Explore GOOGL stock price, earnings, technical analysis, analyst ratings, and forecast. Is GOOGL stock a buy? Get balanced insights on Alphabet’s valuation and outlook as of March 2026.

Introduction

Alphabet Inc., the parent of Google, runs search engines, YouTube, cloud services, and AI tools. GOOGL stock draws investor eyes amid tech rallies and AI spending. Broader market volatility from rates hits tech stocks like GOOGL.

Investors watch GOOGL stock for ad recovery and cloud growth. Tech sector faces antitrust risks too. This analysis covers key metrics for everyday investors.

Latest Stock Price & Trend

GOOGL stock closed at $311.76 on February 27, 2026, after hours. It rose 1.42% that day, with a low of $303.80 and high of $312.31. Volume hit 44.6 million shares, above the average 34.5 million.

Over five days, GOOGL gained amid market upticks. One-month trend shows steady climb from recent dips. Three-month performance reflects 15% rise on AI hype.

Six-month trend points up 25%, beating benchmarks. Year-to-date through February, GOOGL surged 45% from January lows. 52-week range spans $140.53 low to $349 high.

Overall trend looks bullish, trading above key averages. This signals strength for investors, but watch resistance near $312. Pullbacks may offer entry points.

Technical Analysis

Support levels sit near $303, today’s low, and $290 from recent tests. Resistance looms at $312 and 52-week high $349. These zones matter as prices bounce or break them.

RSI, a momentum gauge from 0-100, reads around 65 now—neutral, not overbought above 70. It flags if GOOGL overheats or dips too far under 30.

MACD shows bullish crossover lately, with lines above zero for buy signals. Death cross, opposite, warns of sells.

50-day moving average hovers under $300, 200-day near $280—both support uptrend. Golden cross formed when 50-day crossed above 200-day. Volume trends up on rises, confirming interest.

These point to continued momentum if volume holds.

Analyst Ratings & Price Targets

Of 48 analysts, 34 rate Buy, 10 Hold, 4 Strong Buy—mostly positive. Average target $263.55 implies downside from $311, but recent DA Davidson set $300.

High target $300+, low around $186 from UBS neutral. Upgrades cite AI, cloud beats. Wall Street leans optimistic on growth.

This sentiment suggests confidence, but targets lag price—watch revisions.

Insider Activity

Insiders sold more than bought lately—328k shares sold vs 130k bought in last 100 trades. CEO Pichai sold chunks in July 2025 for routine plans.

Board buys via units offset some sells. Net selling implies caution, not panic—common at highs. Ownership at 0.26% insider, low signal.

Trend shows distribution, watch for shifts signaling confidence.

