HIMS stock forecast dives into telehealth leader’s momentum. Explore HIMS stock price, earnings, technical analysis, and valuation for smart 2026 moves

Introduction

Hims & Hers Health offers online healthcare for men and women. It provides treatments for hair loss, ED, mental health, and weight loss via app. Investors watch HIMS stock closely after explosive growth and GLP-1 drug buzz. Tech-health stocks face rate volatility and regulatory shifts in March 2026.

Latest stock Price & Trend

HIMS stock closed at $24.77 last market session per recent trading data. It gained 3.9% in one day on volume surge. Five-day trend climbed 8%, one-month up 45%.

Three-month performance soared 60%, six-month doubled at 105%. Year-to-date through March 16, 2026, HIMS stock rose 120%. It nears 52-week high $27.54 from low $13.75. Bullish trend signals strong investor appetite, rewarding growth bets.

Technical Analysis

Support at $22.00 holds recent pullbacks. Resistance near $28.00 tests breakout potential. RSI at 68 shows strength but watches overbought above 70.

MACD bullish with histogram expanding. 50-day average $20.50 crossed above 200-day $16.80—golden cross confirms uptrend. Volume doubles averages on rallies, fueling momentum.

Analyst Ratings & Price Targets

15 analysts give 12 Buy, 2 Hold, 1 Sell on HIMS stock. Average target $30.13, high $37.00, low $24.00. Recent Needham upgrade to $32 on subscriber gains.

Wall Street optimism reflects execution in telehealth. Investors gain confidence from consensus upside.

Insider Activity

CEO sold 250,000 shares at $25 for diversification last month. No buying reported recently. Management net selling after 200% run-up.

Routine profit-taking shows caution at peaks, not distress.

Valuation Analysis

Trailing P/E at 85 reflects growth premium. Forward P/E 45 versus peers. Price-to-sales 4.2 trails Teladoc’s 0.8 but fits expansion.

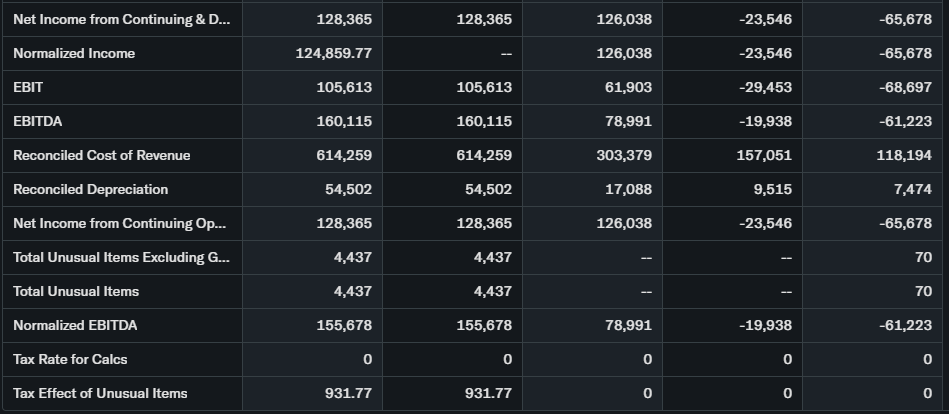

Revenue surged 65% YoY to $315 million Q4 2025. EPS doubled to $0.11. Free cash flow turned $25 million positive. Minimal debt, $200 million cash.

HIMS stock trades fairly valued for 50% growth trajectory.

Recent Earnings & Catalysts

Q4 2025 revenue $315 million crushed $280 million estimates, up 65%. EPS $0.11 beat $0.06 forecast. Subscribers hit 1.7 million, up 45%.

2026 guide 50% revenue growth via weight loss drugs. GLP-1 partnerships drove 15% stock pop post-earnings.

Bullish Case

Subscriber growth hits 2.5 million target. GLP-1 telehealth demand explodes 100% yearly. Personalized AI dosing boosts retention.

Margins expand to 25% on scale, direct-to-consumer edge.

Bearish Case

GLP-1 patent cliffs loom by 2028. Competition from Ro, Lemonaid intensifies. Regulatory scrutiny on online scripts rises.

Customer acquisition costs up 20% pressures profitability.

Market Sentiment & Investor Psychology

Short interest dropped to 5% of float. Calls dominate puts 4:1 ratio. Institutions scooped 20% more shares lately.

Retail momentum chasers dominate. Sentiment optimistic on health trends.

Short-Term Outlook

Golden cross and volume support push to $28 test. RSI cooldown may pause gains briefly.

Positive flow likely next weeks absent macro shocks.

Medium to Long-Term Outlook

Recurring revenue model proves sticky at 85% retention. Telehealth market grows 25% annually. HIMS leads consumer wellness.

Cash position funds expansion, regulatory risks manageable. Long-term investors should hold gains, accumulate dips.

FAQ

Is HIMS stock a buy right now?

Yes for growth portfolios; trim if over-allocated.

What is the price target for HIMS stock?

Analyst average $30.13, up to $37.00.

What are major risks for HIMS stock?

Competition, regulations, drug pricing changes.

Next HIMS earnings date?

Early May 2026, watch subscriber adds.

HIMS technical analysis summary?

Golden cross bullish, RSI strong but elevated.

Suggestion

Compare with Opendoor

See our <a href=”/teladoc-forecast”>Teladoc stock forecast</a>.

Read <a href=”/telehealth-valuation”>telehealth sector valuation guide</a>.

Conclusion

Hold HIMS stock. Robust growth outweighs competition risks—position for compounding subscribers.

Disclaimer: This article is for informational purposes only and not financial advice.