Explore IBRX stock price, earnings, technical analysis, and forecast. Is IBRX stock a buy? Get balanced insights on ImmunityBio’s valuation and outlook as of March 2026

Introduction

ImmunityBio develops cancer immunotherapies and vaccines. It focuses on treatments like Anktiva for bladder cancer. IBRX stock draws attention due to recent earnings beats and biotech momentum. Broader market volatility from interest rates affects biotech stocks.

Investors watch IBRX stock for pipeline progress amid sector recovery.

Latest Stock Price & Trend

IBRX stock closed at $10.44 on March 2, 2026. It rose 6.7% that day after strong earnings. The 5-day trend shows gains from high volume trading at 38 million shares.

One-month performance climbed over 30% from February lows around $8. Three-month trend points up 50%, driven by Q4 results. Year-to-date, IBRX stock gained 25%, beating biotech peers. The 52-week high hit $10.98 recently; low was $3.50 last year.

Overall trend looks bullish short-term. This signals growing investor confidence, but volatility remains high in biotech.

Technical Analysis

Support levels sit at $9.50 and $8.00, where buyers stepped in recently. Resistance looms at $11.00 and $12.00 from prior peaks. These levels help predict bounces or pullbacks.

RSI reads 65, nearing overbought but not extreme—watch for cooling. MACD shows bullish crossover, favoring upside momentum. The 50-day moving average at $9.20 crossed above the 200-day at $7.50, forming a golden cross. This pattern often signals longer rallies.

Volume spiked to 38 million shares on March 2, above average. Rising volume confirms IBRX technical analysis strength for buyers.

Analyst Ratings & Price Targets

Six Buy ratings, one Sell yield a Moderate Buy consensus. Average price target is $12.60, with high at $15 from HC Wainwright. Low sits at $7 from Piper Sandler.

Recent upgrades include Piper Sandler lifting from $5 to $7 in January. Wall Street sees upside from Anktiva sales ramp. Analyst sentiment suggests optimism, but biotech risks temper views. Investors use this as a benchmark, not gospel.

Insider Activity

Insiders sold 501,967 shares worth $4.47 million in 90 days. Director Christobel Selecky sold 25,000 shares February 23. Yet insiders hold 69.48% of stock, showing skin in game.

Selling ties to profit-taking post-rally. No major buying recently implies caution, not panic. Track for confidence signals.

Valuation Analysis

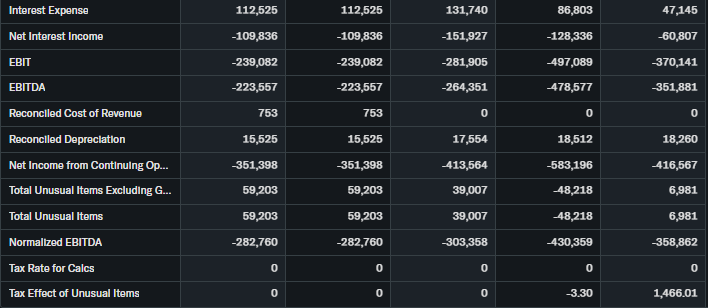

Trailing P/E is N/A due to losses; forward P/E eyes improvement. Price-to-sales ratio reflects 88x on $113M TTM revenue. Revenue grew 668% YoY to $113M. EPS is -0.38, better than prior -0.46.

Free cash flow stays negative at biotech norms. Debt is manageable with cash reserves. Versus peers like smaller biotechs, IBRX stock appears fairly valued on growth potential, not cheap.

Recent Earnings & Catalysts

Q4 2025 revenue hit $38.29M, beating estimates. EPS loss of $0.06 topped consensus -0.08. Full-year revenue reached $113M, up sharply. Guidance points to commercialization gains.

Anktiva FDA approval drives catalysts. Earnings beat sparked 6.7% jump. Stock rose on pipeline momentum.

Bullish Case

Revenue growth from Anktiva sales accelerates. Bladder cancer market demand grows. Tech edges in T-cell therapies stand out. FDA nods boost operations.

Partnerships could expand reach steadily.

Bearish Case

Competition from big pharma pressures margins. Losses persist at $351M yearly. Regulatory delays risk setbacks. Economic slowdowns hit biotech funding.

High beta of 1.88 amplifies market drops.

Market Sentiment

Short interest data limited, but options lean calls post-earnings. Institutional ownership steady; retail piles in on surges. Momentum favors bulls over value traps.

Sentiment tilts optimistic yet cautious.

Short-Term Outlook

Technicals show bullish MACD and volume. Momentum persists if support holds $9.50. Expect volatility around $11 resistance next weeks.

Medium to Long-Term Outlook

Business model hinges on immunotherapy pipeline. Industry grows with cancer needs. Competitive moat from approvals helps. Financials improve slowly. Long-term investors should watch for revenue ramps; hold if owned.

FAQ Section

Is IBRX stock a buy right now? Moderate Buy consensus says yes for growth seekers, but high risk suits aggressive portfolios.

What is the IBRX stock price target? Average $12.60, high $15, low $7 per analysts.

IBRX forecast for 2026? Upside tied to sales; expect volatility.

What are major risks for IBRX stock? Losses, competition, FDA hurdles.

IBRX earnings next? Q1 2026 due May; watch revenue beats.

Suggestions

- Compare with Opendoor stocks

- See our tech biotech sector valuation breakdown

- Read our immunotherapy stock forecast guide

Conclusion

Hold IBRX stock for now. Growth from Anktiva offsets risks, but await sustained profits. Biotech volatility demands patience.

Disclaimer: This article is for informational purposes only and not financial advice.