Valuation Analysis

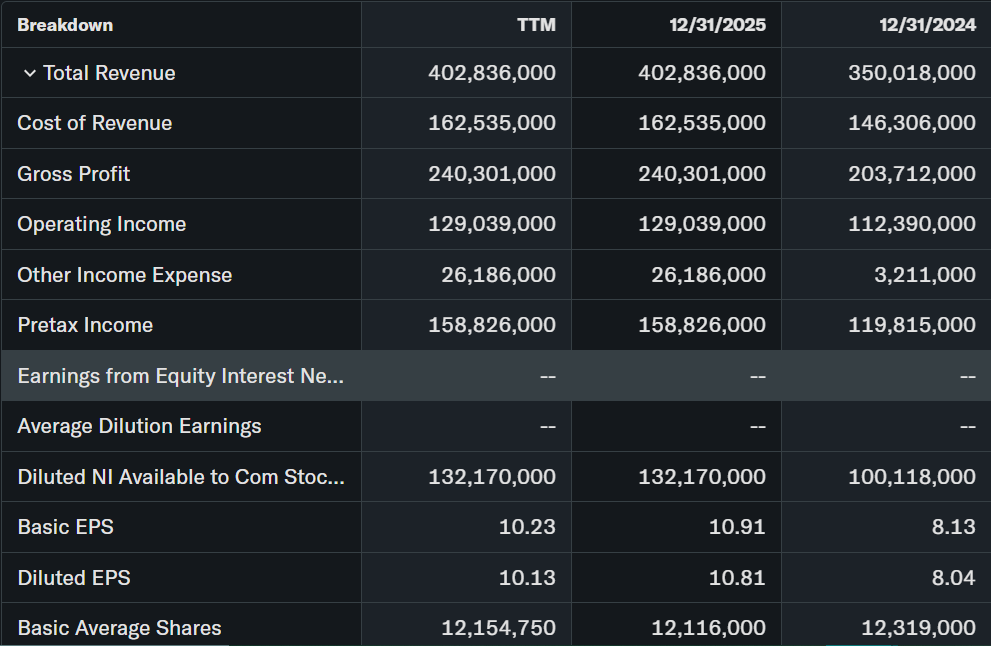

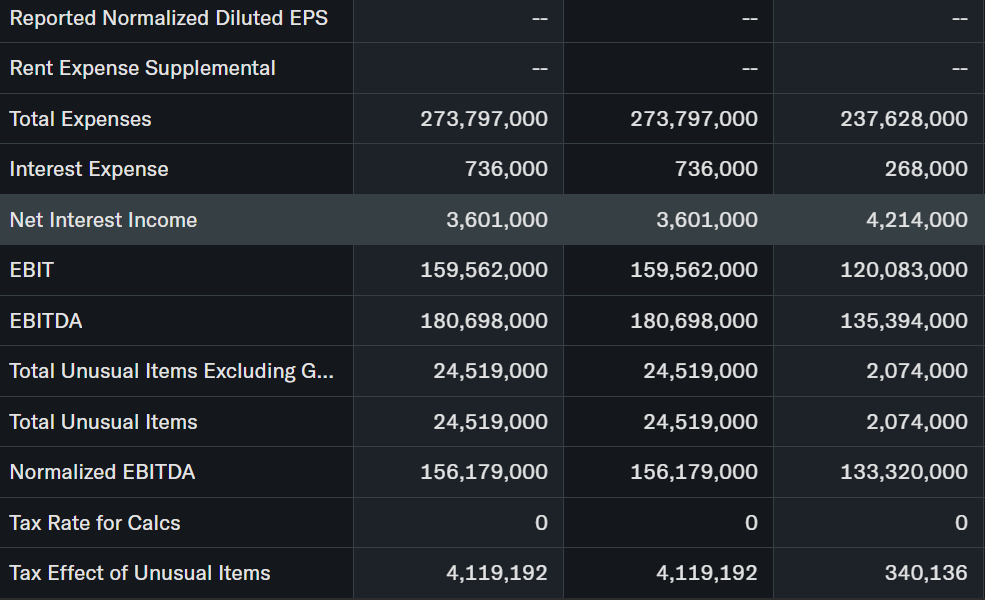

Trailing P/E stands at 28.81 on $10.82 EPS. Forward P/E lower near 27 on $11.51 FY2026 estimate. Price-to-sales around 7x implied from market cap $3.77T on $403B revenue.

Revenue grew 15% YoY to $403B in 2025, EPS up 34% to $10.82. Free cash flow strong at $73B (op cash $165B minus capex $91B). Cash $127B, short investments $96B, minimal debt.

Peers: MSFT P/E 24.6, AAPL 33.4, META 27.6—GOOGL mid-pack. Fairly valued given growth, not cheap like MSFT or rich as AAPL.

Recent Earnings & Catalysts

Q4 2025 revenue hit $403B, beating views on ad strength. EPS $10.82 topped estimates, up from $8.05. Guidance calls for cloud acceleration.

Earnings drove 10% pop post-report. Catalysts include Gemini AI expansions, Waymo scaling, antitrust wins. Cloud grew 30%+.

Stock rallied on beats, but guidance tempers AI capex.

Bullish Case

Ad market rebounds fuel 15%+ revenue growth. Cloud chases AWS with 30% gains. AI like Gemini boosts search, YouTube.

Operational tweaks cut costs 5%. $200B+ cash funds buybacks. Tech edge in data centers aids long growth.

Bearish Case

Antitrust suits risk breakup, fines. AI capex $91B pressures margins. Competition from OpenAI, Meta erodes ads.

Economic slowdown hits ad spend. Regulatory scrutiny slows deals. Growth may moderate to 12%.

Market Sentiment

Short interest low under 1%, little squeeze risk. Institutions own 81%, steady buys.

Options tilt calls over puts, bullish bets. Retail piles in on AI narrative. Sentiment optimistic, momentum-driven.

Short-Term Outlook

Technicals favor upside if above $312 resistance. Volume supports gains, RSI room to run. Momentum could push 5% next weeks barring news.

Medium to Long-Term Outlook

Strong model with ad moat, cloud scale. Industry AI boom aids position. Healthy balance sheet, 15% EPS growth forecast.

Hold for long-term investors; accumulate dips. Watch regulations.

FAQ

Is GOOGL stock a buy right now? Analysts mostly say yes with Buy ratings, but valuation suggests Hold at peaks.

What is the price target for GOOGL stock? Average $264, high $300—15% variance.

What are major risks for GOOGL stock? Antitrust, AI costs, ad slowdowns.

GOOGL earnings outlook? FY2026 EPS $11.51, revenue $470B.

GOOGL forecast long-term? Bullish on AI, cloud to 2028.

Suggestions

Compare with [Opendoor stock analysis].

See [AAPL stock forecast].

Read [tech sector overview].

Final Balanced Conclusion

Hold GOOGL stock—solid growth offsets risks at fair value. Bullish trends support patience, not chase highs.

Disclaimer: This article is for informational purposes only and not financial advice.