Explore our comprehensive NVDA stock analysis. We dive into Nvidia earnings, technical trends, and price targets to help you decide if the AI giant is a buy.

Introduction: The Backbone of the AI Revolution

Nvidia Corporation has transitioned from a niche graphics card manufacturer to the most critical infrastructure provider in the world. By designing the high-performance Graphics Processing Units (GPUs) that power artificial intelligence, Nvidia sits at the center of the global technology shift.

Investors are hyper-focused on NVDA stock right now because the company has become a bellwether for the entire S&P 500. As cloud service providers and governments race to build AI data centers, Nvidia’s hardware has become the “digital gold” of the 21st century.

While broader market conditions remain sensitive to interest rates, the tech sector continues to outperform. Nvidia’s role in this ecosystem makes it a unique case study in growth and valuation.

Latest Stock Price & Trend

As of February 23, 2026, the NVDA stock price is trading at $190.04. This represents a steady 1.14% increase over the previous day’s close. The stock has shown remarkable resilience in the face of shifting macroeconomic data.

Over the last five days, the trend has been moderately bullish as the market anticipates the upcoming earnings report. The one-month trend shows a gain of 8.2%, while the three-month performance stands at an impressive 14.5% increase.

Looking further back, the six-month trend reveals a 28.3% climb. Year-to-date, NVDA stock has already gained 12.1%, continuing the momentum from a record-breaking 2025. The 52-week high currently sits at $212.19, with a 52-week low of $86.63.

This trajectory indicates a strong, sustained bullish trend. Investors are currently treating dips as buying opportunities rather than signs of a reversal. The stock is trading well above its annual baseline, signaling high market confidence.

Technical Analysis: Navigating the Charts

Technical indicators for NVDA stock suggest a healthy but heated market environment. The primary support level is currently established at $175.00. If the price pulls back, this is where buyers have historically stepped in.

The immediate resistance level sits at $200.00. This psychological “round number” barrier has proven difficult to break through in recent weeks. A clean close above $200.00 could signal a fresh leg up for the rally.

The Relative Strength Index (RSI) is currently reading 64. This suggests the stock is approaching “overbought” territory (above 70) but still has some room to run. It indicates strong buying pressure without immediate exhaustion.

The Moving Average Convergence Divergence (MACD) remains in a bullish crossover state. The 50-day moving average is comfortably above the 200-day moving average. This “Golden Cross” configuration is a classic sign of long-term upward momentum.

Trading volume has been slightly above average. High volume on green days suggests institutional accumulation. For a technical trader, these signs point toward a “buy the dip” strategy within an established uptrend.

Analyst Ratings & Price Targets

Wall Street remains overwhelmingly optimistic about Nvidia’s future. Out of 55 analysts covering the stock, 48 maintain a “Buy” or “Strong Buy” rating. Only 6 analysts suggest a “Hold,” and just 1 carries a “Sell” rating.

The average price target for NVDA stock is currently $225.82. The most aggressive “street high” target sits at $300.00, while the conservative “street low” is $140.00. Recent upgrades from firms like Goldman Sachs and Morgan Stanley cite the Blackwell chip ramp-up.

Analyst sentiment suggests that while the stock has grown significantly, the “earnings power” of the company justifies the price. Most analysts believe the market is still underestimating the long-term demand for AI enterprise software.

Insider Activity

Recent SEC filings show a pattern of consistent, planned selling by Nvidia insiders. Over the last 90 days, senior executives have sold approximately $105 million worth of shares. However, it is vital to note these sales were conducted under 10b5-1 trading plans.

These plans are scheduled months in advance to avoid conflicts of interest. There has been no significant “unplanned” selling, which would usually signal a lack of confidence. CEO Jensen Huang still maintains a massive stake in the company.

Large institutional transactions show that hedge funds and pension funds are still increasing their positions. This suggests that while individual insiders are diversifying their wealth, the “smart money” still sees a growth path ahead.

Valuation Analysis

Evaluating Nvidia requires looking at growth-adjusted metrics. The trailing Price-to-Earnings (P/E) ratio is 47.01. While this seems high compared to the broader market, the Forward P/E is more modest at 23.6x.

Nvidia’s Price-to-Sales (P/S) ratio stands at 32.5. This is significantly higher than Microsoft (12.1) or Alphabet (6.5). However, Nvidia’s revenue growth of 67.5% Year-over-Year (YoY) far outpaces its mega-cap peers.

