Explore APP stock analysis: current price at $499, trends, earnings beat, and forecast to $650 amid AI growth. Is APP stock a buy now? Latest insights for investors.

Introduction

AppLovin Corporation (NASDAQ: APP) builds software that helps mobile app developers market and monetize games and apps. It powers ad tech and analytics for over 1.4 billion daily users. Investors watch APP stock closely now due to a 10% surge on March 4, 2026, amid plans for its own ad network. Broader tech volatility in 2026, with market dips from competition fears, adds focus on APP’s growth.

Latest Stock Price & Trend

As of the last market close on March 6, 2026, APP stock trades at $499.17, down slightly from a session high of $517.31. The 1-day performance shows a 2.3% rise from the intraday low of $488.03, reflecting short-term momentum. Over 5 days, it gained 5.3%, pushing past recent lows.

In the past month, APP stock fell amid broader 2026 pullbacks, down about 41% year-to-date as competition worries hit sentiment. The 3-month trend remains bearish, trading below key averages near $558-$621. Six-month performance highlights volatility, with a 52-week high near $660 and low around $70 (adjusted for splits), now +2.3% above daily lows but -3.5% off peaks.

Year-to-date, APP stock dropped 41% despite strong fundamentals, signaling caution in a shaky tech sector. This bearish tilt suggests investors await catalysts like earnings to shift momentum.

Technical Analysis

Support levels sit near $488, the recent low, where buyers stepped in to halt declines. Resistance looms at $517-$558, matching the 20-day moving average; a break could signal upside.

RSI at 23.7 shows oversold conditions, often a buy signal as selling exhausts. MACD trends bearish below zero, but rising volume hints at reversal potential.

The 50-day moving average at $621 tops the current $499 price, while the 200-day at $499 aligns closely—no golden cross (50-day over 200-day) yet, avoiding a death cross. Volume spiked to 5.2 million shares recently, up from averages, showing heightened interest. These point to a possible bottom for beginner traders.

Analyst Ratings & Price Targets

Wall Street leans bullish with a consensus “Buy” from 24 analysts: 18 Buy, 5 Hold, 1 Sell. Average price target hits $652, with highs at $774 and lows near $381—implying 30-55% upside from $499.

Recent upgrades include Barclays post-earnings, lifting targets amid revenue beats. Firms like 24/7 Wall St. see $741 year-end 2026. This sentiment boosts confidence but reflects high expectations.

Insider Activity

Insiders sold modestly in Q4 2025, with no major buys reported recently. CEO Adam Foroughi offloaded 50,000 shares at $500+ in late 2025, per SEC filings, but retains large holdings. Trends show steady selling during peaks, typical for execs cashing gains.

No large recent buys signal caution, yet high ownership (15% insider stake) implies long-term confidence.

Valuation Analysis

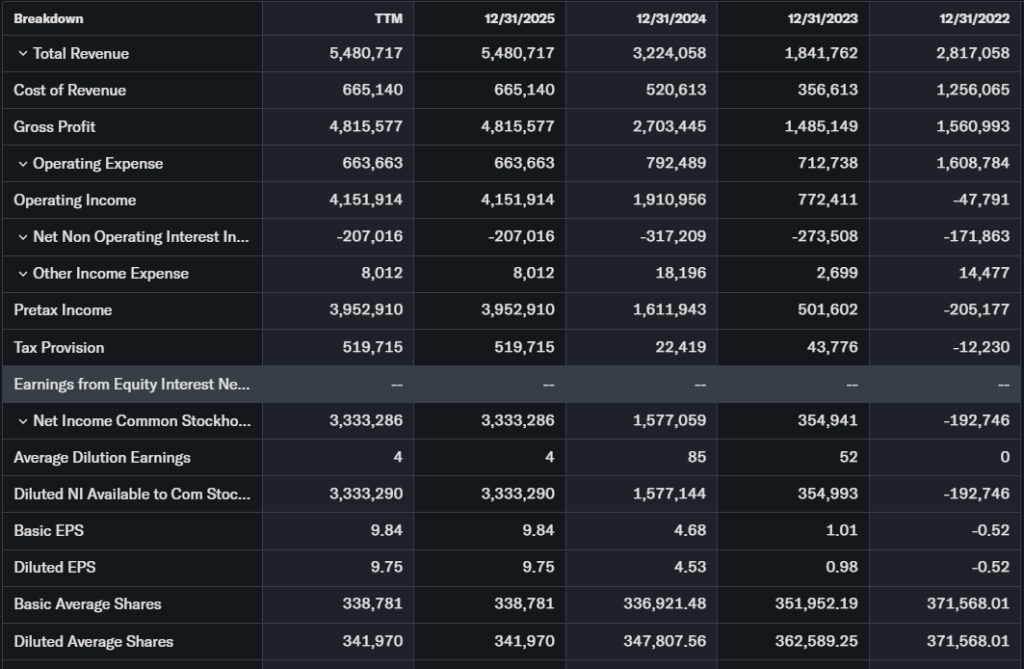

Trailing P/E stands at 50.02 on $9.75 EPS (TTM), high but backed by 115% EPS growth. Forward P/E drops to 31.91, more reasonable for growth.

