HIMS stock analysis covers latest price trends, earnings, technicals, and 2026 forecast. Is HIMS stock a buy now? Explore valuation, risks, and outlook for everyday investors.

Introduction

Hims & Hers Health runs a telehealth platform. It sells wellness products like hair loss treatments and weight loss drugs online. Investors watch HIMS stock closely now due to its weight loss business and regulatory news. Broader market volatility in healthcare stocks adds pressure amid economic shifts.

HIMS stock price has swung wildly this year. Recent earnings showed growth but missed some targets. Tech sector gains help, yet regulatory risks loom large.

Latest Stock Price & Trend

HIMS stock closed at $15.88 at last market close on March 13, 2026. The 1-day performance rose 1.8%. Over 5 days, it gained slightly amid profit-taking.

The 1-month trend fell 37.8%. Three-month data shows deeper declines tied to earnings misses. Year-to-date, HIMS stock dropped 52%, reflecting regulatory fears.

Six-month performance weakened further. The 52-week high hit higher levels earlier, while the low sits below current prices. Overall trend looks bearish short-term but with rebound signs.

This indicates caution for investors. Pullbacks create entry points if growth resumes. Watch volume for confirmation.

Technical Analysis

Support levels sit near $15, a recent low. Resistance looms at $20, past highs. These levels matter as they show where buyers or sellers step in.

RSI reading hovers neutral, not overbought or oversold. It signals no extreme momentum yet. MACD trend leans bearish, with lines crossing down.

The 50-day moving average falls below the 200-day, no golden cross. Trading volume trends down, suggesting low conviction. These point to sideways action ahead.

Analyst Ratings & Price Targets

Analysts split on HIMS stock. Of 21 covering it, many rate Buy or Overweight. Average price target nears $30-$48. Highest hits $48 from Barclays.

Lowest around $25-$30. Barclays raised to $29 Overweight on March 11. Citi holds Sell at $30. Upgrades show optimism post-Novo news.

This sentiment means mixed views. Bulls see growth; bears flag risks. Investors use it to gauge consensus.

Insider Activity

Insider selling dominated recently. No major buying noted in latest SEC filings. Management trimmed shares amid stock drops.

Large transactions involved executives. Trends show caution, not panic selling. This implies tempered confidence amid uncertainty.

Valuation Analysis

Trailing P/E stands high due to earnings volatility. Forward P/E looks better at growth rates. Price-to-Sales ratio reflects premium on revenue.

