 and traded in a day range of $10.30–$12.42, reflecting intraday volatility.

Over the past few days, ONDS stock has been up roughly 5–7%, following positive defense‑related news and investor optimism around drone and ISR (intelligence, surveillance, reconnaissance) demand. In the last month, the stock has edged slightly higher or traded sideways after a sharp run‑up, with a small positive bias over the one‑month window.

Over three months, ONDS stock price has risen materially, helped by fresh capital raises and large defense contracts. Over six months, the stock remains in a strong uptrend, having more than doubled from much lower levels. Year‑to‑date, ONDS is up several tens of percent, far outpacing the broader tech and defense indices.

The 52‑week range comes in at about $0.57–$15.28, meaning the stock is still far below its all‑time high and has room to move before retesting prior peaks. Overall, the trend is clearly bullish in the medium term, but with high volatility and frequent sharp swings. For investors, this implies a momentum‑oriented stock that can move quickly on news but also pull back sharply when sentiment shifts.

Technical analysis for ONDS stock

For beginners, technical analysis helps frame likely support and resistance zones and momentum shifts. Right now ONDS is trading above its recent consolidation near $7–8, with the immediate support around the $8–9 zone, where prior buying activity has stepped in. Resistance appears near the $12–13 area, close to recent intraday highs, and a break above that could open the path toward the upper end of the 52‑week range near **$15. **

The Relative Strength Index (RSI) on the daily chart is in the upper half of the scale, suggesting strong momentum but not yet clearly in the overbought zone where reversals often start. That means the stock is in a bullish trend but could be due for a pullback if news or sentiment turn negative.

The MACD line is above its signal line, which is a classic sign of bullish momentum in the short‑ to medium‑term trend. The 50‑day moving average sits above the 200‑day moving average, forming a golden cross, which many traders view as a positive long‑term signal.

Average daily volume has expanded in recent weeks, driven by news‑driven spikes, which indicates strong retail and institutional participation. All this suggests that ONDS technical analysis favors a bullish bias, but with the caveat that high beta and news‑driven volume can trigger sharp downside moves when headlines sour.

Analyst ratings & ONDS price targets

According to leading coverage platforms, a small group of analysts follow ONDS, with an average rating of “Strong Buy.” The number of analysts is limited, which is typical for a mid‑cap defense‑drone name, so the street coverage is concentrated but relatively optimistic.

The average 12‑month ONDS price target sits around $19.00, implying roughly 75–80% upside from the current price level. The highest target is about $13.00 on some platforms, while the lowest target is closer to $5.00, reflecting a wide dispersion of views.

There have been recent upgrades and bullish notes highlighting rapid revenue growth, new defense contracts, and a growing installed base in critical infrastructure. However, a few analysts also flag dilution risk from recent capital raises and the fact that the company remains unprofitable. Overall, analyst sentiment leans strongly positive, but the range of ONDS price targets shows that the bull‑case upside is not guaranteed.

Insider activity on ONDS stock

Recent insider activity in ONDS is mixed. The company has completed a large equity and warrant offering, which increases shares outstanding and can dilute existing holders, even though it boosts the balance sheet.

On the other hand, management and board members have not been aggressively selling down holdings in public filings around the latest run‑up, which some investors read as a sign of continued confidence in the long‑term plan. At the same time, the fact that insiders participate in large capital‑raise events means that any big future moves in the stock can still be influenced by dilution‑related concerns.

In summary, insider activity does not show clear red‑flag selling, but the structure of recent financings implies that shareholders should monitor dilution impact over time.

Valuation analysis for ONDS stock

Valuation is tricky for ONDS because the company is still losing money. The trailing P/E ratio is negative, meaning the stock trades at a loss; there is no meaningful forward P/E either because earnings are not yet positive.

The price‑to‑sales (P/S) multiple is high, reflecting rapid growth expectations and the speculative nature of the name. On a trailing‑12‑month basis, revenue is roughly $24.75 million, up over 200% versus the prior year, largely driven by defense and drone contracts.