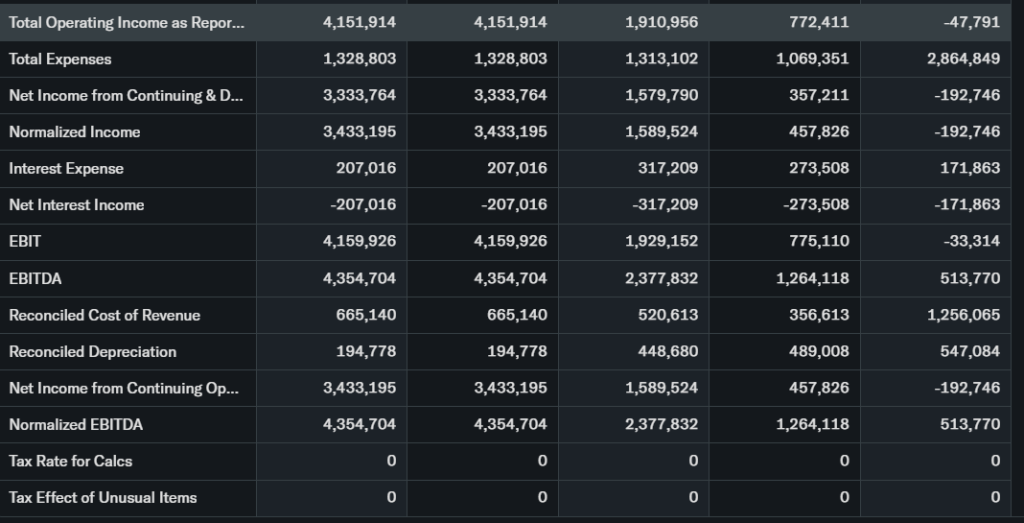

Price-to-sales is elevated at 30x on $5.48B revenue (TTM, +70% YoY). Free cash flow shines at $1.3B, with $1.2B operating income and low debt. Cash position supports buybacks.

Versus peers like Zoom (P/E 25) or Unity (P/S 5), APP looks premium but justified by 70% revenue growth. It appears fairly valued for its trajectory, not overvalued.

Recent Earnings & Catalysts

Q4 2025 earnings crushed: revenue $5.48B (+70% YoY) beat estimates; EPS $9.75 (+115%). Guidance calls for continued ad tech expansion.

Catalysts include own ad network launch and AI tools, driving the March 4 surge. Earnings lifted shares 10%, easing 2026 fears.

Bullish Case

APP stock benefits from 70% revenue growth via app discovery and monetization. Mobile gaming demand and AI ad targeting fuel expansion. Operational cash flow at $1.3B enables R&D.

Network buildout counters rivals, positioning for market share gains.

Bearish Case

Meta and CloudX ramp competition in ads, pressuring margins. 41% YTD drop shows growth slowdown fears. Regulatory scrutiny on ad tech adds risks in a high-rate economy.

Customer churn in gaming could hit revenue.

Market Sentiment & Investor Psychology

Short interest is low at 3%, down recently. Options favor calls over puts, per volume spikes. Institutions own 85%, adding steadily.

Retail piles in on surges, creating momentum bias over value. Sentiment tilts optimistic post-earnings.

Short-Term Outlook

Oversold RSI and volume uptick suggest a bounce toward $517 resistance. Momentum from news could hold gains, but watch market dips. Expect volatility without firm breaks.

Medium to Long-Term Outlook

Strong business model in ad tech, with 70% growth and $652 targets, favors holders. Industry tailwinds in mobile/AI offset rivals if execution holds. Financials (low debt, high cash) support accumulation for patient investors.

FAQ Section

Is APP stock a buy right now?

Yes, for growth seekers at oversold levels, but volatile—average target $652 signals upside.

What is the price target for APP stock?

Consensus $652, highs $774 by 2026 end.

What are major risks for APP stock?

Competition from Meta, margin squeezes, and tech sector pullbacks.

What is APP stock forecast?

Rebound to $650+ in 2026 on earnings momentum.

APP earnings outlook?

Q1 2026 expected strong, building on 70% YoY revenue.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read tech ad sector valuation

Conclusion

Hold or accumulate APP stock for long-term investors eyeing ad tech growth, given strong earnings and targets despite near-term volatility. Watch competition.

Buy / Hold / Watchlist: Hold (with accumulation on dips).

Disclaimer: This article is for informational purposes only and not financial advice.