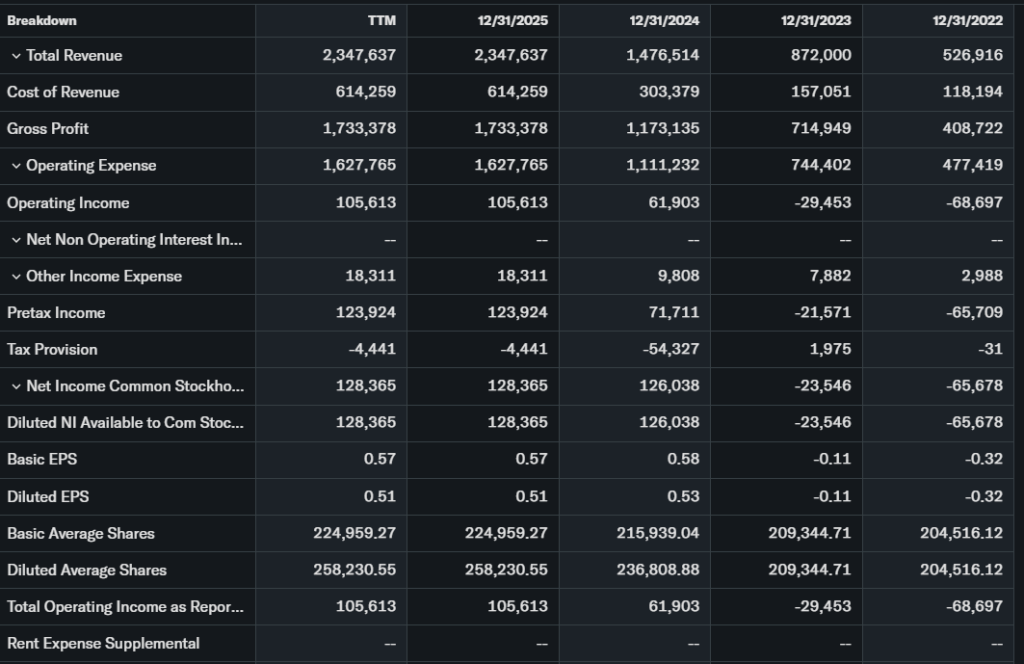

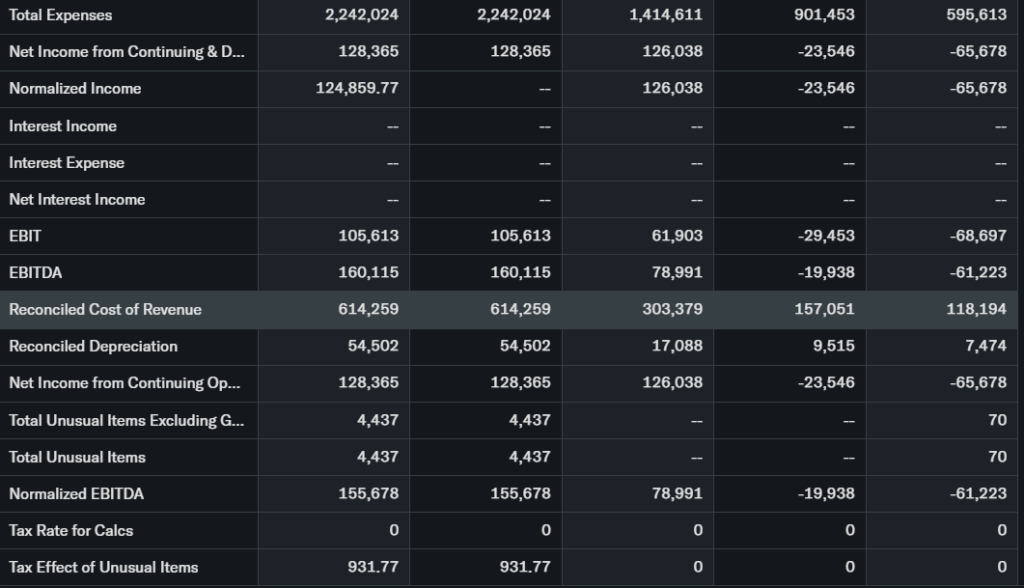

Revenue grew 28% YoY to $617.8 million last quarter. EPS missed slightly. Free cash flow improves; debt low with strong cash.

Compared to peers like Teladoc, HIMS stock appears fairly valued. Not overvalued, but not cheap. Growth justifies multiple.

Recent Earnings & Catalysts

Latest quarter revenue hit $617.8 million, up 28% YoY, shy of $619.22 million expected. EPS beat some views but Q1 guidance low at $600-625 million.

2026 revenue forecast $2.6-2.9 billion tops $2.74 billion estimates. Catalysts include Eucalyptus acquisition and Canada entry. Labs testing launch adds services.

Earnings dipped stock initially. Guidance offers upside surprise potential.

Bullish Case

Revenue growth hits from subscriber base at 2.5 million, up 13%. Non-weight loss products drive most profits.

International moves like Australia deal boost reach. Tech like YourBio sampling aids diagnostics. Barclays sees FY26 drivers.

Operational scale and diversification support realistic expansion.

Bearish Case

Competition heats in GLP-1 drugs from Novo Nordisk. Regulatory risks hit compounded semaglutide.

Growth may slow if margins squeeze. Economic slowdowns curb elective spending. Churn rises in telehealth.

Market Sentiment & Investor Psychology

Short interest data shows elevated levels. Options lean puts over calls lately. Institutional ownership steady.

Retail chases momentum dips. Sentiment neutral, shifting optimistic on acquisitions.

Short-Term Outlook

Technicals show support hold. Volume picks up on rebounds. Momentum could push to resistance next weeks.

Expect choppy trading without big catalysts.

Medium to Long-Term Outlook

Business model scales via platform. Industry grows in telehealth. Financial health solid with cash.

Competitive edge in personalization. Long-term, hold or accumulate on dips. Watch regulations.

FAQ

Is HIMS stock a buy right now?

Mixed. Growth potential yes, but risks high. Wait for support hold.

What is the HIMS stock price target?

Average $30-48. Barclays at $29 Overweight.

HIMS stock forecast for 2026?

Revenue $2.6-2.9B. Upside if expansions work.

What are major risks for HIMS stock?

GLP-1 regulations, competition.

HIMS earnings next quarter?

Guidance $600-625M revenue.

Suggestion

Compare with Opendoor stock analysis.

See our telehealth sector forecast.

Read HIMS technical analysis update.

Conclusion

Hold HIMS stock for now. Growth drivers balance risks. Long-term watchlist worthy.

Disclaimer: This article is for informational purposes only and not financial advice.