The company maintains a stellar balance sheet with deep cash reserves and manageable debt. Its Free Cash Flow (FCF) margins are among the highest in the semiconductor industry. Compared to rivals like AMD, Nvidia appears “fairly valued” when factoring in its dominant market share.

Recent Earnings & Catalysts

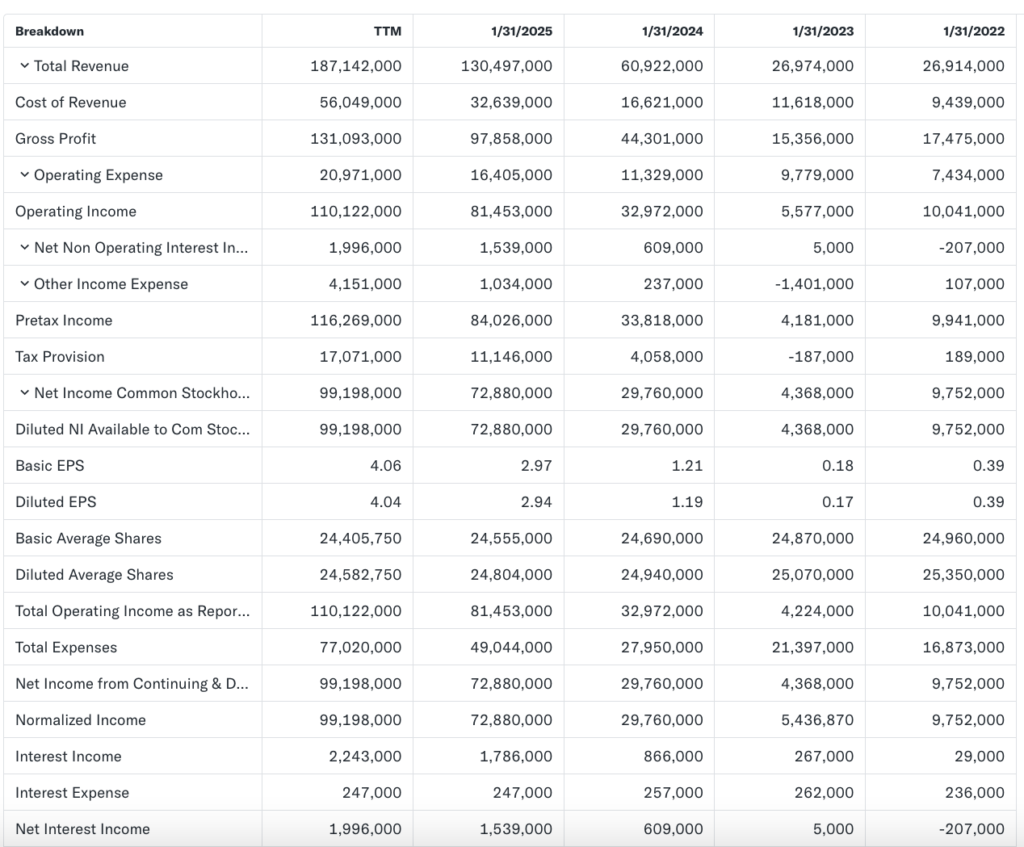

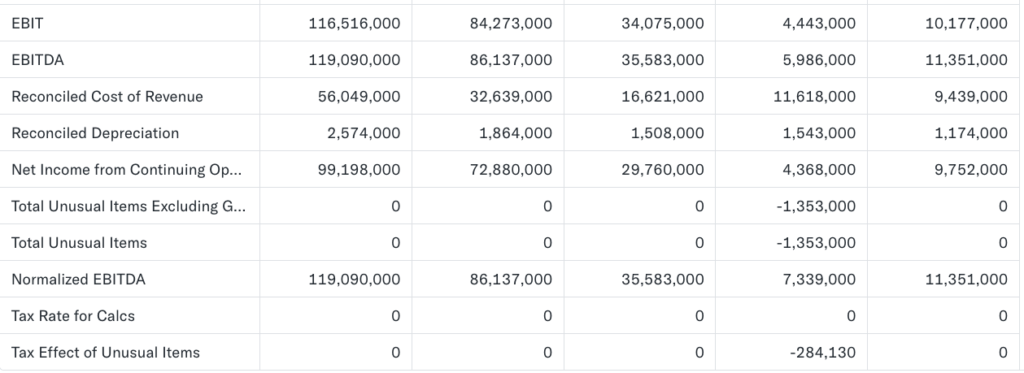

The last NVDA earnings report exceeded all expectations. The company reported record quarterly revenue, driven primarily by the Data Center segment. This growth was fueled by the transition from traditional CPU-based computing to GPU-accelerated computing.

