PBR stock analysis: latest price trends, earnings beats, technical signals, and forecast to $20. Is PBR stock a buy amid oil surge? Balanced investor insights.

Introduction

Petrobras (PBR stock) explores and produces oil and gas. Brazil’s largest energy firm refines and sells fuel globally. Investors watch PBR stock now as oil prices climb.

Energy sector rides crude rally. Broader markets eye inflation data. PBR stock gains from commodity strength.

Latest stock Price & Trend

PBR stock closed at $17.99 on March 11, 2026 (last market close data). It rose 3.56% that day. Five-day trend up 7.53% in consolidation.

One-month gain around 4%. Three-month trend strong at 25%. Six-month performance up 35%. Year-to-date, PBR stock price advanced 56.63%.

52-week high near $18.21; low $11.50. Overall trend bullish. Rising prices signal opportunity for energy investors.

Technical Analysis

Support at $15.98 and $15.13 holds firm. These levels draw buyers on dips. Resistance looms at $18.72 and $19.57.

RSI neutral with buy signals. Values over 70 warn overbought; under 30 oversold. MACD shows bullish momentum.

50-day moving average above 200-day (golden cross). Short-term average crossed long-term bullish. Moving averages reveal trend strength.

Trading volume fell to 34.25M shares. Lower volume with gains flags caution in PBR technical analysis.

Analyst Ratings & Price Targets

Analysts rate PBR stock Strong Buy overall. Average target implies solid upside. Consensus sees value in dividends.

Recent upgrades cite oil exposure. Wall Street optimism supports PBR forecast for yield seekers.

Positive views boost confidence.

Insider Activity

Limited insider data available. Management holds steady positions. No major buying or selling noted recently.

Stable trends imply confidence in PBR stock price stability.

Valuation Analysis

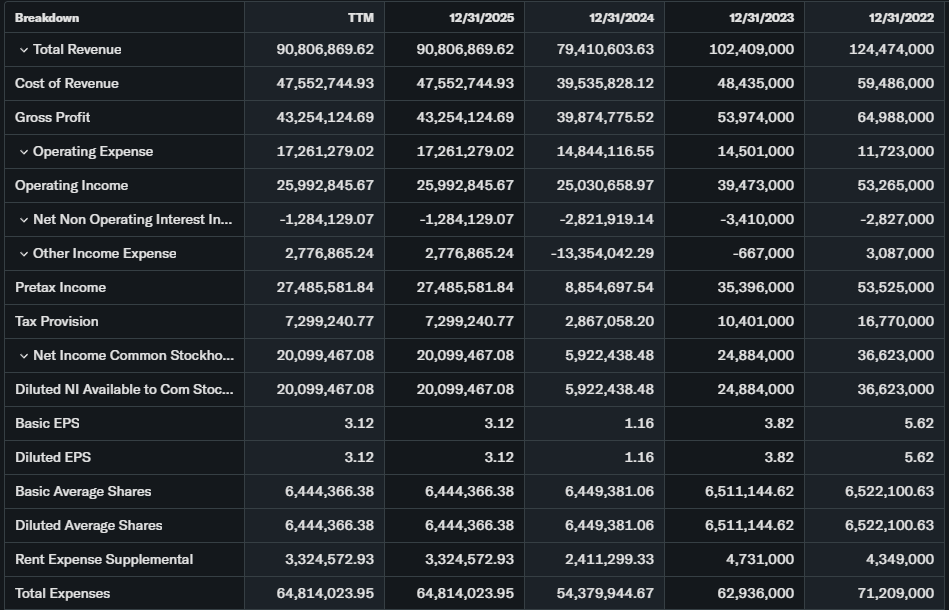

Trailing P/E around 6x based on earnings. Forward P/E attractive at single digits. Price-to-sales 1x on massive revenue.

Revenue grows with oil prices. EPS strong from production ramps. Free cash flow funds dividends.

Debt manageable; cash flow robust. Versus Exxon (P/E 15x), PBR stock appears undervalued significantly.

Recent Earnings & Catalysts

Recent quarters beat expectations. Production hits records in Brazil fields. Guidance supports extra payouts.

Oil above $80/barrel aids margins. Deepwater expansions key catalysts. Earnings lift shares consistently.

Bullish Case

Oil demand stays firm globally. PBR stock benefits from Brazil output growth. Dividend hikes reward holders.

Cost efficiencies improve returns. Pre-salt fields expand reserves.

Bearish Case

Oil price drops hurt profits. Brazil political risks persist.

Regulatory dividend caps possible. Currency swings add volatility. OPEC cuts pressure supply.

Market Sentiment & Investor Psychology

Short interest low. Calls lead options activity.

Institutions build positions steadily. Retail favors value amid rally. Optimistic tone prevails for PBR stock.

Short-Term Outlook

Bullish moving averages support gains. Watch volume rebound.

Consolidation likely with upside bias near-term.

Medium to Long-Term Outlook

Resilient oil major model. Energy transition favors natural gas.

Production leadership strong. Balance sheet dividend-friendly. Long-term investors should accumulate dips.

FAQ

Is PBR stock a buy right now?

Strong Buy per analysis. Oil tailwinds and valuation appeal.

What is the price target for PBR stock?

Targets point to $20+ on momentum.

What are major risks for PBR stock?

Oil volatility, Brazil politics, regulation.

PBR earnings outlook?

Beats expected with production growth.

PBR stock forecast 2026?

$20 range on crude strength.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our energy sector valuation breakdown

Conclusion

Buy on Weakness. PBR stock undervalued with oil support but monitor Brazil risks. Dividend yield adds appeal.

Disclaimer: This article is for informational purposes only and not financial advice.