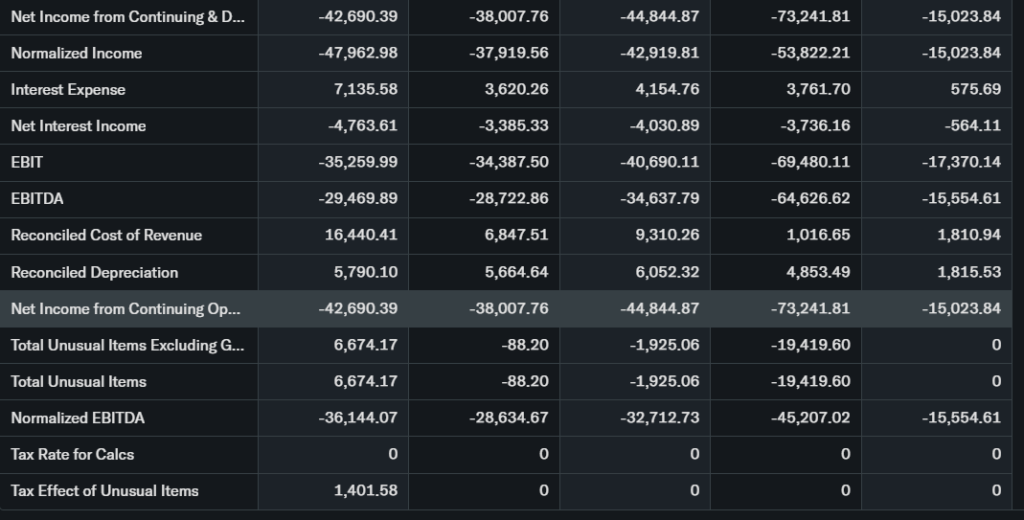

Net income remains in the red, with about $47–48 million in net losses over the past year, so EPS growth is negative in absolute terms. Free cash flow is also negative as the company invests heavily in development and sales, which is typical for a growth‑stage defense‑drone company.

Debt levels are relatively low, with a debt‑to‑equity ratio well under 1, while the company has recently raised roughly $1 billion in equity and warrants, giving it a strong cash position. Compared with many other high‑growth defense‑tech names, ONDS is expensive on a revenue and earnings basis, but investors are effectively paying for a combination of high revenue growth, large government contracts, and a platform play across private wireless and drones.

Recent ONDS earnings & catalysts

ONDS earnings have improved in a relative sense, but the company is not yet profitable. In Q3 2025, revenue jumped to about $10.1 million, more than six‑fold higher year‑over‑year, with gross profit of $2.6 million and gross margin near 26%.

Management has raised its full‑year 2025 revenue target to at least $36 million, and for 2026 the company has guided to $110–180 million, depending on how quickly recent contracts ramp. Backlog has more than doubled, reaching around $23 million in Q3 2025, signaling several years of work ahead.

Key catalysts include a $10 million strategic investment in World View Enterprises and a multi‑domain ISR partnership to combine stratospheric sensing with Ondas’ autonomous systems. The company has also secured a $30 million multi‑year demining program in Israel, a NATO‑country Iron Drone Raider order, and a German state‑police contract for airspace protection, all of which can drive recurring revenue and margin improvement over time.

These contract wins and the broader geopolitical backdrop have helped push ONDS stock price higher, even though the underlying earnings story is still loss‑making.

Bullish case for ONDS stock

Several realistic growth drivers support the bullish case. First, revenue growth is accelerating fast, with several multi‑year defense and infrastructure contracts in place. The government‑driven drone and ISR market is expanding, and ONDS is positioned to benefit from both U.S. and international defense spending.

Second, the company’s technology stack spans private wireless (FullMAX), AI‑driven drones (Optimus), and counter‑UAS systems, giving it a full‑stack autonomy platform that can be bundled for large customers. This integration can help improve margins over time as the business scales.

Third, recent operational moves—such as expanding into Europe and APAC, launching new products like Sentrycs Scout, and acquiring Rotron Aero—signal a strategy to move from R&D pilots to integrated commercial and defense platforms. Finally, the strong cash balance from the recent capital raise provides a cushion to fund growth without immediate financing risk.