The primary catalyst for the coming months is the “Blackwell” chip architecture. Nvidia has stated that demand for Blackwell is “staggering” and exceeds supply. Any update on production yields will likely move the stock price significantly.

Another catalyst is the expansion into “Sovereign AI.” Countries are now building their own domestic AI clouds. This creates a new customer base beyond just the major US cloud providers like Amazon and Google.

Bullish Case: Why the Rally Could Continue

The bullish case for NVDA stock rests on its “moat.” Nvidia does not just sell chips; it sells an entire software ecosystem called CUDA. This makes it extremely difficult for customers to switch to competitors.

Furthermore, the expansion of AI into robotics and autonomous vehicles provides a second wave of growth. If Nvidia becomes the “brain” of the global robotics fleet, its current revenue could be just the beginning.

Operational efficiency is also a key driver. Nvidia is able to maintain high gross margins because its products are considered “must-have” technology. This pricing power protects the company from inflationary pressures affecting other sectors.

Bearish Case: Risks to Consider

The primary risk for Nvidia is its high concentration of revenue. A small group of “Hyperscalers” (Microsoft, Meta, Google) accounts for a large portion of its sales. If these companies reduce their capital expenditure, Nvidia’s growth could stall.

Geopolitical tensions also pose a threat. Export restrictions on advanced chips to China limit Nvidia’s access to one of the world’s largest markets. Any further tightening of these regulations could impact the long-term NVDA forecast.

Finally, there is the risk of “AI digestion.” After a period of massive buying, customers may take time to implement the hardware before ordering more. This could lead to a cyclical slowdown in an otherwise high-growth story.

Market Sentiment & Investor Psychology

Market sentiment toward Nvidia is currently “Optimistic.” Short interest remains low at roughly 1.2% of the float, meaning very few traders are willing to bet against the company.

Options activity shows a heavy bias toward “Calls” (bets that the price will rise). Institutional ownership sits at over 65%, providing a stable floor for the stock. Retail investor behavior remains highly bullish, often viewing Nvidia as a “core” long-term holding.

The momentum bias is strong. However, some value-oriented investors are beginning to show caution, waiting for a more significant pullback before entering new positions.

Short-Term Outlook

For the next few weeks, the NVDA stock direction will be determined by the February 25 earnings call. If the company provides strong guidance for the Blackwell ramp-up, we could see a push toward the $210 level.

Technically, the stock is in a consolidation phase. Expect high volatility surrounding the earnings announcement. If the stock holds the $185 support level through the earnings cycle, the short-term path remains upward.

Medium to Long-Term Outlook

Over the next 6 to 24 months, the outlook for Nvidia remains strong. The business model is shifting toward recurring software revenue, which could lead to higher valuation multiples.

Long-term investors should focus on the company’s ability to maintain its technological lead over AMD and Intel. As long as Nvidia remains the standard for AI training, the stock is likely to remain a leader in the tech sector.

For those with a multi-year horizon, “accumulating” on major pullbacks (10-15%) has historically been a winning strategy. Nvidia is no longer just a “chip company”; it is a foundational utility for the digital age.

FAQ Section

Is NVDA stock a buy right now?

NVDA remains a strong growth play, but new investors should be aware of the high valuation. Many analysts suggest buying on dips rather than at all-time highs.

What is the price target for NVDA stock?

The consensus analyst price target is approximately $225.82, representing a potential upside of 18% from current levels.

What are the major risks for NVDA stock?

Key risks include geopolitical tensions with China, potential spending cuts from major tech customers, and increasing competition from custom-designed chips.

Suggestions

- Compare with AMD stock: See how Nvidia’s chief rival is performing in the AI race.

- Microsoft stock forecast: Explore how the world’s largest AI software buyer impacts the market.

- Tech sector valuation breakdown: Understand how NVDA fits into the broader semiconductor industry.

Final Balanced Conclusion

Nvidia continues to defy gravity by delivering consistent, massive growth. While the valuation is high, it is backed by real earnings and a dominant market position. For most investors, NVDA stock serves as an essential exposure to the AI theme.

A “Hold” or “Watchlist” approach is appropriate for those wary of short-term volatility. However, for those with a long-term perspective, Nvidia’s role in the future of computing remains unmatched.

Disclaimer: This article is for informational purposes only and not financial advice.