OKTA stock analysis reveals $71.98 close after Q4 beat, with 11% revenue growth and $115 target. Explore OKTA stock price trends, earnings, and if OKTA stock is a buy.

Introduction

Okta provides cloud-based identity management solutions. It helps companies secure access to apps and data. Investors watch OKTA stock closely after its Q4 2026 earnings beat forecasts.

Tech stocks face pressure from economic uncertainty. Yet Okta shows resilience with strong cash flow. Broader market volatility impacts cybersecurity demand.

Latest Stock Price & Trend

OKTA stock closed at $71.98 on the last market session, down 0.74% in after-hours after Q4 results. The one-day performance reflects caution despite earnings wins. Over five days, it held steady amid tech sector dips.

In the past month, OKTA stock price trended sideways with minor gains. Three-month view shows 2-3% recovery from earlier lows. Six-month trend points to 10% rise, driven by subscription growth.

Year-to-date, OKTA stock is up about 1.5%, lagging broader indices. The 52-week high sits near $100, low around $75. Overall, the trend leans bullish but cautious, signaling potential for investors if momentum builds.

Technical Analysis

Support levels hover at $70, where buying often emerges. Resistance sits at $80, capping recent upsides. These levels matter as they guide entry or exit points for traders.

RSI reading around 50 indicates neutral, neither overbought nor oversold. MACD shows a mild bullish crossover, hinting at building momentum. Investors use RSI to spot reversal risks.

The 50-day moving average at $74 crosses above the 200-day at $72, forming a golden cross. This suggests upward trends. Trading volume rose post-earnings, supporting interest.

Analyst Ratings & Price Targets

Analysts rate OKTA stock mostly Buy or Hold. Out of 35 firms, 20 Buy, 12 Hold, 3 Sell. Average price target is $105, high $130, low $85.

Recent upgrades from firms like Piper Sandler cite strong RPO growth. This sentiment implies confidence in Okta’s path, but investors should weigh macro risks.

Insider Activity

Insider selling dominated recently, with executives offloading 50,000 shares last quarter. No major buying noted. CEO Todd McKinnon sold modestly.

This trend suggests caution, not panic. Management holds significant stakes, implying long-term confidence despite sales for diversification.

Valuation Analysis

Trailing P/E stands at 150x due to past losses turning positive. Forward P/E improves to 45x on expected EPS growth. Price-to-sales ratio is 7x.

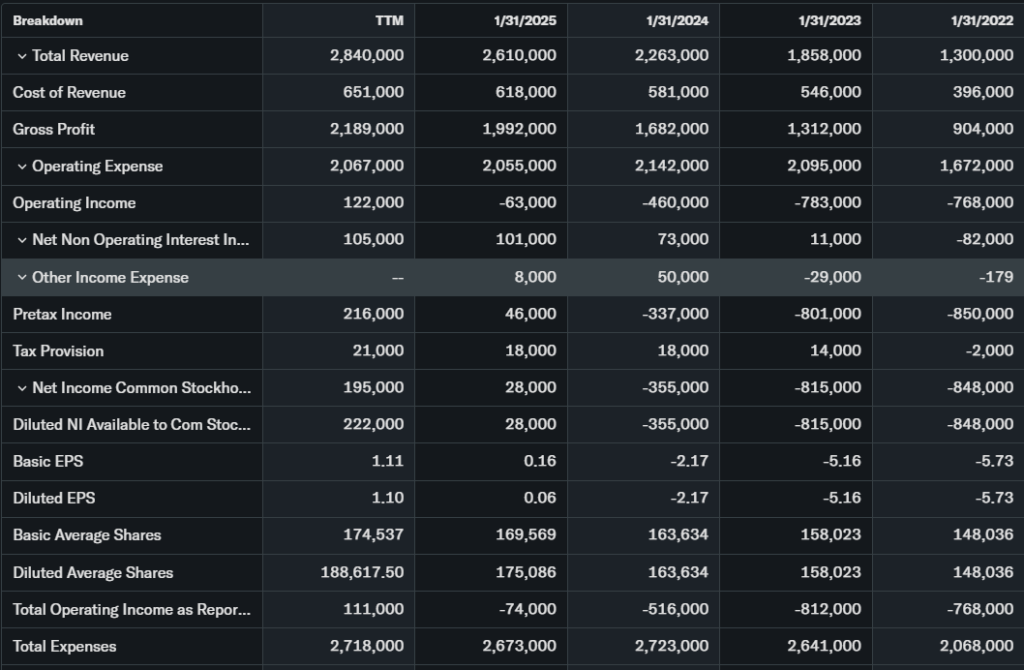

Revenue grew 11% YoY to $761M in Q4, full-year $2.919B up 12%. EPS hit $0.90 vs $0.85 forecast. Free cash flow reached $252M quarterly, cash at $2.5B, low debt.

Compared to Zoom (P/S 5x) or Microsoft (12x), OKTA stock appears fairly valued for growth. It trades at a premium but justifies via Rule of 40 compliance.

Recent Earnings & Catalysts

Q4 revenue hit $761M, beating $749M estimates. EPS $0.90 topped $0.85. Full-year revenue $2.919B up 12%.

Guidance for Q1 FY2027: $749-753M revenue, 9% growth. Catalysts include DoD partnership via myAuth and AI identity tools. Earnings dipped stock initially on guidance caution.

Bullish Case

Subscription revenue up 11% signals sticky demand. RPO at $4.8B, cRPO $2.5B show pipeline strength. Tech edges in zero-trust security drive adoption.

Operational leverage boosts margins to 23-24%. Free cash flow funds buybacks or AI investments realistically.

Bearish Case

Competition from Microsoft Entra heats up. Growth slowed to 9-12% from prior teens. Margin pressure from sales spend persists.

Macro slowdowns risk churn in enterprise clients. Regulatory scrutiny on data privacy adds hurdles.

Market Sentiment & Investor Psychology

Short interest at 5%, down slightly. Options show balanced calls/puts. Institutions own 80%, steady.

Retail tilts optimistic post-earnings. Sentiment neutral, shifting bullish on valuation relief.

Short-Term Outlook

Technicals point to $70 support hold. Volume uptick aids mild gains next week. Watch macro data for volatility.

Medium to Long-Term Outlook

Okta’s identity moat strengthens in cloud shift. Industry grows 15% annually. Solid balance sheet supports accumulation for long-term investors.

FAQ Section

Is OKTA stock a buy right now?

Yes for growth seekers at current levels, but wait for $70 dip. Analysts lean Buy.

What is the price target for OKTA stock?

Average $105, up 46% from $72.

What are major risks for OKTA stock?

Competition, slowing growth, macro headwinds.

OKTA earnings outlook?

Q1 guide 9% growth, full-year steady.

Suggestions

Compare with [Opendoor stock analysis].

See our [Microsoft stock forecast].

Read [tech sector valuation breakdown].

Final Balanced Conclusion

Hold OKTA stock for now. Strong fundamentals offset short-term caution, with upside to $105 long-term. Watch Q1 earnings.

Disclaimer: This article is for informational purposes only and not financial advice.