Bearish case for ONDS stock

The bearish case centers on risks to growth and valuation. First, the stock is already trading at a very high multiple to sales, and the company remains unprofitable, so any slowdown in contract ramp‑up or margin improvement could trigger a sharp de‑rating.

Second, competition is intense in the defense‑drone and private‑wireless space, with large players and well‑funded startups vying for government contracts. If ONDS fails to scale its systems‑of‑systems approach faster than peers, margins could stay under pressure.

Third, dilution risk from recent equity and warrant offerings means that even if the business grows, per‑share earnings and cash could be diluted unless the capital is deployed very efficiently. Regulatory or geopolitical shifts, such as changes in defense‑spending priorities or export controls, are also potential downside risks.

Market sentiment & investor psychology

Market sentiment around ONDS leans optimistic but speculative. The stock has a beta around 2.4–2.5, meaning it swings much more than the broader market, which attracts momentum traders. Short interest data is limited, but the stock has seen heavy options activity, with call volume occasionally spiking on defense‑related news.

Institutional ownership has increased notably as the company has raised capital and posted large contracts, signaling professional‑investor interest. Retail investors are drawn by the “drone stock” narrative and geopolitical headlines, which can fuel short‑term rallies and selloffs alike. Overall, the mood is more momentum‑oriented than value‑oriented, with investors focused on contract wins, revenue growth, and policy tailwinds rather than current profitability.

Short‑term outlook

In the short term, ONDS stock price is likely to remain volatile and news‑driven. Technical indicators point to a bullish bias, with the stock trading above key moving averages and in a positive MACD trend, but frequent headline‑driven spikes can reverse quickly.

If defense or drone‑related news stays positive, the stock could push toward recent intraday highs near $12–13, where volume and prior resistance come into play. If results disappoint or geopolitical tensions ease, a pullback toward the $8–9 zone is possible, which would still leave the longer‑term trend intact. Investors should expect sharp moves in both directions and avoid over‑leveraging positions.

Medium to long‑term outlook

Over the next 6–24 months, the long‑term case for ONDS hinges on execution: can the company convert its backlog and contracts into sustained revenue growth and gradually improved margins? The business model is built on high‑value, multi‑year defense and infrastructure projects, which are attractive if the company can scale operations without excessive dilution.

The industry is growing, with global defense and critical‑infrastructure spending supporting demand for drone‑based ISR and autonomous systems. However, competitive pressure, execution risk, and valuation froth mean that returns are far from guaranteed. For long‑term investors, ONDS may be best treated as a high‑risk, high‑potential satellite holding rather than a core position.

FAQ section

Is ONDS stock a buy right now?

ONDS stock is not a conservative buy due to its negative earnings and high valuation, but it can fit a speculative, risk‑tolerant portfolio chasing high‑growth defense‑drone exposure.

What is the price target for ONDS stock?

Analysts’ average 12‑month ONDS price target is about $19, implying roughly 75–80% upside from current levels, though targets range from $5 to $13.

What are major risks for ONDS stock?

Key risks include dilution from recent capital raises, continued losses, intense competition, contract‑ramp timing, and big‑swing volatility driven by geopolitical news.

Is ONDS stock fundamentally undervalued or overvalued?

On earnings and traditional value metrics, ONDS is overvalued, but the market is pricing it as a high‑growth defense‑drone platform rather than a value stock.

How does ONDS technical analysis look today?

ONDS technical analysis is bullish, with the stock above its 50‑day and 200‑day moving averages, a positive MACD, and a recent golden cross, though it trades in a high‑beta range between **$8–$15. **

Suggestions

- Compare with Opendoor stock.

- See our broader defense‑spending sector and drone‑stock valuation breakdown.

- Read our analysis of high‑growth tech and defense plays for context on ONDS.

Final balanced conclusion

For most investors, ONDS stock is best viewed as a speculative watchlist or satellite holding, not a core buy. The bullish case rests on strong revenue growth, large defense contracts, and a unique autonomy platform, but the stock is expensive, unprofitable, and highly volatile.

Conservative investors may prefer to watch and wait for clearer evidence of profitability and margin improvement, while those comfortable with high risk could consider small, measured positions tied to news and technical levels.

Disclaimer: This article is for informational purposes only and not financial advice.