Explore JOBY stock analysis with latest price, technicals, earnings, and forecasts. Is JOBY stock a buy? Get balanced insights for investors on Joby Aviation’s eVTOL future.

Introduction

Joby Aviation develops electric air taxis for urban travel. These vertical takeoff vehicles aim to cut city commutes. JOBY stock draws attention amid eVTOL hype and regulatory wins.

Tech stocks face pressure from high rates, but aviation innovation boosts interest. Investors watch FAA progress and partnerships like Delta. Broader markets stay volatile in 2026.

JOBY stock price reflects pre-revenue growth bets. Everyday investors eye its path to 2025 services.

Latest Stock Price & Trend

JOBY stock closed at $10.01 on March 1, 2026. It ranged from $9.81 to $10.32 that day, down from prior close of $10.23. Volume hit 27.68 million shares, above average of 23.72 million.

Over five days, JOBY showed volatility after funding news. One-month trend leaned down amid dilution fears from $1.38 billion raise. Three-month view mixed with certification hopes.

Six-month performance dropped from peaks near $20. Year-to-date, it’s off highs but above lows. 52-week high stands at $20.95, low at $4.96. Overall trend looks sideways to bearish short-term.

This signals caution for investors. High volume hints at interest, but recent dips show funding worries. Watch for support near lows.

Technical Analysis

Support levels sit around $9.81, recent lows where buyers may step in. Resistance looms at $10.32 and prior highs near $11. These levels matter as they guide entry or exit points.

RSI at 59.59 shows neutral, not overbought or oversold. Values above 70 signal sell risks; below 30, buy chances. It helps spot momentum shifts.

MACD at 0.69 leans sell, with line above signal but fading. This tracks trend speed; crossovers predict turns.

50-day moving average trails price; 200-day lags further. No golden cross (bullish 50 over 200) yet—watch for it. Averages smooth noise for trend direction.

Volume trends up lately, supporting moves. High volume confirms real interest, not fakeouts.

Analyst Ratings & Price Targets

Analysts rate JOBY a Hold overall. Counts show few Buys, more Holds, minimal Sells. Average target is $13.43, up 33.5% from $10.01. High at $18, low $7.

Recent views mix optimism on certification with cash burn caution. Wall Street sees path to revenue but dilution risks.

This sentiment means steady progress priced in. Investors gain from targets as benchmarks, not guarantees.

Insider Activity

Recent insider selling topped 1.08 million shares worth $11.52 million in last 30 days. No buys reported. Executives trimmed amid stock rise.

Trends show sales, not purchases. This may signal caution or personal needs, not panic. Large transactions lack buys, implying less confidence boost.

Investors view sales warily in growth stocks. It suggests management locks profits pre-milestones.

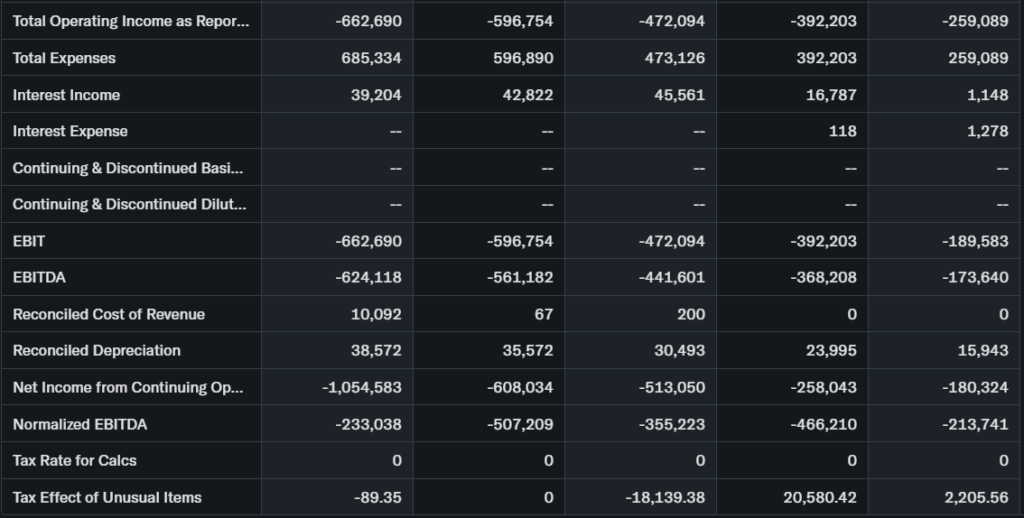

Valuation Analysis

Trailing P/E is negative at -8.94 due to losses. Forward P/E stays negative. Price-to-sales ratio exceeds 157,000x on low revenue—typical for pre-profit firms.

2025 revenue hit $53.43 million, up massively YoY from $136,000. EPS was -1.13; net loss $929.84 million. Free cash flow negative; cash at $1.4 billion post-raise. Debt low.

Compared to peers like Archer, JOBY looks premium on hype. It appears overvalued on current metrics but growth bets justify for some.

Recent Earnings & Catalysts

Q4 2025 revenue was $31 million, beat views via Blade unit. EPS -$0.14 topped -$0.20 estimates. Net loss narrowed to $122 million aided by warrant gains.

Guidance: 2026 revenue $105-150 million. Catalysts include vertiports with Metropolis, Ohio factory for four taxis monthly by 2027, CES 2026 prep.

Earnings lifted stock briefly, but funding diluted gains. Progress on FAA certification drives future pops.

Bullish Case

eVTOL demand grows with urban traffic woes. Joby leads via Toyota, Delta ties.

Certification nears; manufacturing scales. Cash pile funds to 2028. Revenue ramps via Blade, contracts.

Partnerships like Air Force deals add credibility.

Bearish Case

Competition heats from Lilium, Archer. Pre-revenue status means cash burn risks.

Dilution from $1.38 billion raise pressures shares. Regulatory delays possible. Economic slowdowns hit travel. Margins thin on scaling.

Market Sentiment & Investor Psychology

Short interest data limited, but options show balanced calls/puts. Institutional ownership steady.

Retail piles in on eVTOL buzz; volume spikes reflect hype. Sentiment neutral to optimistic on long-term, fearful short-term post-funding.

Short-Term Outlook

Technicals neutral; RSI steady, MACD soft sell. Volume high but downtrend lingers.

Momentum fades post-raise; expect sideways near $10. Watch $9.80 support.

Medium to Long-Term Outlook

Strong model in air mobility. Industry booms; Joby competitive via pilots.

Financials solid with cash; risks in execution. Hold for believers, watch for others. Accumulate on dips if certified.

FAQ

Is JOBY stock a buy right now?

Hold rating prevails; targets above current but risks high. Weigh certification odds.

What is the price target for JOBY stock?

Average $13.43, range $7-18. Analysts see 33% upside potential.

What are major risks for JOBY stock?

Dilution, delays, competition, cash burn.

JOBY earnings outlook?

2026 revenue $105-150M; EPS improves slowly.

Suggestions

Compare with Opendoor stock analysis.

See eVTOL sector forecast.

Read urban mobility tech breakdown.

Final Balanced Conclusion

Watchlist JOBY stock. Growth potential exists, but dilution and losses warrant caution. Long-term hold if eVTOL pans out.

Disclaimer: This article is for informational purposes only and not financial advice.