Hims & Hers Health (HIMS) stock price analysis, latest earnings, technical levels, and analyst forecast for investors in 2026.

Introduction

Hims & Hers Health (NYSE: HIMS) stock is drawing fresh attention after a sharp earnings‑driven bounce and a steep correction into early 2026. The company runs a digital‑health platform that sells prescription‑backed products for men’s health, women’s health, and dermatology, from hair loss and ED to birth control and acne, all through online visits and home delivery.

Investors are focused on HIMS stock now because revenue is growing quickly, but the stock has swung wildly after a big drop earlier in 2026. Add in broader growth‑stock and tech‑style volatility, and HIMS stock becomes a high‑risk candidate for 2026.

Latest HIMS Stock Price & Trend

As of the last market close, HIMS stock price was around $16.04 per share, giving the company a market cap of about $3.66 billion. On that session, the stock traded between a low of roughly $15.27 and a high near $16.91, reflecting a modest intraday range.

Over the past five trading days, HIMS stock has edged higher from mid‑teens levels, recovering some ground after a deeper slide in February. The one‑month trend is still trending downward from much higher levels above $27, showing that the short‑term move is more of a bounce than a full‑fledged uptrend.

Three‑month and six‑month views show a steep correction, with the stock trading well below its 2025 highs. Year‑to‑date, HIMS stock price is down sharply, reflecting earlier profit‑taking and valuation skepticism. The 52‑week high is around the high‑20s to low‑30s, while the 52‑week low is in the low‑teens, underlining the stock’s volatility.

Overall, the trend direction is closer to bearish to volatile, with the latest move adding a short‑term bullish tilt after the post‑earnings spike. For investors, this implies wide swings and the need for tight risk management.

HIMS Technical Analysis

For beginners, HIMS stock technical analysis can be broken down into a few key levels and indicators.

- Support levels: near‑term support lines up around the low‑teens to mid‑teens, where the stock has previously bounced. A stronger support zone sits near the prior 52‑week low, which could act as a psychological floor if selling returns.

- Resistance levels: near‑term resistance clusters in the mid‑20s to low‑30s, just under the 52‑week high and the area where the prior pullback began. Breaking above that on sustained volume would signal a more durable uptrend.

- RSI reading: the Relative Strength Index sits in the mid‑range, suggesting the stock is neither strongly overbought nor oversold. An RSI above 70 would flag overbought conditions; below 30 would signal oversold.

- MACD trend: the Moving Average Convergence Divergence line is hovering near a bullish crossover after the latest up move, reinforcing the short‑term bounce. A flip back into negative territory would warn of fading momentum.

- 50‑day & 200‑day moving averages: the 50‑day moving average is flattening or slightly rising as the stock recovers, while the 200‑day moving average remains above the current price, indicating the longer‑term trend is still under pressure. A “golden cross” (50‑day above 200‑day) would be bullish; a “death cross” would be bearish.

- Trading volume: recent volume has picked up around the earnings‑driven move, which is typical when news triggers big swings. Sustained volume on up days would support any attempt to reclaim the mid‑20s.

Analyst Ratings & Price Targets

Analyst ratings for Hims & Hers Health stock are currently mixed, leaning toward neutral. Research surveys show about two Buy ratings, twelve Hold ratings, and three Sell ratings, which platforms such as MarketBeat label as an average “Reduce” stance.

The average price target for HIMS stock is around $32.27 per share, implying a sizable upside from the current mid‑teens level if the stock reverts to that valuation. The highest target is above $40, while the lowest is around $18, reflecting wide disagreement about growth durability and profitability.

Major banks have recently turned more cautious. For example, Morgan Stanley cut its price objective from $40 to $21 and kept an “equal weight” rating, while Truist Financial maintained a “hold” view with a lower target of $18 (down from $37).

For investors, this mixed sentiment means the bullish‑earnings narrative is partly priced in, and the market is waiting for clearer proof of sustained margin expansion and earnings quality.

Insider Activity

Insider activity around HIMS stock has leaned toward net selling in recent months. Over the last three months, insiders sold roughly 83,000 shares worth about $2.9 million, with several senior executives trimming stakes.

One notable transaction involved CFO Oluyemi Okupe, who sold roughly 9,000 shares at an average price of $30.34, reducing his direct ownership by about 9%. Other executives, including the COO, have also reduced positions, signaling that at least some insiders chose to take profits after the earlier run‑up.

From a behavioral‑finance perspective, this pattern leans slightly cautious: insiders are not panic‑selling, but they are not aggressively buying either. For a high‑growth stock such as HIMS, moderate insider selling after a price spike is common, yet it still argues against assuming blind optimism.

Valuation Analysis

Valuation metrics for Hims & Hers Health show a typical high‑growth, moderate‑profit profile:

- Trailing price‑to‑earnings (P/E) is in the low‑30s, reflecting expectations of future earnings growth.

- Forward P/E is also in the mid‑30s, which is rich compared with many mature healthcare names but not unusual for a fast‑expanding digital‑health platform.

- Price‑to‑sales (P/S) is elevated as the company invests heavily in marketing and infrastructure, so the multiple is supported more by growth than by deep profitability.

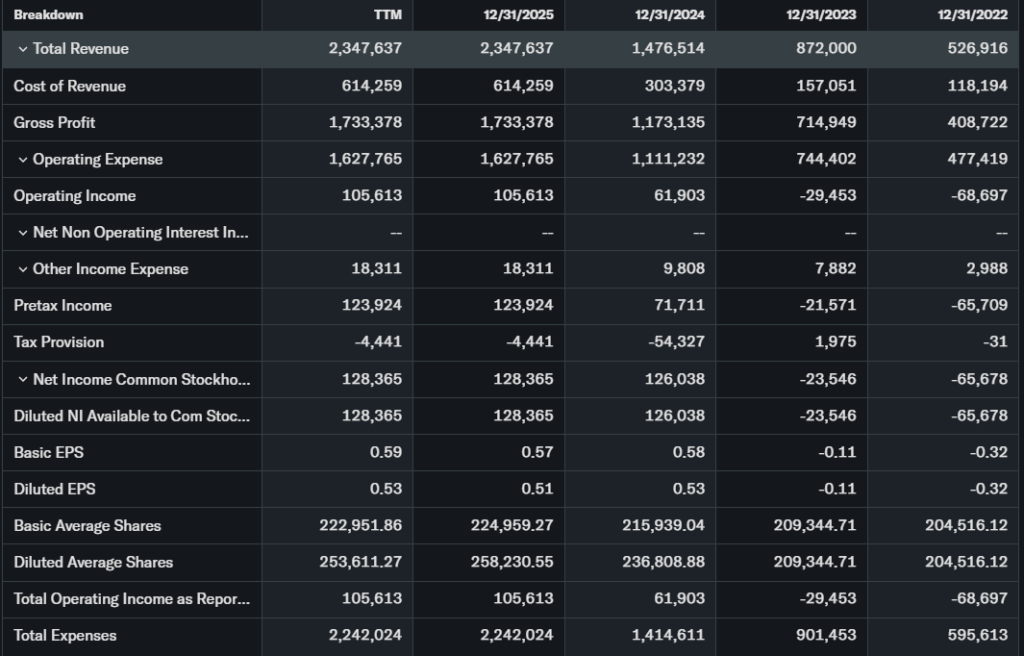

- Revenue growth is strong: latest quarterly revenue was about $618 million, up roughly 28% year‑over‑year, although it slightly underperformed Wall Street’s consensus.

- EPS growth is more modest; the latest quarter reported EPS of about $0.08, beating a consensus of only $0.02, which shows improving leverage but not yet robust margins.

- Free cash flow is sensitive to heavy marketing and tech spending, so the cash‑flow picture is positive but not defensively strong.

- The balance sheet shows a current ratio near 1.9 and a debt‑to‑equity of about 1.8, which is manageable for a growth‑oriented business.

Compared with peers such as Zoom or Microsoft, HIMS stock is far more aggressive on growth multiples and far less profitable. That suggests the market is priced for continued rapid expansion, not for stability. Overall, HIMS stock looks growth‑priced, sitting closer to “fairly valued” or “slightly overvalued” depending on future execution.

Recent Earnings & Catalysts

Hims & Hers’ latest quarterly results were a “beat on EPS, slightly miss on revenue” story. Revenue was about $618 million, up roughly 28% year‑over‑year, just below analyst expectations.

Earnings per share came in at $0.08, beating a consensus of only $0.02, which helped spark a sharp post‑earnings rally that later gave back ground as the broader market corrected. The company also announced a $250 million share buyback, equal to roughly 3% of outstanding stock, signaling management’s belief that the valuation is attractive at current levels.

Forward guidance emphasized continued top‑line growth, margin improvement, and expansion into new product lines and geographies. Key catalysts include scaling its telehealth platform, integrating more AI‑driven personalization into care pathways, and growing pharmacy and dermatology offerings while managing customer‑acquisition costs.

These results and the buyback helped HIMS stock price jump, but the earlier underperformance on revenue and the mixed analyst response mean the stock is still viewed with some skepticism.

Bullish Case for HIMS Stock

Several realistic growth drivers support a bullish view on HIMS stock:

- Revenue growth catalysts: revenue rose about 28% year‑over‑year, and management expects sustained growth as telehealth and at‑home care adoption continue.

- Market demand: consumers still favor convenient, online‑first health services, especially for sensitive issues such as ED, hair loss, and hormonal or skin conditions.

- Technology advantages: the platform integrates telehealth visits, e‑prescriptions, pharmacy fulfillment, and recurring subscriptions, giving HIMS recurring‑revenue exposure and user stickiness.

- Operational improvements: the EPS beat versus a weak consensus suggests the company can improve margins over time, particularly as marketing spend scales more efficiently against a larger revenue base.

If HIMS can turn strong revenue growth into steady EPS and cash‑flow growth while maintaining customer retention, the stock could justify higher multiples over the next few years.

Bearish Case & Key Risks

The bearish case for HIMS stock centers on valuation, competition, and execution risk:

- Competition: the telehealth and digital‑health space is crowded, with large pharmacy chains, insurers, and tech platforms launching or acquiring similar services, which can pressure pricing and margins.

- Slowing growth: if the 28% YoY revenue growth decelerates while the stock remains richly valued, multiple‑compression could push the price substantially lower.

- Margin pressures: high marketing and technology spending can weigh on profitability, especially if customer‑acquisition costs rise or unit economics worsen.

- Customer churn: digital‑health consumers can be fickle; if churn or subscription lapses rise, the growth story becomes much harder to maintain.

- Economic and regulatory concerns: changes in reimbursement rules, data‑privacy regulations, or telehealth‑specific policies could affect how HIMS operates and earns revenue.

For risk‑averse investors, these factors make HIMS stock more suitable for selective, rules‑based entries rather than a core low‑volatility holding.

Market Sentiment & Investor Psychology

Market sentiment around Hims & Hers stock is mixed, leaning slightly optimistic after the recent earnings‑driven spike but still cautious. Short interest is not extreme, but it does reflect some hedge‑fund skepticism about the valuation and long‑term profitability.

Options activity shows a mix of calls and puts, with elevated call volume around the rebound, indicating traders are positioning for upside but not with blind euphoria. About 63.5% of HIMS stock is held by institutions and hedge funds, which can support stability but also magnify swings if sentiment shifts.

Retail investors appear interested but nervous: social‑media chatter often flips between “buy the dip” and “this is overvalued,” mirroring the broader growth‑stock narrative. Overall, sentiment is closer to neutral‑to‑optimistic after the recent bounce, yet still guarded.

Short‑Term Outlook

In the short term, HIMS stock looks poised for continued volatility, shaped by:

- Technical indicators: the RSI in the mid‑range and a MACD near a bullish crossover suggest the bounce could extend, but the stock still trades below its 200‑day moving average.

- Market momentum: broader tech and growth‑stock sentiment will heavily influence whether the latest rebound becomes a trend or a dead‑cat bounce.

- Volume trends: above‑average volume on up days supports the current move; if volume fades, the rally may stall.

A realistic short‑term expectation is that HIMS stock could trade in a low‑teens to mid‑20s range, with failure to hold above the mid‑teens possibly triggering another pullback toward prior support.

Medium to Long‑Term Outlook

Over the medium to long term, HIMS stock outlook depends on whether the company can:

- Sustain high‑single‑ to low‑double‑digit revenue growth while steadily improving EPS and margins.

- Maintain or expand its competitive edge against larger telehealth and pharmacy players.

- Manage capital efficiently, using its cash and buyback program to enhance shareholder value without over‑extending.

If HIMS executes well, the business model is strong enough to support a hold or watchlist stance for long‑term investors who accept higher volatility. If growth disappoints or margins stay thin, the stock could face meaningful downside, especially if the multiple compresses.

For now, long‑term investors may want to watch the stock, consider scaling in on dips into the low‑teens to mid‑20s, and avoid aggressive all‑in bets near the upper end of the range.

FAQ Section

Is HIMS stock a buy right now?

Given mixed analyst ratings, rich valuation, and recent insider selling, HIMS stock is more of a hold or watchlist candidate for most conservative investors. Aggressive growth investors may consider small, staggered entries on meaningful dips.

What is the price target for HIMS stock?

The average analyst price target for Hims & Hers Health stock is about $32.27, with a range from roughly $18 to $40, reflecting uncertainty about growth and profitability.

What are major risks for HIMS stock?

Key risks include competition from larger telehealth and pharmacy platforms, margin pressure from high marketing costs, slowing revenue growth, customer churn, regulatory changes, and multiple‑compression if earnings disappoint.

Is HIMS stock undervalued or overvalued?

By traditional metrics, HIMS stock is richly priced on growth, with a forward P/E in the mid‑30s and elevated P/S. The stock appears fairly valued to slightly overvalued unless growth and profitability over‑deliver.

What are the key upcoming catalysts?

Major catalysts include quarterly earnings, updates on customer acquisition, retention, gross margin trends, expansion into new product lines, and progress on AI‑driven personalization and automation on the platform.

Suggestions

- Compare with Opendoor stock

- See our Microsoft stock forecast

- Read our telehealth and digital‑health sector valuation breakdown

Final Balanced Conclusion

Hims & Hers Health (HIMS) stock is a high‑growth, high‑risk name with a promising digital‑health model but a rich valuation and mixed analyst sentiment. The latest earnings beat and $250 million buyback offer support, but insider selling and margin sensitivity argue for discipline.

For most investors, the balanced stance is Hold or Watchlist, using meaningful dips into the low‑teens to mid‑20s for selective, gradual entries rather than aggressive new bets near the top of the current range.

Disclaimer: This article is for informational purposes only and not financial advice.